One of the most intimidating aspects of launching a solo advisory firm is the question of how to manage compliance. Advisors coming from a background of working as an employee at a larger firm may be familiar with some of the rules for complying with state or Federal securities regulations from the perspective of an individual advisor, but handling compliance for an entire firm – even when there is just 1 employee – entails a whole additional set of responsibilities to be aware of. Fortunately, the annually recurring nature of ongoing RIA compliance tasks makes it highly conducive to create a compliance calendar for a solo RIA (particularly because they must manage it all themselves) which helps to systematize and manage compliance tasks, requirements, and deadlines by breaking them up into discrete steps to complete incrementally throughout the year.

A good baseline for creating an annual Compliance Calendar comes from the North American Securities Adminstrators Association (NASAA), which publishes Model Rules for investment advisers that many states base their own requirements on, and can give an overall sense of the types of tasks RIAs can build into their own annual compliance calendar (with the caveat that specific compliance requirements for RIAs vary at the state level, where most solo advisors are registered).

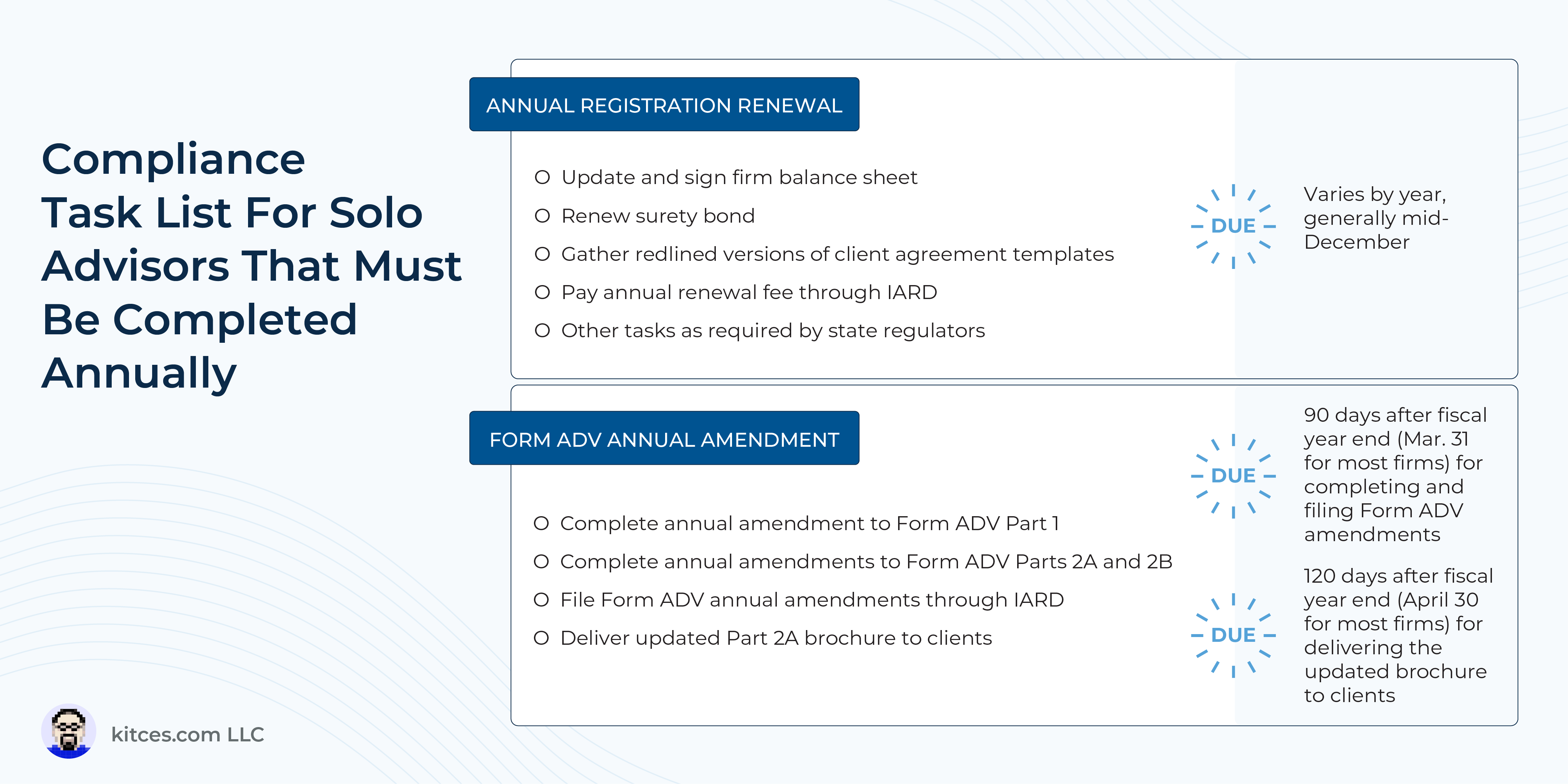

The 1st category of tasks that advisory firms must handle involves renewing their registration with the applicable state(s) in which they do business each year, which typically involves submitting select documents (e.g., accounting reports, client contract templates, and a surety bond) and filing an annual renewal fee near the end of the year. After year-end, firms typically have until March 31 to submit an annual amendment to their Form ADV Part 1 and Part 2A/2B, and until April 30 to offer a copy of their updated Form ADV to their clients.

Second, firms are generally required to adopt and implement a set of written policies and procedures governing the firm’s actions in areas including proxy voting, cybersecurity, personal trading of the firm’s employees, material nonpublic information, and the firm’s business continuity plan. Firm policies and procedures in each of these areas need to be reviewed and updated on an annual basis; however, given how wide-ranging each of these topics can be, solo advisors might want to consider tackling each topic separately at a different time each year (for example, addressing 1 major area each quarter).

Third, regulators require RIAs to maintain an extensive set of books and records of the firm’s business and advisory practices, including business and financial records (like bank statements and invoices), client-related documents (like written client communications, client agreements, and written information forming the basis of any recommendation made by the advisor), advertisements (including newsletters, blogs, and social media posts), and written copies of the firm’s policies and procedures (including records of holdings and trades in the advisor’s own personal accounts).

Putting all of this information together, it’s possible to create a compliance calendar that accounts for each task required, its frequency, and the due date for each. Because even though most compliance tasks (save for annual registration renewal and annual ADV updates) don’t have specific due dates during the year, setting a date for each task to be done – and blocking out specific time in the advisor’s calendar to do so – can ensure that it gets done. Which can be especially helpful for RIA founders who are also their own Chief Compliance Officers, and still have duty to oversee (and document that they are overseeing) themselves.

Ultimately, the key point is that turning a litany of annual RIA compliance tasks into a compliance calendar helps to systematize the process of managing compliance (especially for a solo RIA) in order to stay on top of all of the firm’s compliance requirements, even when there are other matters like client-facing work that can seem more urgent at any given time. Because once compliance tasks are systematized into time blocks on a calendar basis – approximately 1 hour for monthly tasks, 4 hours for quarterly tasks, and 8 hours for annual tasks, at least for a solo advisor – it’s feasible for the RIA to keep their compliance house in order with barely 2% of their annual working hours… leaving the other 98% of their time to serve their clients effectively (and get new ones, too!)!

{kind=link}