There’s been a lot of speculation that home prices would crash as mortgage rates surged.

The argument was especially convincing after the 30-year fixed climbed from around 3% to over 7% in less than a year.

This was unprecedented movement, even if mortgage rates remain below those crazy double-digits from the 1980s.

Sure, they are still low historically, at around 6/7%, but the doubling in less than 12 months is what you need to pay attention to.

Going from 12% to 15% isn’t fun either, but it’s not as much of a payment shock percentage-wise.

Do Higher Mortgage Rates Mean Lower Housing Prices?

At first glance, you’d think that mortgage rates and home prices have an inverse relationship.

In that if one variable goes up, the other must come down. And vice versa. So if mortgage rates shoot higher, home prices must tumble lower.

But here we are, looking at new all-time highs for home prices while the 30-year fixed averages nearly 7%.

How is it possible that both home prices and mortgage rates rose in tandem?

Well, for one, history reveals that they aren’t negatively correlated. In other words, they can rise together, or fall at the same time.

As to why, remember how mortgage rates are determined. Much of their direction is based on the health of the economy.

At the moment, the economy is strong, if not too strong, which is why the Fed began tightening the screws and raising its own fed funds rate in the first place.

This was meant to cool off the overheated housing market, which was experiencing unprecedented demand.

And it seemed to work, pushing home price appreciation back to much more normal levels, instead of double-digit annual gains.

However, the Fed could really only fiddle around with the demand side of things. By that, I mean cool demand by making mortgage financing more expensive.

And they accomplished that goal. There’s a lot less demand out there, whether it’s driven by a lack of affordability or just less willingness to buy at this combination of prices/rates.

But the Fed can’t really do anything about the supply piece, which is the other key part of the equation.

They can attempt to rein in inflation with monetary policy, but they can’t build more homes.

Unfortunately, low inventory was an issue before the Fed got involved. So their attempt to tame the housing market might be in vain, at least partially.

This might also explain, why despite markedly higher mortgage rates, the typical U.S. home value surpassed $350,000 for the first time ever in June.

Per Zillow, national home prices increased 1.4% from May to June, their fourth monthly gain in a row.

That put the typical home at $350,213, nearly 1% above the price seen the previous June, and just enough to beat out the old Zillow Home Value Index (ZHVI) record set last July.

It’s All About the Inventory, or Lack Thereof

If we shift our attention away from mortgage rates, and instead focus on available inventory, the current state of the housing market begins to make a lot more sense.

When you realize there are virtually no homes for sale, it begins to explain why home prices are up in spite of near-7% mortgage rates.

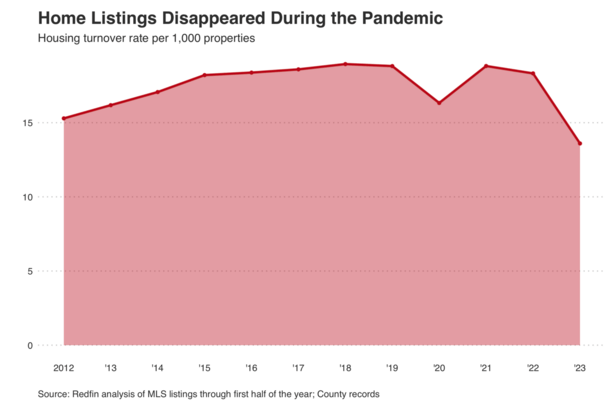

The latest piece of data on the inventory front comes courtesy of Redfin, which reported that the turnover rate is the lowest it has been in at least a decade.

This is defined as the number of homes that are listed divided by the total number of sellable properties that exist in a given area.

It includes all residential properties, including single-family homes, condos/townhouses, and 2-4 unit properties.

Just 14 out of every 1,000 U.S. homes changed hands during the first half of 2023, compared to 19 of every 1,000 during the same period in 2019.

Looked at another way, prospective home buyers have 28% fewer homes to choose from versus four years ago.

And it was already slim pickings back then, before the pandemic upended the U.S. housing market.

California appears to be the hardest hit, with roughly six of every 1,000 homes in San Jose selling this year. Similar low turnover rates can be found in nearby Oakland, as well as down south in San Diego.

They add that the “pandemic homebuying boom depleted supply, and it hasn’t been replenished because homeowners are hanging onto their relatively low mortgage rates.”

This is known as the mortgage rate lock-in effect, or golden handcuffs to some.

Simply put, homeowners can’t (due to affordability) or are unwilling (due to the price disparity) to give up their current 2-3% mortgage rate.

As such, existing home supply is basically nonexistent. And the only supply in town is coming via the home builders, who incidentally are enjoying this odd dynamic at the moment.

Last week, the National Association of Realtors 2023 Member Profile revealed that a shortage of housing supply was the biggest impediment to their clients buying a home.

NAR also noted that housing inventory fell to the lowest level recorded since the year 1999.

Home Prices Defying Gravity Thanks to Low Supply

Zillow said there were 28% fewer new listings this June versus last June. We’ll find out soon if inventory gets even worse.

But they added it might be “the low water point for year-over-year comparisons in new listings” because inventory plunged last July.

So we might not see as many startling headlines regarding low supply since it’ll be hard to go much lower, at least relative to recent readings.

Regardless, it’s clear that a lack of supply, well below healthy levels of 4-5 months, is allowing home prices to defy gravity as interest rates remain elevated.

This differs tremendously from the boom years of the early 2000s, when there was an oversupply of homes (8-9 months), similar mortgage rates, and exotic financing to boot.

It also explains why home prices aren’t dropping, despite much higher mortgage rates and poor affordability.

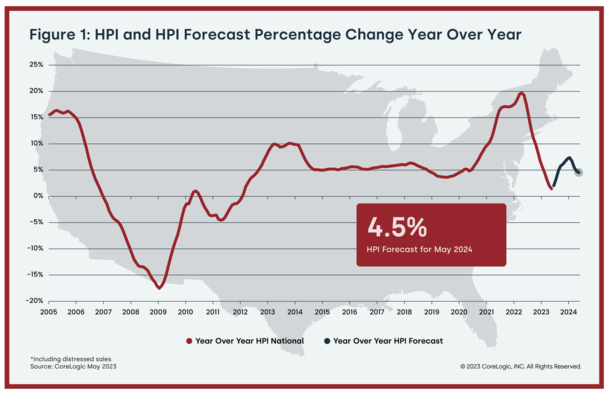

And why many forecasts now have home prices gaining steam, with CoreLogic predicting an increase of 4.5% by May 2024.

In other words, don’t expect home prices to fall anytime soon because of high mortgage rates. Instead, watch inventory.

If inventory starts rising, you can begin to make the argument for falling home prices.

Read more: Will mortgage rates go down in 2023?

{kind=link}