Income tax notice under section 143(1) is a message sent after processing return. It Compares your filed return with department’s computations. If you have received the income notice under 143(1)(a) due to variance in income as a mismatch with 26AS and the details are correct then You have to agree to the notice and file a revised return.

Notice under section 143(1)

Notice under section 143(1) is simply an intimation in response to the tax return filed by you, which will do one of the following:

- The return filed by you matches the assessment of the AO and no further action is required

- You will be issued a refund, through the bank account stated in the return, as the amount of taxes paid is more.

- A demand notice, as you have paid less than the required amount of taxes and taxes are due by you, which will need to be paid within 30 days of receiving the demand.

You should open the document sent in the email with the notice. Scroll down to the bottom and see what is net tax payable as shown in

Notice under section 143(1A)

Notice u/s 143(1A) is sent If there are any mismatches, such as you have not included in your return all the income as reported in your 26AS, then these computer-assisted notices will be sent seeking necessary clarification. You will need to respond to this notice within 30 days by logging onto the income tax portal and uploading the proof needed to correct the mismatch. Notice Variance due to Income From Other sources

If you have received a communication of proposed adjustment u/s 143(1)(a) notice, please read the article here. This is different from a 143(1) notice.

Income tax notice under Section 143(1)

When is the Income tax notice under Section 143(1) – Letter of Intimation served?

Three types of notices can be sent under section 143 (1)

- Intimation where the notice is to be simply considered as final assessment of your returns since the CPC or assessing officer has found the return filed by you to be matching with his computation under section 143 (1).

- A refund notice ,where Income tax refunds you for extra tax paid, then you can look forward to the cheque.

- Demand Notice where the officer’s computation shows shortfall in your tax payment. The notice will ask you to pay up the tax due within 30 days.

What is the time limit of sending the intimation?

The intimation is sent before the expiry of one year from the end of the assessment year in which the income was assessable. In other words, before the expiry of one year from the end of the financial year in which the return was filed.

How is the intimation sent?

These intimations are sent through email to the Email address provided in filing income tax returns online. As e-return are processed by Central Processing Centre (CPC) sender is intimations@cpc.gov.in. For e-return hard copy will also be sent through post at the address associated with PAN number just like the non electronic filed ITRs. Our article Income Tax Notice :Sections,What to check,How to reply explains how to find address associated with PAN number.

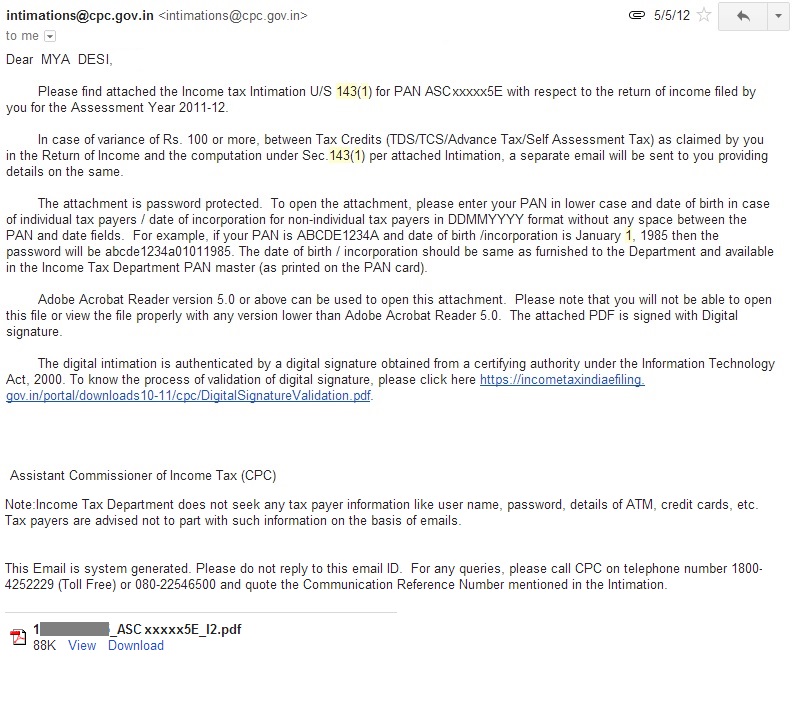

Sample e-Mail sent with an attachment is shown in image below.Attachment can be a pdf file or a zip file.

Email for 143(1) notification

As mentioned in email, attachment is password protect. Password is your PAN number in lower case, followed by your date of birth in DDMMYYYY format , for example for Mr Sharma with PAN number AJSPD8693E and date of birth as 20-Mar-1976 the password would be ajspd9693ed20031976

If it’s zip file extract the pdf and open the pdf.

