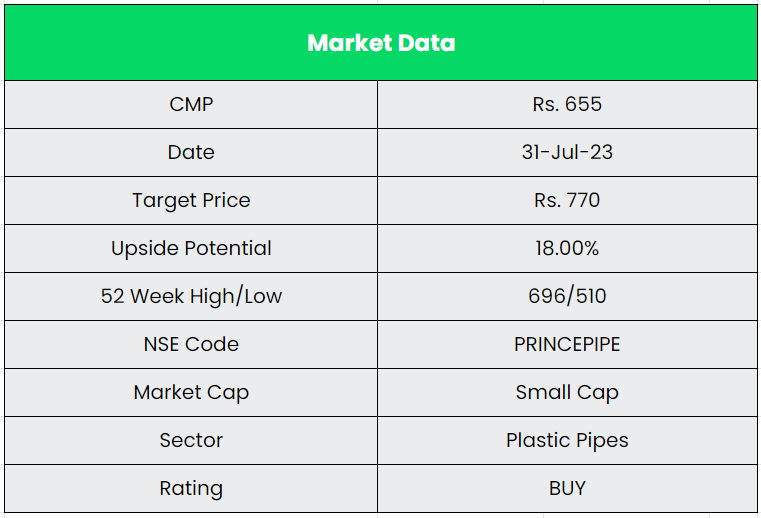

Prince Pipes & Fittings Ltd. – Pure Play Plastic Pipe Company

Prince Pipes and Fittings Limited (PPFL) is one of India’s largest manufacturers of integrated piping solutions & multi polymers, based in Mumbai, Maharashtra. Incorporated in 1987, Prince is one of the fastest growing companies in the Indian pipes and fittings industry. For over 3 decades, the company has been engaged in the manufacturing of polymer piping solutions in four types of polymers – CPVC, UPVC, HDPE, PPR. With a network of more than 1,500 distributors, PPFL is steadily increasing its pan-India distributor base to ensure stronger customer proximity and respond faster to their needs. Prince Pipes and Fittings Limited has 7 state-of-the–art manufacturing units located across the country at Haridwar (Uttarakhand), Athal & Dadra (Dadra and Nagar Haveli), Kolhapur (Maharashtra), Chennai (Tamil Nadu), Jaipur (Rajasthan) and Sangareddy (Telangana).

Products & Services:

It has several products spread across several segments.

- Plumbing – FLOWGUARD PLUS, EASYFIT AND EASYFIT RE.

- Industrial – GREENFIT, GREENFIT BLUE, Etc.

- Sewage – SILENTFIT, ULTRAFIT and RAINFIT

- Underground – FOAMFIT, DRAINFIT, CORFIT and DURAFIT.

- Agri – AQUAFIT, SAFEFIT and PEFit Aqua

- Others – STOREFIT in Water storage segment and CABLEFIT in Cable ducting segment.

Subsidiaries: As on FY23, the company doesn’t have any subsidiaries.

Key Rationale:

- Leadership Position – PPFL is one of the top six players in the pipes & fittings market in India. The growing market position is supported by well-known brands ‘Prince’ and ‘Trubore’ and the diverse product offerings with presence in un-plasticized polyvinyl chloride (UPVC), Chlorinated polyvinyl chloride (CPVC), Polypropylene random (PPR) and High-density polyethylene (HDPE) segments. Prince has ~10% market share in overall CPVC market and CPVC contributes ~20-25% in Prince’s overall portfolio (volume and value). In the overall piping industry, Prince currently has 6.5-7.5% market share. Over the past five years, PPFL has made strategic moves to bolster its capacity for higher margin products, showcasing its commitment to growth and profitability. Notably, the company’s tie-up with Lubrizol has further enhanced its CPVC pipe portfolio, signifying a focus on product innovation and quality. The company is also introducing value added products to ensure cost efficiency and enhance market share.

