The Indian stock markets hit all-time highs on Friday (July 14, 2023). The bellwether indices Nifty 50 and Sensex closed above 19,500 and 66,000, respectively.

If your portfolio had a decent equity allocation, you would be a happy investor today. Your portfolio must be showing healthy gains. However, your investment journey is not yet complete. A bigger question bothers you: What to do now? How to invest when the markets are at all-time highs?

- Should you sell all (or a part) of your portfolio and reinvest when the market falls? OR

- Should you stop SIPs and restart when the markets have corrected? OR

- Should you do nothing, sell nothing, and let the SIPs continue?

There is no black and white answer to this. We will know the CORRECT answer only in the future. Say 3 to 5 years from now. However, in this post, I will try to share what according to me is the RIGHT approach in such situations. Note my definition of the RIGHT investment approach may be different from yours.

For me, the RIGHT approach is the one that is easy to execute and stick with, is less mentally exhausting, and offers satisfactory returns. Good enough to help me reach my financial goals. I do not try to time the market (nor do I have the skills to do that). I do not lose sleep trying to get the best out of the markets. And I am fine with my neighbour earning better returns than me.

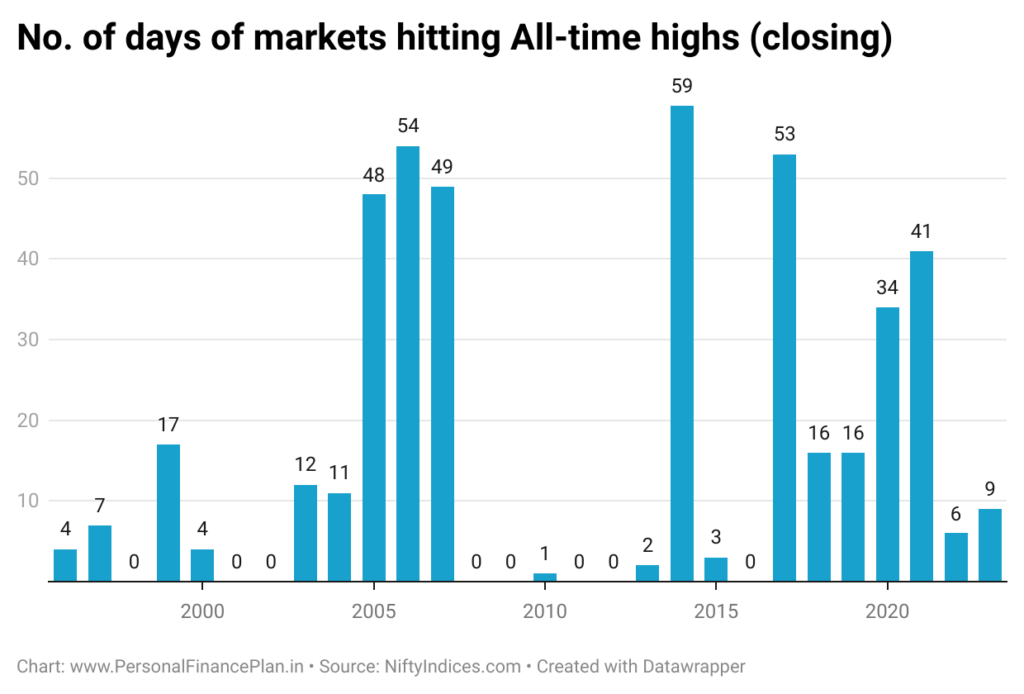

Market hitting all-time highs is not uncommon

Happens more often than you would imagine.

Expected too, isn’t?

After all, Nifty 50 has gone from ~1,500 since the turn of the century to 19,500. Ditto with Sensex that has moved from ~5,000 at the end of 1999 to 66,000 today. So, these indices have gone up 13X. That’s not possible without markets hitting all-time highs regularly.

I wrote this post in March 2021 when Sensex hit 50,000 for the first time. We are up 30% in 27 months since then. Not bad at all.

We have hit an all-time high on Nifty 50 atleast once in 17 out of the last 24 years. Pretty frequent, right? The years when we didn’t hit an all-time high even once are 2001, 2002, 2008, 2009, 2011, 2012, and 2016. And in the years when the markets have reached the all-time highs, they have not broken the peak just once.

What have been the returns like when investing at an all-time high?

I looked at 1-year, 3-year, 5-year, 7-year returns from the date markets hit all-time highs (closing).

*Past performance, as you see in the historical data above, may not repeat.

You can see that the returns are NOT that bad. Average past returns (from all-time highs) for medium to long term range from 9% to 11% p.a.

Yes, this performance may NOT be exciting for some of you.

However, my experience is that selling at all-time highs is just not a problem. It is quite easy. You must have made money with all your investments (let’s ignore taxes for now). The problem is how to get back in. If you sell at all-time highs planning to get back in when the markets fall, when do you invest those amounts back?

- If the markets start rising, you wouldn’t invest. After all, you sold at lower levels.

- If the markets take a sharp U-turn and start falling, the market commentary will likely turn adverse. You may be scared to invest and may want to wait until everything “normalizes”. Then, the markets would suddenly reverse, and you go to (1).

