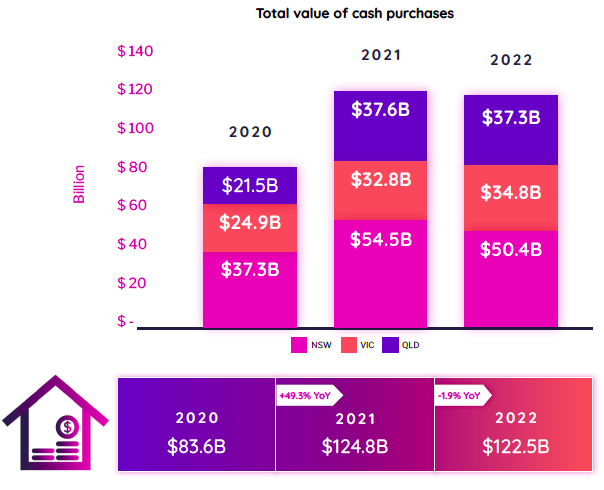

Despite 12 interest rate rises and stubbornly high inflation, a whopping $122.5 billion worth of residential properties were bought using cash across Australia’s eastern states in 2022, adding up to more than a quarter of all residential property transactions, a new report has shown.

Digital and property exchange and data insights company PEXA has released its Cash Purchases report, which reveals statistics on homes that were purchased without a mortgage involved. While the number of properties bought using cash in 2022 was a slight drop from 2021’s $124.8bn, it was still 46.5% higher than compared to the $83.6bn in 2020. NSW notched up the highest total value of cash purchases at $50.5bn in 2022.

Source: PEXA Cash Purchases Report

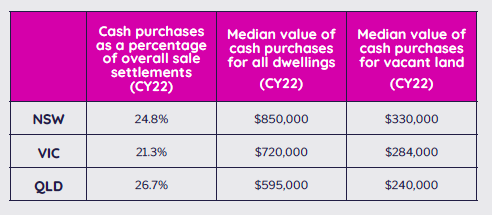

The PEXA report, which highlighted residential property transactions that were funded with cash, also showed that cash purchases accounted for a significant proportion of the total $478.6bn value residential sale settlements last year – the highest was in Queensland at 26.7%, followed by NSW at 24.8% and Victoria at 21.3%. Cash purchases are defined as not having a mortgage registered on the property at settlement and may also include alternative finance sources.

The most popular property type for cash buyers across all states was dwellings (houses and units), followed by vacant land. For overall dwellings, the median value of cash purchases was highest in NSW at $850,000, followed by Victoria ($720,000) and Queensland ($595,000).

Source: PEXA Cash Purchases Report

The report revealed that regional postcodes featured a high proportion of cash purchases in 2022. In Queensland, 65.2% of cash purchases were in regional areas, while in NSW it was 56.3%; Victoria had the lowest proportion of regional cash purchases – 36.8%. The 2021 Census showed that these areas have a higher median age compared to the rest of the state.

Those postcodes also had lower labour force participation and their primary family composition, according to the ABS, was “couple family without children”. When considered together, it suggested that cash buyers were often older Australians moving to the country to retire, PEXA said.

The top three postcodes for cash purchases by percentage in Queensland were Tara 4421 (78.4%), Russell Island 4181 (76.4%) and Gin Gin 4671 (71.9%). In NSW, Emmaville 2371 (73.3%), Gloucester 2422 (65.2%) and Woombah 2469 (62.5%) had the highest percentages, while Yarram 3971 (57.5%), Paynesville 3880 (57.1%) and Metung 3904 (56.9%) ranked highest in Victoria.

PEXA head of research Mike Gill (pictured above) said the PEXA Cash Purchases report shined a light on an often-overlooked segment of the property sector.

“Given these transactions represent more than a quarter of all residential property purchases, it is important to consider that this is a sizeable cohort of buyers who are less impacted by rising interest rates, having not taken out a loan,” Gill said.

“Our research found cash buyers tended to be older and more likely to be buying in regional locations, which does highlight the generational divide between borrowers. Younger homeowners are more likely to have larger home loan balances, particularly those who have purchased recently, whilst many older homeowners are likely to have paid their home loan off or be able to pay cash for a home to retire in.

Gill said as the RBA raised interest rates to slow the economy and fight inflation, the burden fell more toward younger Australians, who were more sensitive to rising rates and less so on older generations “who may in fact benefit if they have savings”.

Urban centres had the highest value of cash purchases, with postcode 4218 (Broadbeach) in Queensland topping the eastern states with $1.33bn spent on cash purchases in 2022 alone. In Sydney and Melbourne, blue-chip metropolitan postcodes 2088 (Mosman) and 3142 (Toorak) topped the rankings, respectively.

The 2021 Census showed that 31% of homes were owner-occupied with no mortgage, as were 30.6% of investment dwellings.

There are a number of reasons why this high degree of activity by cash buyers in the property market is significant:

- cash buyers are not restricted by bank financing considerations regarding the type of property they buy, its size, its location, or its risks

- cash buyers are less directly affected by interest rates and other mortgage costs

- cash buyers are less responsive to Reserve Bank rate hikes, which weakens the efficacy of lifting (or lowering) interest rates in order to tame inflation (or to stimulate demand)

“The demographic profile of cash buyers is different to mortgagee buyers,” the report said.

“They are older, more likely to be buying in regional locations, and more likely to have an international background or connection. This can raise issues about the inter-generational equity impacts of housing affordability, credit availability, and credit costs, particularly in the context of rising home prices and rising interest rates.”

Use the comment section below to tell us how you felt about this.

{kind=link}