You finally went on that date. The conversation was fun and the eye contact was on point. But no call, no text—nada. Then you think back to when you both grabbed your credit cards to pay. You couldn’t help but notice their shiny Amex label—and the side-eye you got when you pulled out your credit-building card.

But surely that wasn’t a red flag?

You’d be surprised. A study found that 65% of millennials think having a good credit score is important in a life partner. And if your card says anything—it’s that you’re not doing great in that department.

So what exactly are people thinking when they see your credit card?

We’ve gone detective and scoured the online forums to give you the complete scoop—

Chase Sapphire Reserve: The Latte-Loving Millennial

You possess a thirst for travel, and you’ve been told you’ve got quite a refined palate. Your Starbucks addiction is legendary, but you’re not just about caffeine buzzes—you’re all about exploring new horizons.

Your career in tech or finance fuels your jet-setting lifestyle, allowing you to enjoy all the dining and travel perks. You’ve mastered the art of living your best life (with Instagram posts to prove it).

When you’re not snapping pictures of your food, you’re often found in the VIP lounge, sipping on a glass of wine while working to pay those bills.

Amex Gold: The Foodie Financier

You’re a high-earning, high-spending individual who navigates weekly food shopping like a pro. Your grocery bills may be steep, but you refuse to compromise on quality.

Grubhub is your saving grace on busy nights—and dining out is your guilty pleasure. You take Ubers to all the restaurants, indulging in top-notch meals without worrying about the not-so-dreaded bill.

And if you’ve got the Amex Rose Gold Card, you certainly won’t shy away from showing it off. Flaunting that shiny card is almost as satisfying as the weight of the chunky metal in your wallet.

And here’s an interesting tidbit: One in five Americans say points are the best benefit of credit cards—yet 52% don’t track them Are you one of them?

Discover It: The Carefree Cardholder

As a college student, this starter card is your first taste of financial independence—and you’re embracing it with wide-eyed enthusiasm.

The allure of cashback rewards has you bubbling with excitement. Every dollar earned feels like a small triumph—and you can’t help but sing the card’s praises to anyone who’ll listen.

You’re a free spirit, breezing through without reading the fine print. If you paid attention, you’d see that the rewards system is more complex than juggling your partying with studying.

But why let the details dampen your optimism? As time passes, you’ll stash the card away in a dusty drawer—a memento of your college days.

Amex Centurion Black Card: The Elite Tycoon

The Centurion card is the ultimate status symbol, giving you access to a world of luxury and privilege.

So, don’t lie—we know you live for skipping lines and strolling into reserved areas with that air of superiority.

But it’s not just about the perks. It’s the ability to impress us normal folks who can’t touch this coveted card. It’s the ultimate flex, a statement that you’ve arrived and conquered.

You understand that the $10,000 initiation fee is a small price to pay for the status and exclusivity that comes with the card.

