Those looking to buy a home, along with existing owners, may have come across the term “mortgage rate lock-in effect” lately.

It’s a relatively new phrase that came about thanks to the ultra-low mortgage rates that were available in 2020-2022.

During those years, it was entirely possible to snag a 30-year fixed in the 2-3% range.

In fact, some lucky homeowners might have even got their hands on a mortgage rate that starts with 1.

Here’s the problem – now that rates have doubled, many of these homeowners don’t want to give up their low rate. Or perhaps worse, can’t.

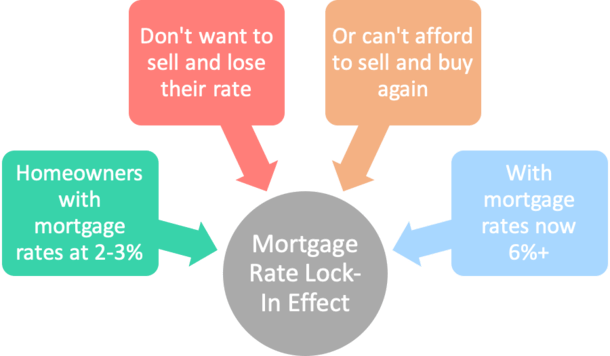

What Is the Mortgage Rate Lock-In Effect?

In a nutshell, the mortgage rate lock-in effect is a phenomenon where borrowers are essentially trapped in their homes thanks to very cheap mortgages.

It’s not exactly a negative, assuming they like their property. But it has been referred to as “golden handcuffs” because it can be somewhat bittersweet.

Basically, folks with mortgage interest rates locked in at 2-3% know they’ve got an amazing deal on their hands.

But if and when they sell, they’ll lose that incredible rate. And worse yet, they’ll have to take on a significantly higher mortgage rate if they buy another home and finance it.

Really the only way to avoid this situation is to sell and rent, or sell and buy a home with cash.

Any other scenario basically results in a doubling of the borrower’s interest rate, from that 2-3% range to 6%+.

Not only is this a tough pill to swallow, it also presents affordability challenges. Especially since home prices haven’t come down all that much.

Remember, there isn’t a negative correlation between home prices and mortgage rates. Both can rise together, or fall together.

Though given the steep increase in mortgage rates lately, there was obviously some downward pressure on home prices, especially in regions of the country that saw big gains.

However, because of this rate lock-in, existing home supply is super limited and has kept home prices elevated.

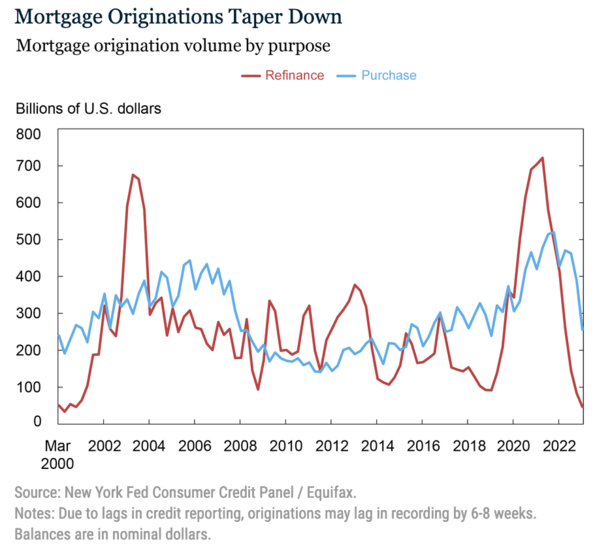

Mortgage Rates Doubled After the Refi Boom

As noted, the 30-year fixed was priced in the 2-3% range a few years ago. It officially hit its lowest point on record during the week ending January 7th, 2021, according to Freddie Mac.

At that time, you could get a 30-year fixed mortgage for 2.65%, and actually even lower if you paid discount points. Or simply shopped around for the best deal.

And that’s exactly what many homeowners did. The so-called “Great Pandemic Mortgage Refinance Boom” resulted in about 14 million new mortgages between the second quarter of 2020 and the fourth quarter of 2021.

Per the Federal Reserve Bank of New York, about five million borrowers extracted a total of $430 billion in home equity via their refinance. These are known as cash out refinances.

Another nine million refinanced their loans without equity extraction and lowered their monthly payments in the process. This is known as a rate and term refinance.

It resulted in a staggering $24 billion in aggregate reduced annual housing costs. And remember, that can be for the next three decades on these 30-year fixed mortgages.

And yes, fixed, meaning the interest rate doesn’t change, regardless of what happens with mortgages in the meantime.

Speaking of, the going rate on a 30-year fixed is now closer to 6.5%, per Freddie Mac.

Can Existing Homeowners Afford to Move?

Now trading in a mortgage priced at 2-3% for one above 6% is clearly unfavorable, especially if the home price doesn’t change much.

This makes a lateral move disadvantageous, and a move-up purchase unlikely.

Moving from one like home to another simply isn’t cost-effective. Let’s consider an example.

Say you purchased a home in 2021 for $500,000, put down 20%, and obtained a 30-year fixed at 2.75%.

That puts the monthly principal and interest payment at $1,632.96. What a deal!

Now imagine you grow tired of your home, or simply want to move for whatever reason. A home you like is going for $475,000. Prices came down a little bit.

You put down 20% and wind up with a loan amount of $380,000, but the mortgage rate is now 6.5%. Ouch!

That puts the monthly principal and interest payment at $2,401.86. What a drag!

Your mortgage payment just increased about $770, or 47%. Yes, you’re reading that right. So not only is it a huge deterrent to move, it’s also potentially unaffordable for some (or many).

This explains why many of today’s homeowners are essentially locked-in to their existing properties.

Either because it makes no financial sense to move, or because it’s not even affordable to do so.

Literally, some homeowners probably couldn’t get approved for a home loan at today’s much higher rates.

But Can’t the Mortgage Rate Lock-In Effect End If Rates Come Down?

Those who don’t buy into this whole mortgage rate lock-in effect argue that life happens. People will move for a variety of reasons, regardless of their low mortgage rate.

While that’s true, it’s unclear how many will move for these reasons. It might be a pretty small percentage of the overall pie.

They also claim that over time, there is a diminishing value to the low-rate mortgage. After all, each time you make a monthly mortgage payment, you have one less at your disposal.

But remember that a 30-year fixed comes with 360 monthly payments. So it’ll take a very long time for that scenario to play out.

What could put an end to the mortgage rate lock-in effect is lower mortgage rates. They don’t necessarily have to be 2-3% again, just something in the ballpark.

So perhaps 30-year fixed rates back in the 4% range would do it. It’d be more palatable for a homeowner to swap a rate of 3% for a rate of 4.5%. And more affordable too!

You could argue that falling home prices would entice people to move, but they’d also have to sell in the process. And it’s unclear if they’d want to take a haircut and lose their low rate.

What would maybe be more likely would be renting out their home and buying another if that were to happen.

This explains why homeowners may be keeping their mortgages for a very long time. And why being locked in can actually be a wonderful thing.

{kind=link}