One of the many things you have to figure out when you start a new job is the new company 401(k).

Believe it or not, we have lots of clients starting new jobs nowadays. Yes, even amidst all the tech-industry gloom and anxiety, new (and good!) jobs are to be had. And it turns out that one of the most confusing parts of getting a new job—and therefore a new 401(k)—mid-year is, “How much should I contribute to my new 401(k)?”

This is something that our clients ask us about all the time, so let us share with you what we share with them.

Why This Is Hard to Figure Out

The challenge is that, even if you work at two companies and participate in both their 401(k)s during a single calendar year, you are limited to a contribution of $22,500 to a pre-tax or Roth account across both those 401(k)s.

($22,500 is the limit for 2023. It was $20,500 in 2022. And it’ll be even higher next year.)

If you didn’t contribute to your old job’s 401(k), then don’t worry about it! You have the full $22,500 at your disposal in the new job’s 401(k).

But if you contributed some money to your old job’s 401(k), you have to contribute that much less to your new job’s 401(k). It’s not multivariable calculus (that I actually found fun), but it can get confusing.

Ah, the Irony

At Flow, we use Guideline as our 401(k) administrator. Because we use Guideline, our tiny, three-person firm gets access to a really useful tool that most of the Big Boys (ex., Fidelity) don’t offer:

Their website provides a tool that quickly and easily tells you how much you need to contribute per paycheck in order to max out your 401(k) by the end of the year. The tool works whether you’ve contributed to another 401(k) earlier in the year or are starting from scratch.

Surprisingly, Fidelity and all the other 401(k) plan providers that our clients’ giant tech employers use don’t, as far as we can tell, offer anything like this.

Which is why we have our own ugly, in-house Google Sheets calculator for our clients.

Calculating How Much to Contribute Per Paycheck

You can see our calculator, and make a copy if you want. (I don’t have complete confidence that sharing the calculator this way will work. If it doesn’t, then reach out and we’ll send it to you.)

(I had initially written, “… though I imagine the internet is awash in similar calculators.” But then I actually looked and didn’t see any such calculators on the first page of results. There are lots of 401(k) contribution calculators, but they all seem to be of the sort “tell us how much you save to your 401(k) and we’ll tell you how many dollars you’ll have when you retire” or vice-versa.)

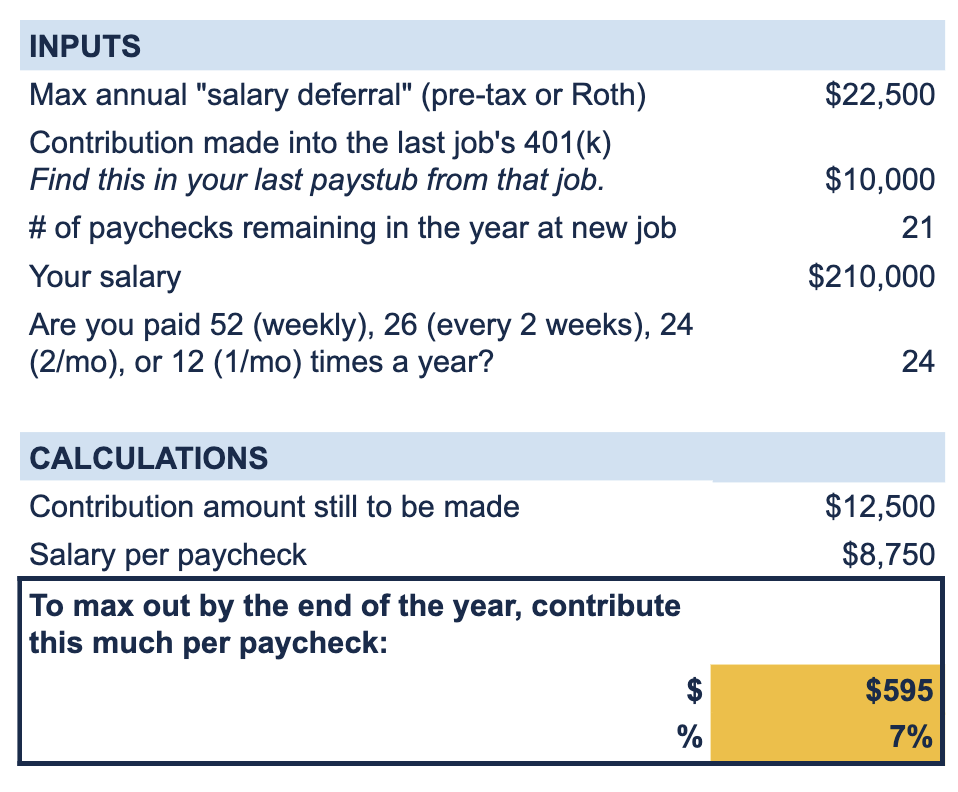

Here’s the non-interactive version of it:

What Does the Calculator Do?