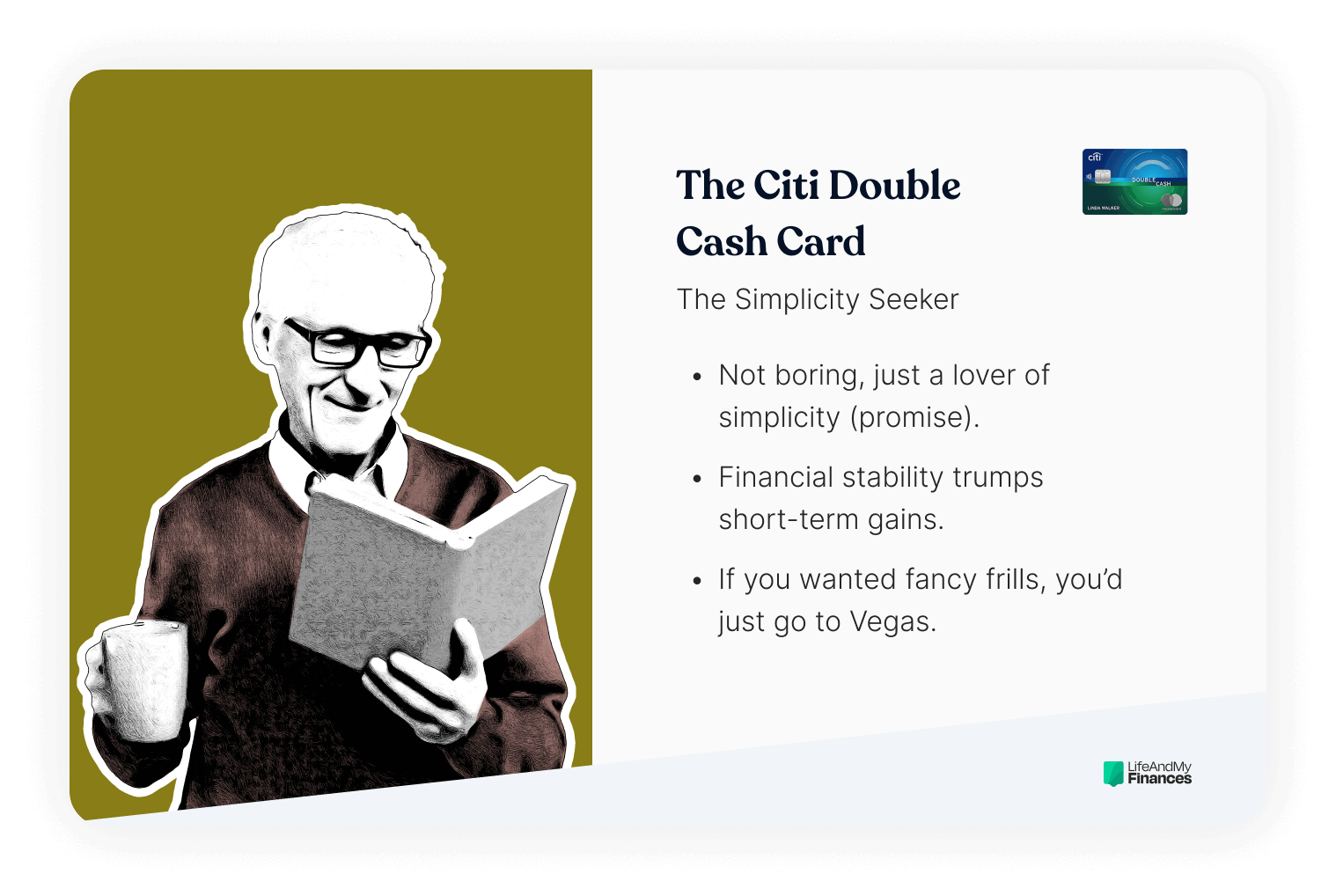

Citi Double Cash Card: The Simplicity Seeker

The Citi Double Cash Card may not be flashy or extravagant, but that’s what draws you in. Some might say boring—but you enjoy the simple things in life.

You couldn’t care less about sparkly sign-up bonuses or rich rewards. And while the tempting cashback rewards don’t excite you, financial stability over short-term gains certainly does.

You’re a classic minimalist, choosing substance over style and finding beauty in the understated. Your card is a true reflection of your practical mindset and grounded nature.

