In times of economic volatility, some sectors are more resilient than others. One of them is the food industry, as food is ultimately one of these items we HAVE to spend on.

This is obviously a very diverse sector, and this article will try to provide an overview of the many possibilities for investing in the food industry.

Best Food Stocks

We might buy a car every 5 to 10 years, but we eat three times a day. And even when times are tough, food is the last thing we cut back on.

So let’s look at the best food stocks.

These are designed as introductions, and if something catches your eye, you will want to do additional research!

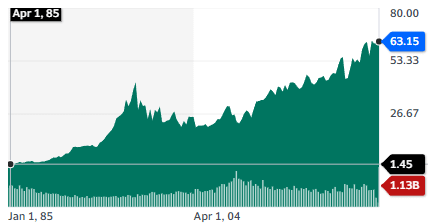

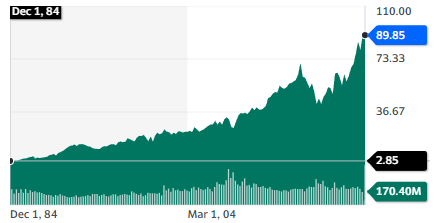

1. Coca-Cola (KO)

| Market Cap | $273.1B |

| P/E | 28.19 |

| Dividend Yield | 2.88% |

A famous favorite stock of Warren Buffett (Berkshire Hathaway owns 9% of KO) and an equally legendary compounding stock. It has a rich history and even an array of urban legends about the drink containing cocaine or how secret its formula is.

While the group takes its name from the famous Coca-Cola drink, it is now a massive corporation holding a very large array of 200 brands and the world’s largest nonalcoholic beverage company.

The company is licensing 225 bottling companies with 900 bottling plants to produce the final products from concentrates they buy from KO.

Coco-Cola grew its earning per share by 6% on average over the last five years, and free cash flow rose by an average of 14% a year. The company is often referenced as a solid example of a stock with a strong moat in the form of a brand supported by multiple decades of marketing and product placement.

Revenues are highly diversified and international, with North America representing just a third of total sales.

This stock is pretty much as safe as it gets and also gives a modest but stable and growing dividend. So it is mostly favored by long-term investors looking for safety and a dividend reinvestment opportunity.

2. Tyson Foods, Inc. (TSN)

| Market Cap | $17.8B |

| P/E | 11.99 |

| Dividend Yield | 3.83% |

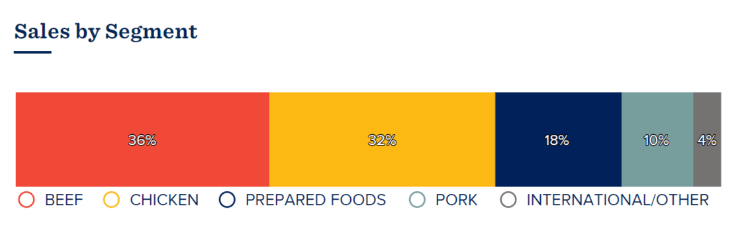

Tyson is one the largest food companies in the world and a leader in protein. Tyson holds 33 different brands, with many of them recognizable by any American.

Most of the activity comes from meat sales, with 2/3 being beef and chicken. Tyson is also investing in potential new sectors and competitors, like lab-grown meat and meat-free alternatives, through its Tyson Ventures branch. The same Tyson Ventures is also investing in other innovations (robotics, carbon marketplace, genomics) and leather production.

The company gave a warning that Q2 2023 would be “more challenging” than Q1, with “All three protein categories impacted by unfavorable market conditions

simultaneously.” So it seems that the looming recession and rising interest rates are affecting Americans’ spending on meat.

Rising commodity prices, including for animal feed, have not helped either.

Whether this is a durable issue or a temporary hiccup will determine if the stock is undervalued or not at 2023 prices. Still, the company is planning international expansions, with 11 new plants planned to open in the next two years.

Tyson Foods is a stock that will attract investors confident in the long-term popularity of meat products and interested in buying it at a (temporary?) lower price and holding it for many years.