The Document with Income Tax Notice 143(1)

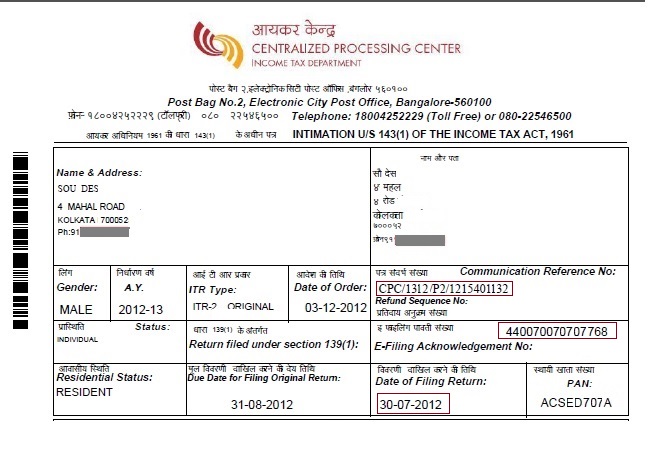

First part of the document has information on Name & Address, PAN number, ITR Type,A ssessment Year, E-Filing Acknowledgement Number ,C ommunication Reference Number, Date of Order as shown in the image below. Date of order is that Date on which order under section 143(1) was passed by the CPC Bengaluru . Please check that the intimation is for you only.

Introduction in 143(1) document

One can contact Income Tax Helpline/Toll Free Number of CPC Bangalore Income Tax Department (Bengaluru) at 1800 -425 2229 or 080-22546500 for Income tax queries. Before you contact you should have Communication Reference No (marked in image above) with you and remember your PAN card details like PAN Card number, Date of Birth

The second part of the document shows computation of income, with income reported under various categories, deductions claimed, taxable income, tax due, tax paid ex advance tax, self assessment tax, TDS, etc in two columns as shown in image below:

a) As provided by taxpayer in his Income tax return is from the ITR filed by the tax-payer.

b) As computed under section 143(1) are computations by CPC .

Part of document which shows Income type (Income from Salary, Income from House Property etc) is shown in image below. Note: The heads of income may be different depending on ITR filed by you. For example ITR1 will not have Income from Capital Gains. Please check that Income is considered properly under appropriate head. Income under one head of income is not considered as from another head or repeated under another head of income

")

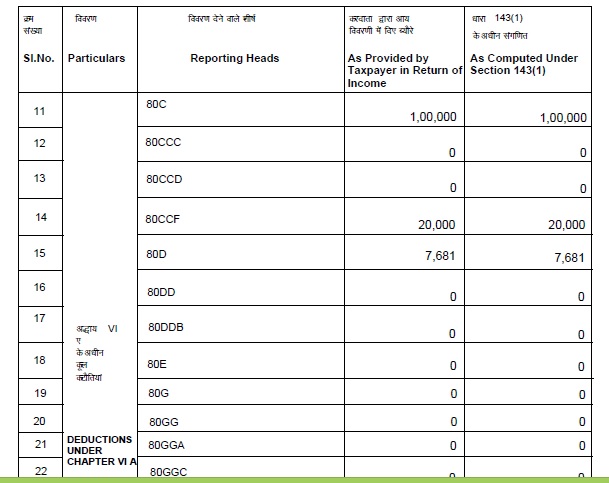

Computation in two columns in 143(1)Part of document which shows Deductions claimed under various heads such as 80C, 80D etc is shown below. Please check that deductions you have claimed under 80C and other sections of chapter VI are considered.

143(1) VIA deductions claimed

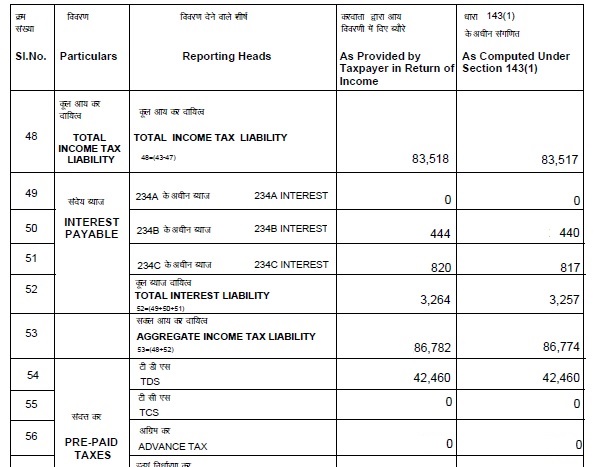

Part of document which shows the tax calculation is shown below.