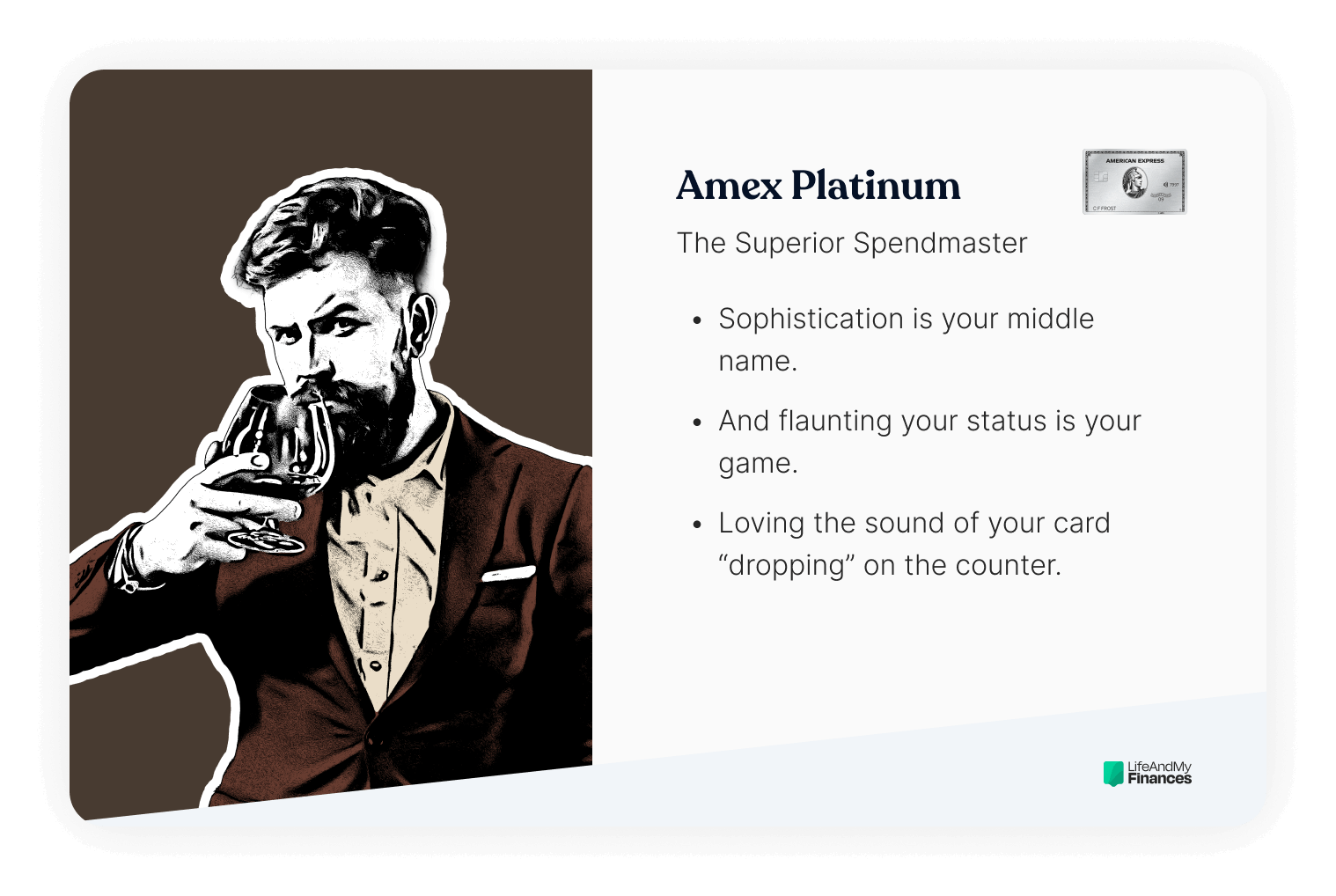

Amex Platinum: The Superior Spendmaster

With your sleek Amex Platinum card, you’re no stranger to sophistication. You’re the epitome of the upper-middle-class, who likes to see themselves more as strictly upper-class.

Studies have shown that demand for a platinum card is much higher than the demand for the benefits it comes with So no wonder you’re a confident cardholder. (It helps that your bank can handle the $695 annual fee without a second thought.)

Splurging comes naturally, and shopping at Saks is your favorite pastime. The sound of your prestigious metal card hitting the counter is music to your ears.