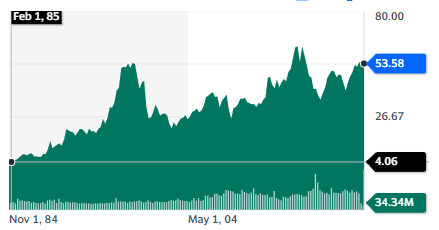

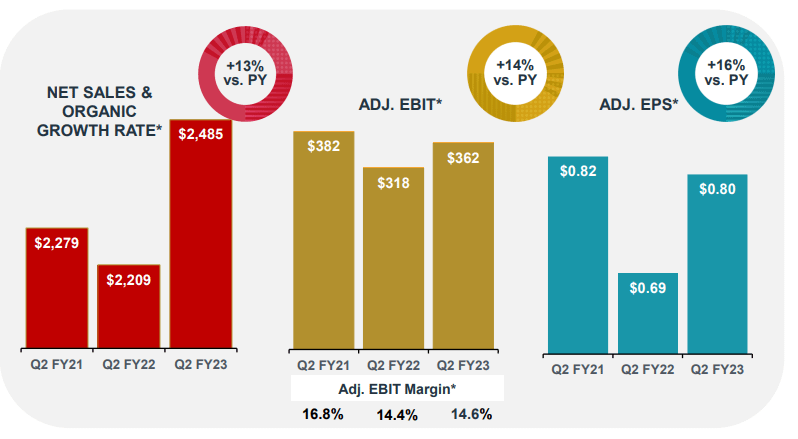

3. Campbell Soup Company (CPB)

| Market Cap | $16B |

| P/E | 19.70 |

| Dividend Yield | 2.78% |

While the company started in the soup business, it is now producing 15 meal and beverage brands and nine snack brands. It specializes in premade meals and convenience foods.

Some of the brands were obtained through acquisition, notably the large selection of snack brands of Snyder’s-Lance, Inc. in 2018 and Pacific Foods in 2017.

Campbell is focused on North America exclusively and registered remarkable sales growth in 2022. Earnings are more volatile due to rising input costs, a recurring theme in the food industry in 2022 and 2023.

While it lacks the size and growth profile of KO, it shares a lot of similarities with Buffett’s favorite stock. The company has a history of successful brand launches or acquisitions and has proven to be a quality compounder. Its smaller size also might give it more room to keep growing.

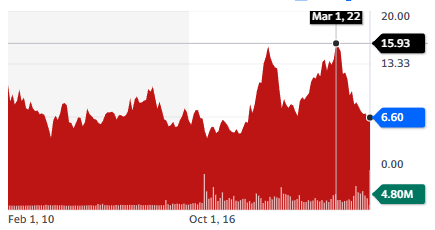

4. JBS S.A. (JBSAY)

| Market Cap | $7.3B |

| P/E | 2.38 |

| Dividend Yield | 11.75% |

The Brazilian leader in meat production, JBS is a larger company than its market capitalization would suggest. It controls 150 brands, as well the production of leather, biodiesel, soap, purified ingredients, supplies for the pharmaceutical industry, packaging, a trading division, and a logistics fleet of 1,100 trucks.

It is the world’s largest beef producer, chicken producer, and second to largest pork producer. It is also the second-largest salmon producer in Australia. It is the leading producer of plant-based meat alternatives in Brazil and the third-largest in Europe. It’s also in first place for prepared meals in the UK, Australia, and New Zealand and second in Brazil.

By revenue, JBS is larger than the better-known known Nestle, Pepsico, or Tyson.

The company has been hit by decreased meat consumption in the same way as Tyson Foods, but also by the generally negative outlook of markets about Brazil since President Lula’s election.

JBS is suitable for investors willing to tackle a lot of international risk and volatility in exchange for a very low valuation as measured by P/E and dividend yields.

