You may have heard the phrase mortgage rate lock-in effect lately.

As a quick refresher, it’s a homeowner’s unwillingness to give up an ultra-low mortgage rate for a much higher one.

Or simply the inability to give up their low rate, as qualifying for a home purchase at today’s much higher rates would be an impossibility.

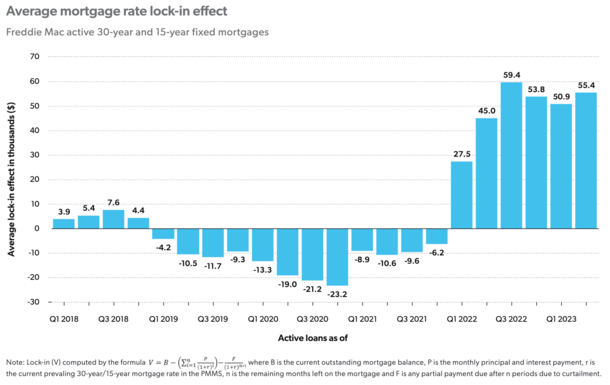

Regardless, there is now a value assigned to this so-called mortgage rate lock-in effect, with Freddie Mac putting the average at about $55,000.

This means an existing homeowner needs a big incentive to sell, unless they want to forgo that value.

How Valuable Is Your Low Mortgage Rate?

Freddie Mac reported that six out of 10 borrowers now have a mortgage rate at or below 4%.

And that the mortgage rate lock-in effect is a benefit to homeowners who hold fixed-rate mortgages.

Now everyone knows a low mortgage rate can save you money, thanks to a lower monthly payment.

But it also carries value, which can ebb and flow based on prevailing market rates. Never has this been truer than the last year and change.

Simply put, mortgage rates more than doubled from their record low levels in 2021.

As a result, those who locked in low rates around that time now hold something extremely valuable.

For perspective, the 30-year fixed hit its all-time low of 2.65% in early January 2021, per Freddie Mac.

Last week, it averaged a significantly higher 6.78%, which is a more than 150% increase.

Aside from creating a world of haves and have nots, it has made moving a lot more difficult for those who need a mortgage to buy a home.

Even if you can qualify at a much higher interest rate, do you want to give up your low rate?

It’s not as if home prices have come down, so you’re simply trading your old low fixed-rate mortgage for a new one that’s much more expensive.

But how much would you “lose” if you did? Well, now we might know.

Determining the Value of Mortgage Rate Lock-In

Thanks to some daunting math, this value has now been quantified by Freddie Mac economists.

They determine the value of mortgage rate lock-in by taking the difference between the outstanding balance of the mortgage and the present value of the mortgage at prevailing market interest rates.

In their example, a “lucky homeowner” gets the opportunity to refinance their mortgage at 2.65% in January 2021.

Their $250,000 loan amount would be whittled down to about $236,379 after 29 months, with a ridiculously low principal and interest payment of $1,007.

Now supposing they wanted to sell and move elsewhere today, they’d be looking at a comparable mortgage rate closer to 7%.

Assuming a similar loan amount, the monthly P&I would jump to more than $1,500 per month.

This hypothetical example puts the value of mortgage rate lock-in at a sizable $86,136.

Put another way, they’d need a near-$90,000 reason to move, whether it was for a much better job, way of life, etc.

Otherwise, they’d need to stay put, which appears to be the most common outcome at the moment given the dearth of existing housing inventory.

Your Mortgage Rate Lock-In Value May Vary

The Freddie Mac economists noted that the average value of mortgage rate lock-in “varies considerably” thanks to region and year of origination.

For example, it’s just $32,000 in West Virginia, but a whopping $91,000 in Hawaii.

And those who took out mortgages in 2020 and 2021 have an average mortgage rate lock-in value of $77,000 and $85,000, respectively.

What’s perhaps more surprising is even those who took out a home loan in 2023 have an average mortgage rate lock-in value of $10,000.

Overall, homeowners with fixed-rate mortgages financed by Freddie Mac (30-year and 15-year fixed loans) have locked in a collective $700 billion dollars in total value.

This total is equal to about 25% of Freddie Mac’s single-family mortgage portfolio’s unpaid principal balance.

It tells you why this phenomenon is so impactful, and why there is a major lack of available for-sale inventory at the moment.

While this will dampen home sales and mortgage originations, it should help prop up home prices at a time when affordability has rarely been worse.

Freddie Mac said its official corporate forecast for the next 12 months has home prices falling by 2.9%, followed by another 1.3% annual decline.

But given current market conditions (and an early read on their data), they expect an upward revision.

In short, they foresee continued tight inventory due in no small part to this lock-in effect, which should keep sales volume down but prices up.

Read more: Will mortgage rates go down for the rest of 2023?

{kind=link}