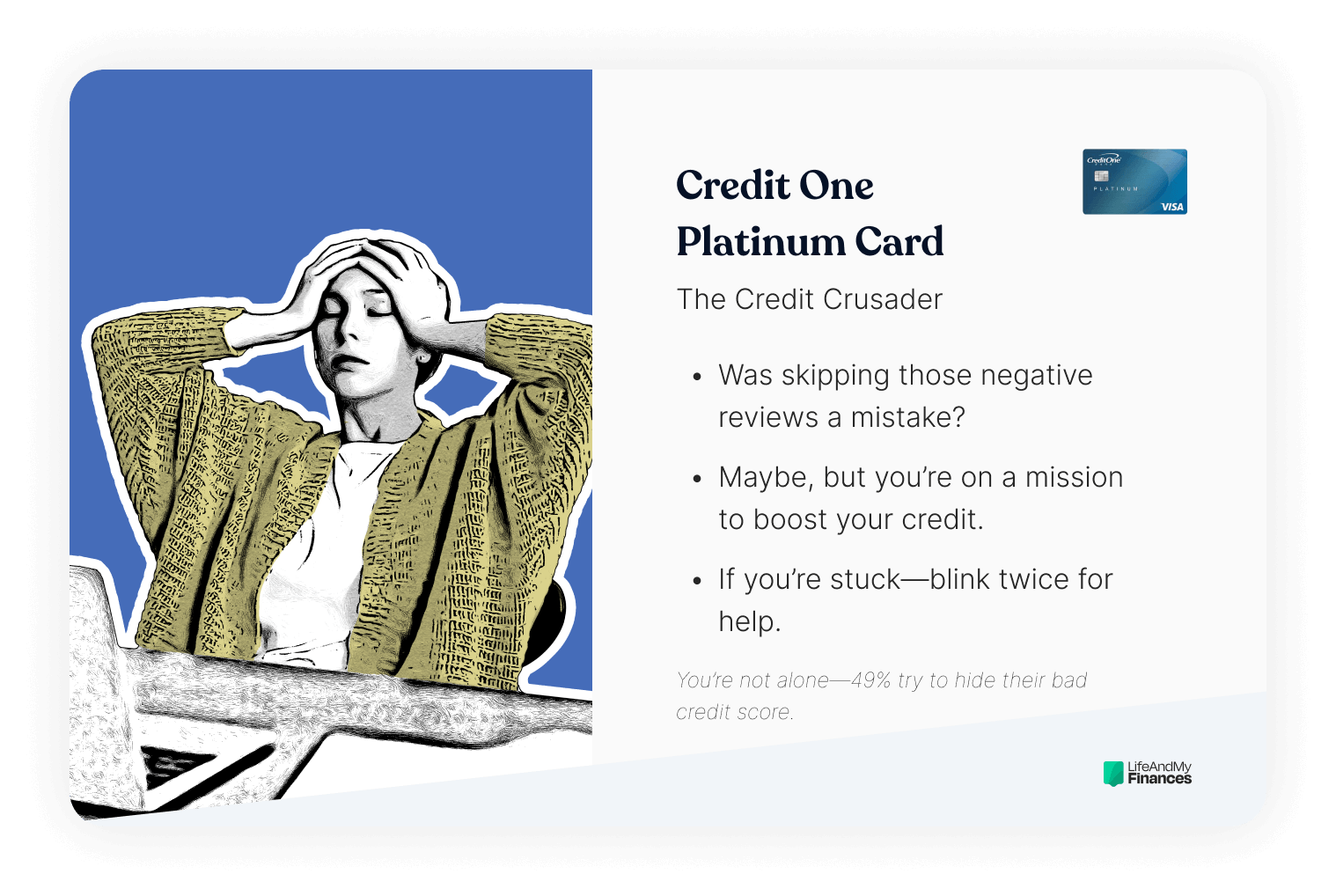

Credit One Platinum Card: The Credit Crusader

You’ve stumbled on some tough financial times, but that hasn’t stopped you from trying to build a better credit future.

In the rush to boost your score, you may have skipped the research phase, ignoring negative reviews and diving headfirst into any offer thrown your way. Or maybe you were just out of options.