- It figures out how much more money you’re allowed to contribute to your new 401(k) for the rest of the year, based on how much money you contributed to your last 401(k).

- It then calculates how many dollars (or percentage of income) you should contribute to your new 401(k) per paycheck, based on how many paychecks you have remaining in the year and the pre-tax size of each paycheck, in order to reach that $22,500 max by year’s end.

To use the calculator, you need to input several pieces of data that can be deceptively hard to figure out.

- Contribution made into the last job’s 401(k): You gotta know how much you put into your previous company’s 401(k).

You should be able to figure this out by looking at the last paystub from that job. There should be a line item for your 401(k) (maybe two, if you put money into both the pre-tax and Roth accounts), and a “YTD” (year to date) number for it. That’s how much you contributed this entire year thus far into that 401(k).

Here’s a part of a client’s actual paystub. I’ve “circled” the year-to-date contributions into the 401(k) pre-tax and Roth. This paystub even has a third contribution line item: contribution from a bonus!

This client has so far contributed $5,979.16 to their 401(k) and therefore can contribute another $22,500 – $5979.16 = $16,530.84. (Dear God, let my arithmetic be right.)

- # of paychecks remaining in the year at new job and Are you paid 52 (weekly), 26 (every 2 weeks), 24 (2/mo), or 12 (1/mo) times a year?: This is kinda tricky. You have to know the frequency with which you get paid, which hopefully you do, or will soon after starting the new job.

Most likely you get paid either every two weeks (26 times/year) or twice per month (24 times/year). For example, if you get paid twice per month and start contributing to your new 401(k) on August 1, then you have 5 months and therefore 10 paychecks remaining.

- Your salary: You’d be surprised how many people don’t know their salaries, but hopefully if you’re just starting a new job, that offer letter is still fresh in your mind.

Random Notes

Once you start digging, 401(k)s offer up boundless complexity. Here’s a smattering of related tidbits to keep in mind:

- Let’s say you contribute more to this new 401(k) than you should, and your total contribution across both 401(k)s is over $22,500. It’s not the end of the world. You will need to remove the “excess” contributions after the end of the year, which you’ll find out at least when you do your taxes.

This can be an administrative hassle, so ‘tis better to not run afoul of this. Any mistake in the world of financial bureaucracy can easily turn into a nightmare for no damn good reason.

- We have had some clients who had an employer/HR department that helped them figure out the remaining 401(k) contribution. If you’re lucky enough to work at such a company, great! No need to do your own calculations. Understanding what’s happening would still be good, though.

- We’ve been talking about this $22,500 cap. Technically, your real 401(k) contribution cap is $66,000 (in 2023), not $22,500. That additional $43,500 can be put into your 401(k) by your employer (most commonly by way of a match) or by you, if your 401(k) plan allows after-tax contributions.

Interestingly enough, if you have more than one 401(k) in the course of one year, you can contribute that $22,500 only once across all your 401(k)s, but you can contribute up to the $66k limit in every single 401(k).

In practical terms, this probably isn’t all that useful. You’d have to have two (or more) 401(k)s, each permitting after-tax 401(k) contributions, you’d max out $22,500 only once, and then contribute up to $66k in each of your 401(k)s. (This situation is finicky and there are lots of rules, so I’m only giving a vague nod to the possibilities here.)

- If you’re 50 years old or older, that $22,500 is instead $30,000 and that $66,000 is instead $73,500.

- I recommend setting a calendar reminder for yourself near the end of the year, when you have a couple of paychecks left. At that time, I recommend looking at how much you’ve contributed to both your 401(k)s so far that year, and make adjustments (up or down!) if you’re not going to hit that $22,500 max in the last paycheck of the year.

When you start a new job, you’ve got a ton of things to figure out, most important of which is your actual job. Thankfully, you might be able to reasonably wait a few paychecks to really figure out your new 401(k).

Oh, and congratulations on the new job!

Do you want to work with a financial planner who can help you figure out frustrating, nitty-gritty details? Reach out and schedule a free consultation or send us an email.

Sign up for Flow’s twice-monthly blog email to stay on top of our blog posts and videos.

Disclaimer: This article is provided for educational, general information, and illustration purposes only. Nothing contained in the material constitutes tax advice, a recommendation for purchase or sale of any security, or investment advisory services. We encourage you to consult a financial planner, accountant, and/or legal counsel for advice specific to your situation. Reproduction of this material is prohibited without written permission from Flow Financial Planning, LLC, and all rights are reserved. Read the full Disclaimer.

{kind=link}