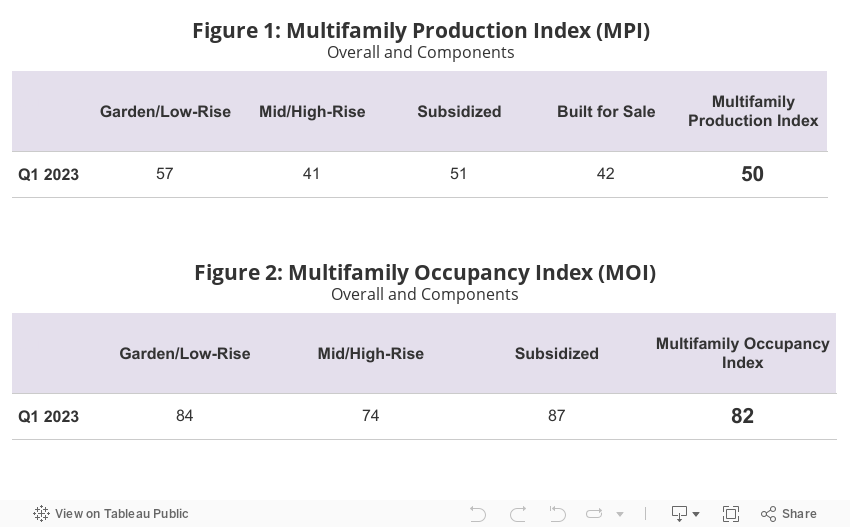

The National Association of Home Builders (NAHB) redesigned its Multifamily Market Survey (MMS) in the first quarter of 2023 to make it easier to interpret and more similar to the NAHB/Wells Fargo Housing Market Index (HMI) for single-family housing. The MMS produces two separate indices. The Multifamily Production Index (MPI) had a reading of 50 for the first quarter while the Multifamily Occupancy Index (MOI) reading was 82.

While occupancy is in positive territory and production is neutral, multifamily builders and developers are still experiencing many headwinds which include increased difficulty with obtaining loans from tightening financial conditions due to the continued interest rate hikes from the Fed and the cost of materials. NAHB forecasts that multifamily starts will decline by more than 10% per year in 2023 and 2024 given the aforementioned headwinds.

The new MPI is a weighted average of four key market segments: three in the built-for-rent market (garden/low-rise, mid/high-rise and subsidized) and the built-for-sale (or condominium) market. The survey asks multifamily builders to rate the current conditions as “good,” “fair, or “poor” for multifamily starts in markets where they are active. The index and all its components are scaled so that a number above 50 indicates that more respondents report conditions are good than report conditions are poor. For the first quarter, the component measuring garden/low-rise units had a reading of 57, the component measuring mid/high-rise units had a reading of 41, the component measuring subsidized units had a reading of 51 and the component measuring built-for-sale units had a reading of 42 (Figure 1).

The new MOI is a weighted average of three built-for-rent market segments (garden/low-rise, mid/high-rise and subsidized). The survey asks multifamily builders to rate the current conditions for occupancy of existing rental apartments in markets where they are active as “good,” “fair” or “poor.” Similar in nature to MPI, the index and all its components are scaled so that a number above 50 indicates more respondents report that occupancy is good than report it is poor. For the first quarter, the component measuring garden/low-rise units had a reading of 84, the component measuring mid/high-rise units had a reading of 74 and the component measuring subsidized units had a reading of 87 (Figure 2).

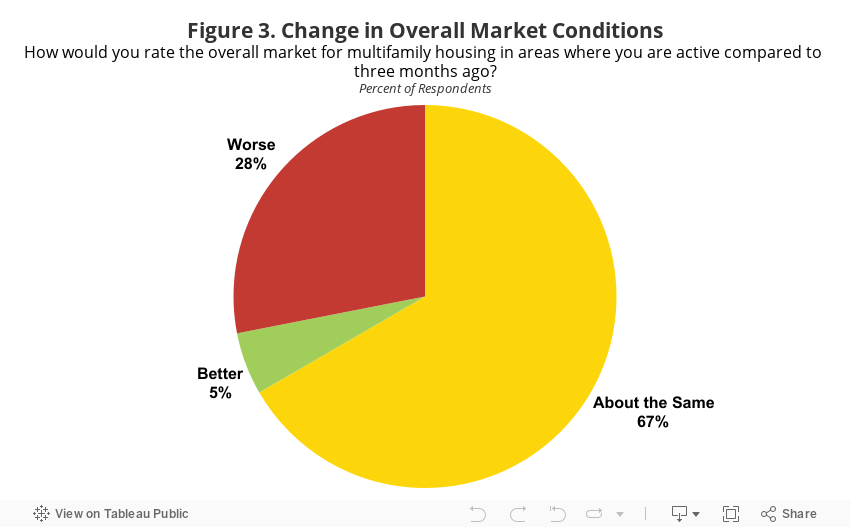

Because the previous version of the MMS series can no longer be used to compare with this quarter’s results, the redesigned tool asked builders and developers to compare market conditions in their areas to three months earlier, using a “better,” “about the same” or “worse” scale. Sixty-seven percent of respondents said the market is “about the same” as it was three months earlier while 28 percent indicated “worse” and 5 percent “better” (Figure 3).

Please visit NAHB’s MMS web page for the full report.

Related

{kind=link}