It probably won’t surprise you that 49% try to hide their bad credit score from others Though it’s honestly hard to hide if you’re carrying this credit card around.

And yet you bravely stick with this less-than-ideal card, fearing the credit score abyss if you sever ties. But don’t let these setbacks bring you down. Keep riding that coaster of credit building, and you’ll get off—eventually.

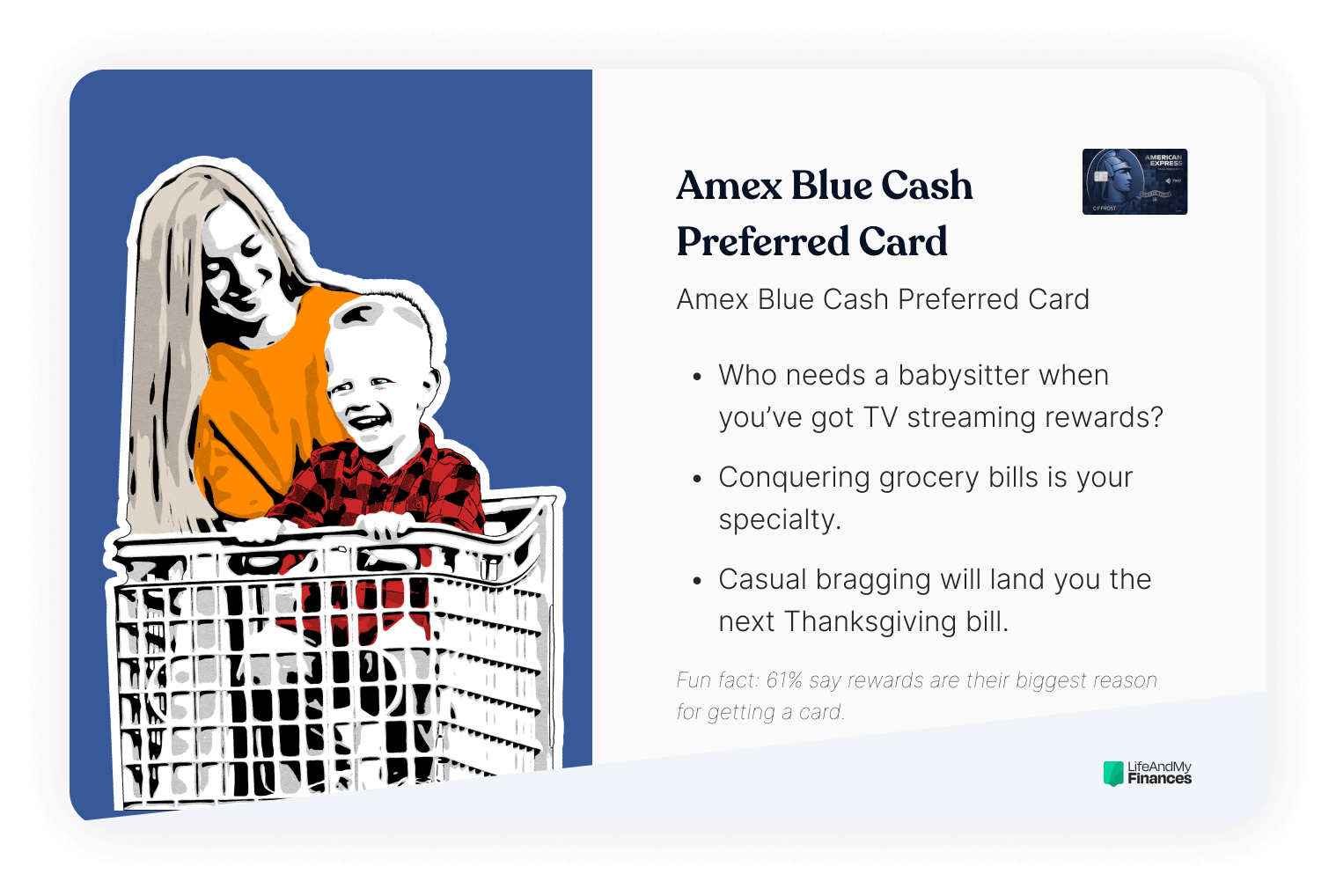

Amex Blue Cash Preferred Card: The Family Fuel Provider

Your grocery bills may be hefty, but you tackle them with gusto. With your Amex Blue Cash Preferred Card, you supercharge your savings and earn generous rewards on all those trips to the store.