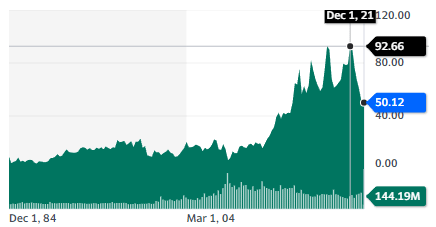

5. General Mills, Inc. (GIS)

| Market Cap | $52.8M |

| P/E | 19.49 |

| Dividend Yield | 2.39% |

General Mills is another household name with 46 brands, including Cheerios, Cocoa Puff, Haagen Dazs, Old El Paso, and Yoplait, and even pet food with Blue Buffalo.

The company has grown, year-to-date in 2023, operating profits by 11% and earnings per share by 14%. The company is looking at an improving 2023 outlook of 8-9% EPS growth.

Overall, despite inflationary pressure, General Mills seems to be handling the macroeconomic environment pretty well.

Cash redistributed to shareholders comes in 2 forms, in dividends but also the same amount in share repurchases for 2022. So considering both, the real yield of the company is much higher than the visible 2-3% dividend yield.

This stock has the profile of a high-quality food stock, with highly valuable brands and a compounding stock price. And its compounding profile over the last four decades is remarkable and rather equal to KO, even if it is less discussed.

6. The Kraft Heinz Company (KHC)

| Market Cap | $47.7B |

| P/E | 19.85 |

| Dividend Yield | 3.98% |

Kraft is a well-known maker of sauces, ketchup, and “easy” food like Mac & Cheese.

It is also a company that got into trouble in 2019 when it wrote off $15B in value for underperforming brands. The situation was blamed on a failure to innovate and poor strategy focusing too much on heavily processed and unhealthy industrial foods.

This was also at the time when “new foods” were expected to take over the market by storm.

The company has faced many challenges, including accounting issues, the resignation of its CEO and a slide in sales and earnings as people look to eat fewer heavily processed foods and embrace plant-based products from the likes of Beyond Meat (BYND) and Impossible Foods.

Concerns might have been exaggerated, even if the stock is still to recover. For example, the “ongoing business growth” segment (brands that have been kept since 2019) has managed a 9% CAGR. The “energize” segment saw a 6% CAGR since 2019, and the “stabilize” segment has been flat at 0%.

Looking at sales numbers, it is hard to fully see a company so much less valuable in 2022 than in 2019.

The new management is centering the company around two segments, which makes a lot of sense for a food business. Taste, with various sauces, and convenience, with easy and quick-to-make meals.

This renewed focus should help the company make better strategic decisions and restart growth.

Kraft is not for every investor, as the last 3-4 years’ stock performance has been abysmal compared to its competitors. But it is also a company that seems to have been radically energized and reformed by the crisis. So it could be a turnaround story with a lot more growth potential than what the markets are pricing in.

Best Food ETFs

If you prefer to have exposure to the sector as a whole, there are several food-focused ETFs available.

1. First Trust Nasdaq Food & Beverage ETF (FTXG)

This ETF has a focus on the largest companies, with the top 5 holdings representing 40% of the whole ETF: Mondelez, General Mills, PepsiCo, Coca-Cola, and Archer-Daniels-Midland.

2. Invesco Dynamic Food & Beverage ETF (PBJ)

This ETF invests in the 30 largest companies in the food sector (Mondelez, General Mills) as well as in beverages (PepsiCo, Molson Coors) as well as agriculture (Archer-Daniels-Midland).

3. VanEck Future of Food ETF (YUMI)

This ETF is focused on food and agricultural innovations. Its top 4 holdings are Ingredion, Corteva, Deere & Co, and Novozymes. It contains fertilizer stocks as well, like Nutrien. It is a great ETF for investors looking for exposure to the sector beyond consumer brands.

Conclusion

Food is a very profitable sector, especially when supported by strong brands. Habits and marketing can make one person a lifetime consumer of this specific product. This is one of the main reasons behind the strong historical performance of food stocks.

With this stock list, it is possible to build a portfolio gathering hundreds of high-quality brands through proven compounded stocks, together with a low-digit dividend yield. And with potential turnarounds like Kraft-Heinz or hammered-down foreign stocks like JBS, it is also possible to increase yields.

{kind=link}