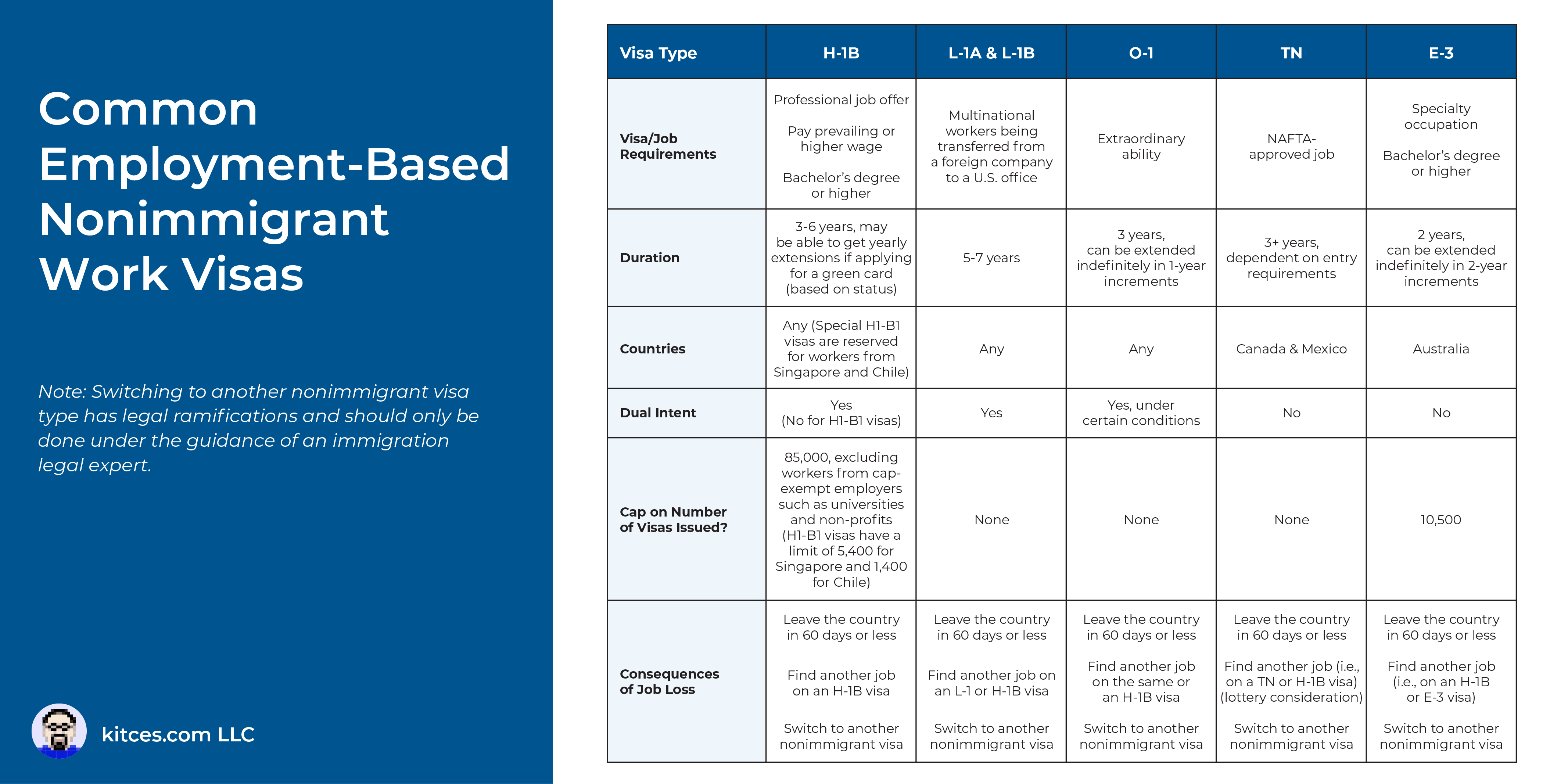

Amid a tight job market and low unemployment rates, a significant amount of the U.S. ‘talent gap’ is filled by foreign-born workers on employment visas like the H-1B. These visas allow foreign workers to live and work in the country temporarily while they are employed – although in practice, this can mean that individuals can spend years or decades (or even their entire career) working in the U.S. on a ‘temporary’ visa.

Like native-born workers, foreign workers need to think about saving for retirement, planning for their children’s college, managing healthcare costs, and all manner of other financial goals. However, the system in the U.S. that incentivizes saving for these goals for American citizens – namely with tax-advantaged accounts such as 401(k) plans, IRAs, 529 college savings plans, and Health Savings Accounts (HSAs) – can impose hurdles on foreign nationals who rely on them for their own savings needs.

For example, the tax benefits of certain accounts can sometimes work in the other direction if a non-U.S.-born worker contributing to them eventually moves back to their home country. Roth IRAs, for instance, are taxed once upon contribution and can grow tax-free thereafter in the U.S., which can allow for a large accumulation of tax-free savings over time; however, because some countries don’t recognize the tax-free nature of Roth accounts, withdrawing from the IRA in another country later could cause it to be taxed a second time, eliminating the primary benefit of Roth savings.

Additionally, foreign workers often also face hurdles in opening and accessing some accounts. For example, some brokerage firms won’t even allow foreign nationals to open new accounts, and others may require the individual to close the account and move their assets out if they ever move away from the U.S. and in some cases, entire account types may be unavailable due to the worker’s foreign status, such as 529 plans, which require beneficiaries to have a U.S. Social Security Number (making them effectively off-limits to individuals with noncitizen dependents) and necessitate a different approach to college savings than is common for U.S. citizens.

Ultimately, navigating saving and investing for foreign-born workers requires a careful balance of understanding the considerations and potential pitfalls of different savings strategies, knowing the person’s goals and plans (including potential relocation overseas), and – perhaps most importantly, given the uncertainty that can come with staying in the U.S. on a work visa – maintaining enough flexibility to preserve their assets should those plans change. Advisors who can stay on top of changes to immigration and tax law and help with navigating these challenges can serve a valuable role for foreign national clients – a potential client base that is only poised to grow in an increasingly global workforce!

{kind=link}