And you’re not the only sucker for perks: 61% say rewards are their biggest motivator to getting a credit card We’re guessing that’s what drew you into this one.

Streaming rewards are your secret weapon to keeping your kids entertained. Name any streaming service—you’re probably subscribed to it. (Though with all those after-school clubs, you’re questioning if it’s really worth it.)

Apple Card: The Apple Enthusiast

With the Apple Card, you’re not just a fan of the brand—you’re a die-hard member of the tribe. And the aesthetics aren’t bad, either. Made from titanium, the card is as sharp as your tech-savvy wit.

As an Apple enthusiast, you’re deeply rooted in the Apple ecosystem—and you’re totally fine with that. Nobody would bat an eye if you got a nerdy tattoo that proudly displays your passion for all things tech.

You’re at the forefront of innovation, marching to the beat of your own nerdy drum. Stay stylish, stay secure, and stay Apple (you have no choice).

Bank of America Visa Debit Card: The Debt-Free Dave

You’re a true warrior against the clutches of credit cards and a dedicated fan of financial guru Dave Ramsey.

For you, debit rules the roost. You firmly believe your money should be yours, not the “bank’s money” tied to credit.

Living free from debt and loans is your ultimate goal—and you’re determined to achieve it. After all, 82% of Americans are worrying about the credit debt piling up

Credit cards? They’re just evil masterminds of a credit conspiracy. You refuse to succumb to their web of tempting rewards and hidden fees while waving your defiant flag with pride.

Key Takeaways

- If you strongly disagree with any of our light-hearted, not-to-be-taken-seriously statements, we apologize.

- These views are largely based on those who like a good old rant on the internet and are not scientifically backed up. (Though that Amex Centurion Card is still a serious flex.)

- But there’s no harm in taking a sneaky peak next time your date pulls out their credit card.

Any of these credit cards catch your eye? Here are some similar options to explore:

FAQ

What does a credit card symbolize?

A credit card can symbolize financial flexibility and convenience. It lets you make purchases without carrying cash and offers a line of credit for emergencies or larger expenses.

Credit cards also offer extra perks, like reward programs, fraud protection, and the ability to build credit history. But it’s crucial to use credit responsibly, avoiding debt and making timely payments to maintain a positive credit score.

What are five things credit card companies don’t want you to know?

Here are five things credit card companies may not share or emphasize:

- High interest rates: They often highlight rewards but downplay the hefty interest rates that kick in if you carry a balance. This could potentially lead to long-term credit card debt.

- Hidden fees: Some companies have fees like annual charges, balance transfer, or foreign transaction fees. Being aware of these can help you cut down on extra costs.

- Credit score impact: Maxing out your credit card or missing payments can harm your credit score. Maintaining a low credit utilization ratio and making timely payments is essential.

- Marketing tactics: They can use persuasive techniques to tempt you into spending more. Understanding their tactics helps you make better decisions and avoid impulsive purchases.

- Negotiation power: You can negotiate better terms, such as lower interest rates or waived fees, if you have good credit. Being proactive and advocating for yourself can save you money.

Is a credit card a status symbol?

Many see certain credit cards as status symbols due to the benefits they offer. They offer a convenient and flexible way to make purchases, access credit, and earn rewards.

For example, premium credit cards often come with exclusive perks, like airport lounge access, concierge services, and travel insurance.

But the status associated with a credit card depends on factors such as brand, credit limit, and usage patterns. Prioritizing responsible financial habits and personal needs is more important than using a credit card just for status.

