If you spend any time with FinTV – even if it’s muted in the background – you would have been treated to a debate as to “Are we in a new bull market?” or not. Sometimes it’s phrased as “Is the bear market over?”

I believe this is the wrong way to think about bull and bear markets.

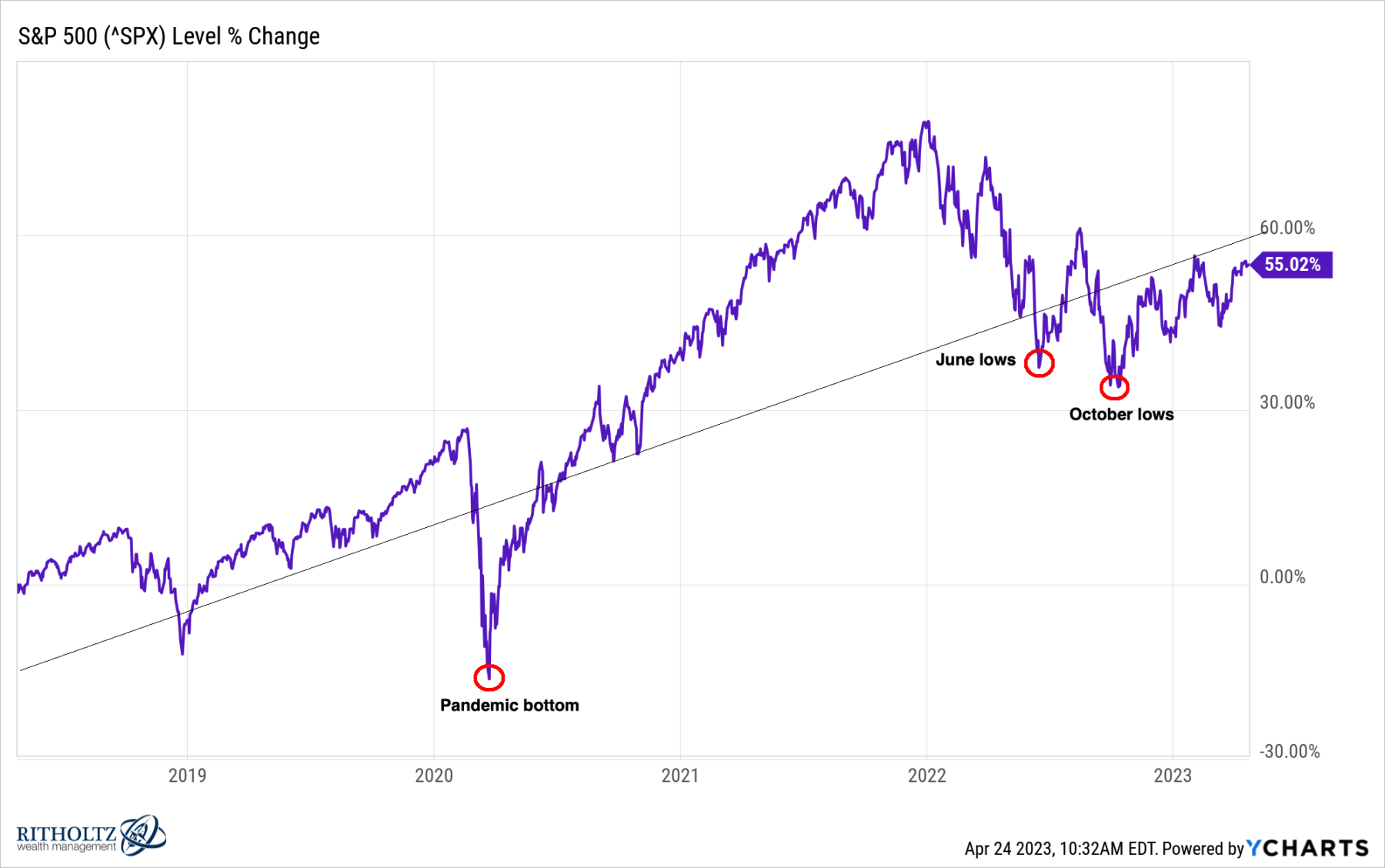

We have previously discussed why the 20% bull/bear frame of reference is simply noisy nonsense.1 It is a meaningless, media-creation fiction, a rule of thumb with no evidence showing it to be significant (beyond the fact we have that many fingers and toes).

But there are many other good reasons to avoid the “Buy Now, No, Sell Now” debate: First, few are any good at picking bottoms and tops; Second, no one should run “real” money2 that way as the costs for being wrong are simply too great. Third, it is an approach that generally lacks the sort of process essential to good investing.

Good investors understand that bear markets and volatility are part of where returns come from; these long-term investors have learned that riding them out is their highest probability approach.3

You might find it useful to instead think of Bull/Bear discussions in terms of context: When, Where, and for How Long.

When: Framing the question of “when” is simply asking what is the larger time-frame around any particular market move. Is this a pullback taking place within the context of a larger up move? Is this a bounce in the midst of a relentless grind lower? Understanding the broader context of when this move is occurring is useful in understanding the odds of it continuing.

Markets are like fractals, and what you see if often dependent upon the time frame you are using. You may find very different conclusions if you focus on minutes, days, weeks, months, quarters, years, or decades. A substantial chunk of market debates seems to be people with different time horizons talking past each other. The time periods I find useful are secular market moves that can last decades and cyclical moves that last months.

Where: In this morning’s reads, I referenced J.C. Paret’s discussion of overseas gains. When people complain they are in a bear market, we should recognize that they are often exhibiting “home country bias.” Just because their local bourse is in a drawdown does not mean that all of the equity markets in the world are in also in a drawdown. As JC noted: “It’s not the bull market’s fault that your country is underperforming.”

Indeed, diversification geographically often means that various equity holdings are behaving differently. Consider 4 geographic regions: The US, the Developed world Ex US, Emerging markets, and Frontier. They all have different sensitivities to economic factors like trade, inflation, commodities, and growth. Within the equity portion of your portfolios, they can provide some measure of diversification.

How Long: My favorite context for thinking about markets is the longer-term secular bull and bear markets is the word “secular.”

A Secular Bull Market is an extended period of time (10-20 years) driven by broad economic shifts that create an environment conducive to increasing corporate revenue and earnings. Its most dominant feature is the increasing willingness of investors to pay more and more for a dollar of earnings. Secular bear markets aren’t as long lasting, are more violent, but otherwise are the flipside of a bull.

But understanding when we are in a secular bull market might allow you better context to think about risk, and about how to manage your own behavior relative to turmoil.

One of the subtexts of the above is that for the vast majority of investors, Martin Gabel‘s admonition of “Don’t just do something, sit there” is most often their best approach.

Markets are complex mechanisms. Oversimplifying them into narratives or relying on context-free myths will not serve your portfolio well.

Previously:

Observations to Start 2023 (January 3, 2023)

Bottoming? (December 1, 2022)

Secular vs. Cyclical Markets, 2022 (May 16, 2022)

Bull Market Bull (March 31, 2021)

Redefining Bull and Bear Markets (August 14, 2017)

Are We in A Secular Bull Market? (November 4, 2016)

__________

1. If you want to read more on why 20% is not significant, see this, this, this, and this.

2. Real in terms of both importance to investors and size. Nobody should be swinging around billions of dollars based on gut instinct, and certainly not retirement accounts or other very important capital.

3. Note we have not even referencing the valuation debate.

The post When, Where, and for How Long… appeared first on The Big Picture.

{kind=link}