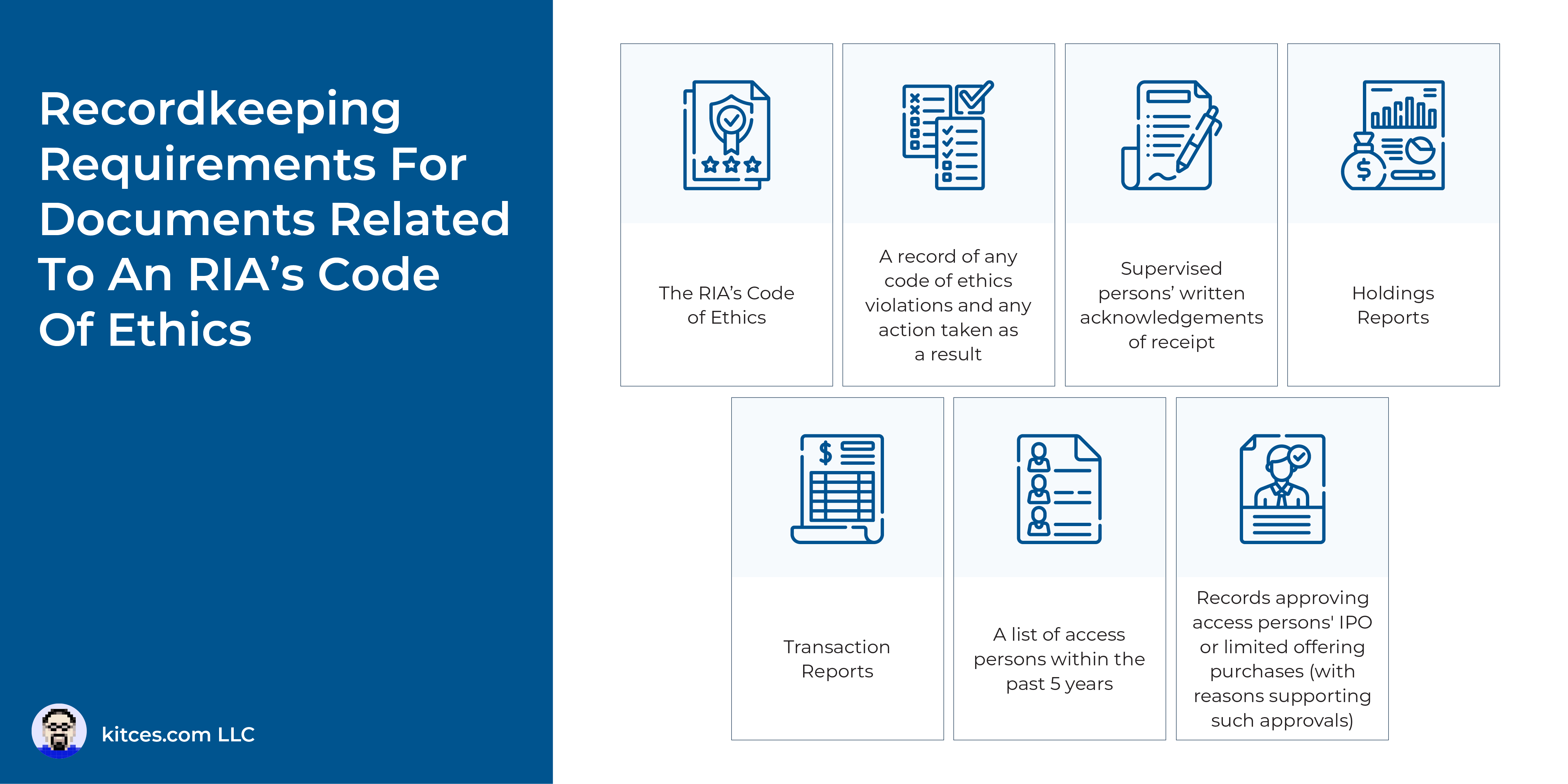

All investment advisers are fiduciaries that owe a duty of care and loyalty to their clients, and, in an ideal world, advisory firms and their staff would abide by these requirements without the need for a prescriptive code of ethics. However, the early 2000s were plagued by a variety of SEC enforcement actions that alleged fiduciary duty violations – primarily involving trading abuses by investment advisory personnel – which led the regulator to create a rule (that became effective in 2004) requiring all SEC-registered investment advisers to adopt and enforce a written code of ethics applicable to its supervised persons. The SEC’s Investment Adviser Codes of Ethics Rule requires all SEC-registered investment advisers to establish, maintain, and enforce a written code of ethics that, at a minimum, includes 5 areas: 1) listing standards of business conduct; 2) complying with applicable Federal securities laws; 3) requiring access persons to report their personal securities transactions and holdings for review; 4) reporting violations; and 5) distributing and acknowledging receipt of the firm’s code of ethics. While most of the Rule’s requirements are relatively straightforward, there are detailed nuances that IAR advisers must be familiar with to enforce their own codes of ethics pursuant to the SEC’s rule.

As a starting point, investment advisers must address 3 important questions when designing and implementing a compliant code of ethics: who within the firm is subject to reporting their personal securities transactions; what information needs to be reported; and when this information must be reported. “Access persons” are defined as “supervised persons” with access to nonpublic information regarding any clients’ purchase or sale of securities or regarding the portfolio holdings of any reportable fund, or is involved in making securities recommendations to clients, or who has access to such recommendations that are nonpublic. Such individuals are required to submit both holdings reports (within 10 days of first being deemed an access person and at least once in each 12-month period) as well as transaction reports (within 30 days of the end of each calendar quarter) for reportable securities that they or immediate family members beneficially own. Notably, these are just minimum requirements for the firm’s code of ethics and the SEC suggests that firms consider other areas for potential inclusion (e.g., “Blackout periods” when client securities trades are being placed or recommendations are being made and access persons are not permitted to place their own personal securities transactions).

In addition to collecting the required reports, the firm’s Chief Compliance Officer (CCO) also has certain review requirements. For instance, the CCO should be on the lookout for access persons who are placing their own interests ahead of clients, usurping client investment opportunities for their own personal benefit, or otherwise managing their own personal investments in such a way that does not reflect their fiduciary duties to clients.

Ultimately, the key point is that an investment adviser’s code of ethics is not just a pro forma document, but rather a key part of ensuring that the firm is living up to its fiduciary duty to its clients. Which not only sets expectations regarding ethics for the firm’s leadership and staff, but also gives prospective and current clients more confidence in the level of care they can expect to receive when working with the firm!

{kind=link}