Magenta Therapeutics (MGTA) ($39MM market cap) is a member of my broken biotech basket, I’m bringing it forward again to highlight the opportunity for shareholders to vote down the proposed reverse merger with privately held Dianthus Therapeutics. In MGTA’s S-4, the company strongly hints that if the deal is not approved, a dissolution and liquidation is on the table:

If the merger is not consummated, Magenta’s board of directors may decide to pursue a dissolution and liquidation. In such an event, the amount of cash available for distribution to its stockholders will depend heavily on the timing of such liquidation as well as the amount of cash that will need to be reserved for commitments and contingent liabilities.

There can be no assurance that the merger will be completed. If the merger is not completed, Magenta’s board of directors may decide to pursue a dissolution and liquidation. In such an event, the amount of cash available for distribution to its stockholders will depend heavily on the timing of such decision and, with the passage of time the amount of cash available for distribution will be reduced as Magenta continues to fund its operations. In addition, if Magenta’s board of directors were to approve and recommend, and its stockholders were to approve, a dissolution and liquidation, Magenta would be required under Delaware corporate law to pay its outstanding obligations, as well as to make reasonable provision for contingent and unknown obligations, prior to making any distributions in liquidation to its stockholders. As a result of this requirement, a portion of its assets may need to be reserved pending the resolution of such obligations and the timing of any such resolution is uncertain. In addition, Magenta may be subject to litigation or other claims related to a dissolution and liquidation. If a dissolution and liquidation were pursued, Magenta’s board of directors, in consultation with its advisors, would need to evaluate these matters and make a determination about a reasonable amount to reserve. Accordingly, holders of its common stock could lose all or a significant portion of their investment in the event of liquidation, dissolution or winding up.

Included in the S-4 is also a management prepared liquidation analysis (the distribution estimate here assumes a May or June 2023 distribution, clearly that’s not a realistic timeline, additional liquidation costs will be incurred if MGTA does end up down that road):

In light of the foregoing factors and the uncertainties inherent in estimated cash balances, stockholders are cautioned not to place undue reliance, if any, on the Liquidation Analysis.

The below summary of the Liquidation Analysis is subject to the statements above, and it represents Magenta management’s estimates of Magenta’s cash which may be distributed to stockholders as permitted under applicable law pursuant to a plan of dissolution.

Key assumptions underlying the Liquidation Analysis included (i) that the entire distribution of Magenta’s net cash would be made in either May 2023 or June 2023, (ii) that Magenta would have approximately $65.2 million and $63.9 million of net cash as of May 2023 and June 2023, respectively, after deducting costs and expenses, including legal fees, the fees payable to Magenta’s strategic financial advisor, accounting fees, employee retention bonuses, severance and benefits, insurance expenses and other transaction-related costs, with no adjustments for taxes; (iii) that these costs and expenses were forecasted to total approximately $11.8 million assuming the closing of a liquidation in each of May 2023 and June 2023; and (iv) approximately 60.7 million total shares outstanding as of April 27, 2023. The analysis resulted in an estimated cash distribution per share in May 2023 and June 2023 of $1.07 per share and $1.05 per share, respectively.

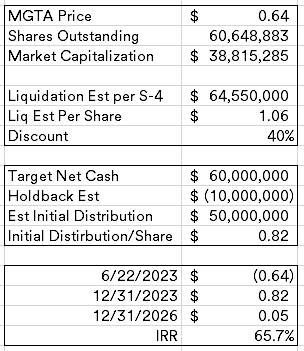

Today, shares trade for $0.64 per share, well below management’s liquidation estimate. There’s a reasonable presumption a liquidation would indeed follow a “no” vote to the merger, per the merger agreement, MGTA would be required to pay a termination fee of $13.3MM (huge in comparison to their cash balances or market cap) if MGTA enters into another merger within 12 months.

Termination Fees Payable by Magenta

Magenta must pay Dianthus a termination fee of $13.3 million if (i) the Merger Agreement is terminated by Magenta or Dianthus pursuant to clause (e) above or by Dianthus pursuant to clause (f) above, (ii) at any time after the date of the Merger Agreement and prior to the Magenta special meeting, an Acquisition Proposal with respect to Magenta will have been publicly announced, disclosed or otherwise communicated to the Magenta board of directors (and will not have been withdrawn), and (iii) in the event the Merger Agreement is terminated pursuant to clause (e) above, within 12 months after the date of such termination, Magenta enters into a definitive agreement with respect to a subsequent transaction or consummates a subsequent transaction.

A liquidation would be their only realistic option, 12 months is a long time to wait it out for a cash burning biotech with no pipeline (they sold all their assets in April). In order to close the deal, MGTA needs a majority of the votes cast to vote in favor of the merger, the support agreement only has 6.9% of the shares, leaving quite a bit of ground to cover. Tang Capital Management owns just under 10% and presumably is the Investor named in the background section of the S-4 who proposed a cash tender offer:

Between March 1, 2023 and March 28, 2023, a stockholder of Magenta (the “Investor”) made several unsolicited inquiries to Stephen Mahoney, the President, Chief Financial and Operating Office of Magenta, to inquire whether Magenta would have an interest in the Investor proposing a cash tender offer for Magenta at a discount to its current cash position. No specific proposal, terms or valuation were discussed during this conversation, or any subsequent conversation between the Investor and representatives of Magenta.

It is unlikely that Tang would vote in favor of the reverse merger at this point, given the current discount to cash. I’m guessing it will be challenging for management to get the 50% of the vote necessary, but as we’ve seen in other microcaps, getting investors to vote at all could be an issue. A non-vote here doesn’t impact the vote one way or another, likely benefitting management.

MGTA’s target net cash position at the time of closing (Q3) per the merger agreement is $60MM, if we assume that the vote fails and MGTA pursues a liquidation, let’s guess that they holdback $10MM for additional winddown expenses or contingencies.

Above is my potential IRR math, I’m assuming an initial distribution by year end and then a small one ($3MM of the $10MM holdback) in 3 years. In addition, the company did sell their pre-merger assets in April, $20MM in combined milestone payments are in play too, but I’m assuming those are worthless. The merger vote hasn’t been set yet, but I would expect it in early-mid Q3. I bought more recently.

Disclosure: I own shares of MGTA