If you have lived through these emotions, when do you invest back this money?

You may not behave in this manner, but I think many investors do. Timing the markets (frequent buying and selling) is not easy and is not for everyone. Certainly not for me. Missing the best day, the best week, or the best month of the year can adversely affect long term returns.

When you invest in stock markets, you are not just fighting against the stock markets. In fact, you are not fighting markets at all. The price of stock or the stock markets will take a trajectory of its own. You can’t control that. You fight a much fiercer battle against your emotions and biases. That’s where most of the investment battles are won or lost. It is easy to say, “I am a long-term investor and do not care about short-term volatility”. You hear this more often when the times are good. However, when the tide turns and markets struggle for an extended period, your patience gets tested. That’s when you go back and question your investment choices. And perhaps make choices that you would regret in the future.

The events happening around you can affect your conviction and approach towards investments, risk, and reward. This is why, despite all the talk about value investing, most investors come into the markets when the markets are rising. And the investors shun the markets when the markets are struggling (value investing would suggest otherwise).

Let Asset Allocation be your guide

When you work with an asset allocation approach to investments, you will automatically get answers about when and how much to sell. You do not have to rely on your guts.

When the markets hit all-time highs, the equity allocation in your portfolio also rises. It is possible that your equity allocation has breached the rebalancing threshold. If that happens, you rebalance the portfolio to target asset allocation. Until the rebalancing threshold is hit, you don’t do anything.

On the other hand, when the markets fall, the equity allocation falls. When the rebalanced threshold is hit, you rebalance to target allocation.

It is that simple.

In investing, simple beats complex.

By the way, don’t think of this as a conservative approach. Regular portfolio rebalancing can reduce portfolio volatility and improve portfolio returns. More importantly, it reduces the mental toll, helps you retain sanity, and stick with investment discipline. And yes, there is no such thing as the best asset allocation. You must select a target asset allocation you can live with.

If you leave your investment decisions to your guts, you will likely mess up. I reproduce this excerpt from one of my old posts.

///////////////////////////////////////////////////////////////////////////////////

You will either sell too much too soon. OR buy too much too late.

While it is impossible to remove biases from our investment decision-making, we can certainly reduce the impact by working with some rules. And asset allocation is one such rule.

For most of us, over the long term, rule-based investments (decision-making) will do a far better job than gut-based decision making.

Selling all your equity investments (just because you feel markets have gone up too much) and waiting for a correction is likely to be counterproductive over the long term.

Similarly, increasing equity exposure sharply (after a market correction) can backfire. Further corrections may await. Or the market may stay rangebound for a few years. This is an even bigger problem when you are talking about individual stocks (and not diversified indices). You may well end up averaging your stock down to zero. Of course, it can be an immensely rewarding experience too, but you need to appreciate the risks. And when you let your guts decide, risk appreciation usually takes a backseat.

Instead, if you just tweak your asset allocation (or rebalance) to the target levels, you are never completely in or out of the markets. You do not miss the upside. Thus, you will never feel left out (No FOMO or Fear Of Missing Out). And corrections do not crush your portfolio completely either. You will not be too scared during a market fall. Thus, it is also easier to manage emotions. And this prevents you from making bad investment choices.

//////////////////////////////////////////////////////////////////////////////////////

There is no perfect approach

- You do not have to optimize all the time. It is ok to sit back and relax and do nothing. Action is not always better.

- To be happy with your investment performance, you do not have to sell everything before the markets fall. And go all in before the markets rise.

- Managing emotions is super critical. If you are too concerned that the fall in the markets will wipe off your notional gains, it is ok to sell a small portion (say 5%) of your equity portfolio. Yes, this will create friction in the form of taxes and affect long-term compounding. However, if this helps you take care of your restlessness and lets you sleep peacefully at night, so be it. In my opinion, you will make lesser investment mistakes with a calm mind.

- If you are investing by way of SIPs, you are anyways not putting all your money at one time. You are putting money gradually. Even if the markets were to correct sharply, your future SIP installment would go at lower market levels. Hence, continuing with SIP (when the markets are at all-time highs) is an easy decision, at least for me.

How are you approach the recent all-time market highs? Do let me know in the comments section.

Source and Additional Read

Data Source: NiftyIndices.com

Investing at 52-week highs vs. Investing at 52-week lows

Disclaimer: Registration granted by SEBI, membership of BASL, and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors. Investment in securities market is subject to market risks. Read all the related documents carefully before investing.

Note: This post is for education purpose alone and is NOT investment advice. This is not a recommendation to invest or NOT invest in any product. The securities/instruments/indices quoted are for illustration only and are not recommendatory. My views may be biased, and I may choose not to focus on aspects that you consider important. You may be in a different life stage than I am in. Hence, you must NOT base your investment decisions based on my writings. There is no one-size-fits-all solution in investments. What may be a good investment for certain investors may NOT be good for others. And vice versa. Therefore, read and understand the product terms and conditions and consider your risk profile, requirements, and suitability before investing in any investment product or following an investment approach.

{kind=link}