What does your credit card statement tell you?

Your credit card statement provides valuable insights into your financial activity:

- Transaction details: The statement shows your purchases, indicating where and when you spent money. This helps you track your expenses and identify any unauthorized charges.

- Payment due date: It specifies the deadline for making your minimum payment or paying the full balance. Timely payments avoid late fees and negative impact on your credit score.

- Interest charges: If you carry a balance, the statement reveals the amount of interest incurred. Understanding these charges encourages responsible credit card usage.

- Rewards summary: If you have a rewards program, the statement summarizes your earned points or cashback. This allows you to take advantage of the benefits available to you.

- Credit limit and available credit: It shows your credit limit and the remaining available credit. Staying within your credit limit is vital for maintaining a healthy credit utilization ratio.

Why are credit cards so powerful?

With credit cards, you can spend without needing physical cash. They also offer financial flexibility by providing access to a credit line. So you can make purchases even when you don’t have immediate funds available.

Credit cards often come with rewards and perks that boost their power. Cashback, travel points, or other reward programs can add value for cardholders, leading to savings or exclusive benefits.

Responsible credit card usage can also contribute to building a positive credit history, which is handy for obtaining loans or mortgages in the future.

Lastly, credit cards offer consumer protections that provide peace of mind. Fraud protection and dispute resolutions safeguard against unauthorized transactions.

What is a red flag on a credit card?

Unauthorized charges are a major red flag. If you notice transactions on your credit card statement that you didn’t make or recognize, it could indicate fraud or identity theft.

Excessive credit utilization is another red flag. When you consistently use a significant amount of your available credit, it can negatively impact your credit score and suggest financial instability.

Late payments are a common red flag that can have a bunch of negative consequences. Missing payment due dates can lead to late fees, increased interest rates, and even a negative impact on your credit score.

If you see a sudden credit limit decrease, it’s also a red flag worth investigating. A big reduction in your credit limit can affect your credit utilization ratio, limit your spending, and show concerns about your creditworthiness.

What is black card status?

Black card status refers to an elite level of credit card membership offered by certain financial institutions.

These cards are typically invitation-only and cater to high net worth individuals. For example, the American Express Centurion Card offers personalized concierge services, luxury travel perks, and exclusive membership rewards.

Black card status symbolizes a level of wealth and provides access to perks and services tailored to the needs of high-end clientele.

Sources

See all

Take a Look: Millennial and Gen Z Personal Finance Trends—Experian Global News Blog. (n.d.). Retrieved July 21, 2023, fromhttps://www.experian.com/blogs/news/2023/05/23/millennial-gen-z-personal-finance-trends/

Over Half of Americans Don’t Keep Track of Credit Card Points—Coupon Chief. (n.d.). Retrieved July 21, 2023, fromhttps://www.couponchief.com/blog/credit-card-rewards-survey/

Bursztyn, L., Ferman, B., Fiorin, S., Kanz, M., & Rao, G. (2017). Status Goods: Experimental Evidence from Platinum Credit Cards (Working Paper No. 23414). National Bureau of Economic Research.https://doi.org/10.3386/w23414

Credit Sesame Survey: The cost of poor credit is more than just financial—Credit Sesame. (n.d.). Retrieved July 21, 2023, fromhttps://www.creditsesame.com/blog/credit-score/credit-sesame-survey-poor-credit/

Americans Save An Average $757 Per Year By Using Credit Card Rewards, According to a Survey Commissioned by Slickdeals. (n.d.). Retrieved July 21, 2023, fromhttps://www.prnewswire.com/news-releases/americans-save-an-average-757-per-year-by-using-credit-card-rewards-according-to-a-survey-commissioned-by-slickdeals-301383301.html

Survey: Nearly 82% Worry About Their Credit Card Debt | Credit Cards | U.S. News. (n.d.). Retrieved July 21, 2023, fromhttps://money.usnews.com/credit-cards/articles/survey-nearly-82-worry-about-their-credit-card-debt

{kind=link}