143(1) tax calculation

Please check that TDS claimed, Advance Tax and Self Assessment Tax paid is reflected in the computation by CPC. CPC picks up the figures from your Form 26AS. Form 26AS is the tax department’s statement showing income tax deposited on your behalf and can viewed on TRACES website or through netbanking. One should verify Form 26AS before filing returns. If there are mismatches in Form 26AS with respect to Form 16/Form 16A then it has to be taken up with the accounts department of your company/bank and errors need to be rectified.

Small Difference in Calculations: You may see difference between the calculations in two columns for example total income after deductions As Computed Under Section 143(1) is 5 rupees more than the amount in Return of Income. This is due to Rounding of income and Income tax payable The income tax act suggests rounding off of income under Section 288A and the income tax payable Section 288B. This is discussed later in Rounding of Income and Tax

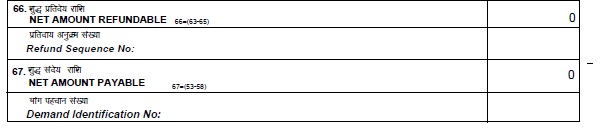

Scroll down and at the end of all calculations you would see two headings Net Amount Refundable and Net Amount Payable as shown in image below.(Row numbers may be different)

143(1) Net tax payable or refundable

If net amount refundable mentioned in Intimation under section 143(1) more than 100 rupees, it means that tax refund is due from income tax department to tax payer. Refunds amounts less than 100 rupees aren’t refunded. You can check refund status online. He will first receive this intimation on mail then a manual intimation along with the refund cheque will reach his address. On receiving the cheque, one can deposit the cheque .

If net amount demand mentioned in Intimation under section 143(1) is more than 100 rupees, then tax payer needs to pay tax . This will be treated as demand notice for the payment of income tax due. This Intimation letter encloses challan form to pay income tax if the due is more than Rs 100. In case of Demand, this intimation may be treated as Notice of demand u/s 156 of the Income Tax Act, 1961. Accordingly, you are requested to pay the entire Demand within 30 days of receipt of this intimation“. If tax payer thinks that

- Tax Demand is valid : he needs to pay the tax.

- Tax Demand is wrong : then he must prove his case following appropriate procedure. He may make an application for rectification under section 154. He may consult a qualified CA or good tax expert for further action. However,sometime return processing by CPC becomes difficult and the taxpayer may contact local income tax officer (ITO) and submit a written application for rectifying your assessment. Support it with his TDS statements, Form 26AS, intimation under section 143 (1) and notice of demand. In a plain paper he can also submit an application for Stay of Recovery. Proceedings for requesting them to hold further proceedings till rectification is made.

If net amount refundable/net amount demand is less than Rs 100 or no difference, you can treat Intimation under section 143(1) as completion of income tax returns assessment under Income Tax Act.

Rounding off Income and Tax

Section 288A : As per section 288A of the Income Tax Act, the total income computed as per various sections of this act, shall be rounded off to the nearest Rs 10. For the purpose of rounding off, firstly any part of rupee consisting of paisa should be ignored. Thereafter, if the last digit in the total figure is 5 or greater than 5, the total amount should be increased to the next higher amount which is a multiple of Rs. 10. If the last digit in the total figure is less than 5, the total amount should be reduced to the nearest lower amount which is a multiple of Rs 10. This rounding off of income should be done only to the total income and not at the time of computation of income under the various heads. Eg: If total income is Rs. 7,83,944.50 gets reduced to 7,83,940 while if income had been 7,83,945.50 it gets rounded off to 7,83,950.

Section 288B : Rounding off Income Tax As per Section 288B of the income tax act, the total tax computed shall be rounded off to the nearest Rs 10. The rounding off of tax would be done on the total tax payable or refundable and not to various different sub-heads of taxes like income tax, education cess, surcharge etc. Rounding off would be done in the same manner as above i.e.. firstly paisa would be ignored and thereafter if the last digit in the total figure is 5 or greater than 5, the total amount should be increased to the next higher amount which is a multiple of Rs 10. Eg: If the total tax payable of a taxpayer is Rs. 79,223.25 gets rounded to 79223 and then to 79,220, while Rs.79226.25, gets rounded off to Rs 79226 and then to Rs 79230

Related Articles :

{kind=link}