- New Launches – In Q1FY24, the company launched and unveiled its new collection of luxury faucets and sanitaryware. Inspired by European bathware trends, the new range entails a complete portfolio of world class faucets. The range goes by the names Aurum, Titanio, Platina, Tiara, Marquise. Matchless in style and design they have been carefully curated following exhaustive industry research. Argento, Meta, Kristal and Palladium complete the Prince Bathware line. During Q4FY23, the company launched 2-new products such as WireFIT & OneFit (with Lubrizol).

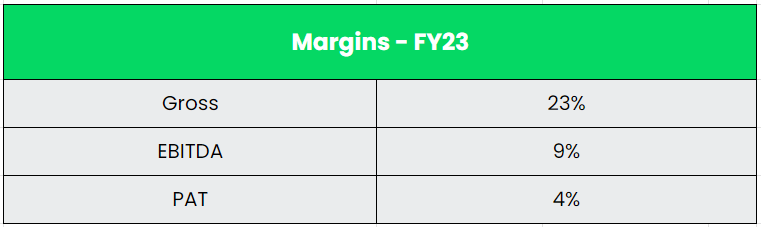

- Q4FY23 – The company’s revenue declined by 15.2% YoY to Rs.764 crore, impacted by 2.1% volume decline (due to higher base of Q4FY22) and 13.3% fall in realizations (due to lower PVC prices). However, QoQ growth was healthy at 8.3% (volume growth of 1.4%) on account of improved demand across Agri and Plumbing /SWR (Soil, Waste and Rainwater) pipes portfolio. EBITDA rose 5.6% YoY and 113.5% QoQ, while EBITDA margins improved by 381bps YoY and 956bps QoQ to 19.4%, driven by better product mix (higher share from fittings). PAT increased by 6.7% YoY and 165.9% QoQ to Rs.94 crore.

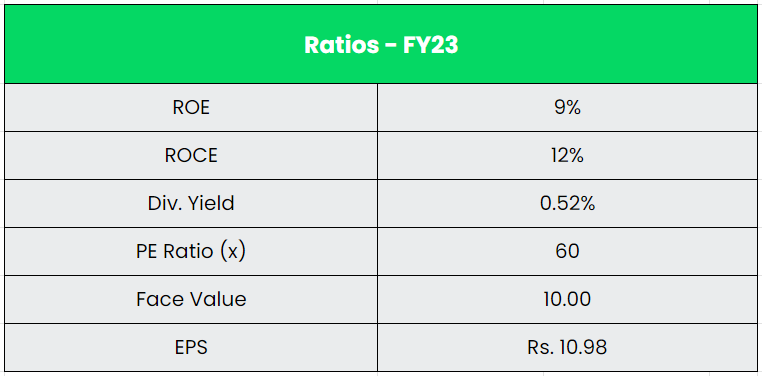

- Financial Performance – The revenue and PAT CAGR have grown at 16% and 11% between FY18-23. Also, the company maintained an average ROCE of ~22% and an average ROE of ~18% for the past 5 years. The Piping Volumes of the company have grown at a CAGR of 6% between FY20-23. The company remains long term debt free, while short term debt reduced from Rs.150 crore in FY22 to Rs.58 crore in FY23. Working capital days also fell from 68 in Mar’22 to 57 in Mar’23 as both debtor and inventory days improved.

Industry:

India’s high growth imperative in 2023 and beyond will significantly be driven by major strides in key sectors with infrastructure development being a critical force aiding the progress. Infrastructure is a key enabler in helping India become a US$ 26 trillion economy. Infrastructure development is always the key growth driver for Piping Industry. Indian plastic pipes industry has historically grown faster than the GDP led by multiple factors like real estate, irrigation, urban infrastructure and sanitation projects. Currently, plastic pipes market is valued at ~Rs.400 bn with organized players accounting for ~67% of the market. By end use, 50-55% of the industry’s demand is accounted by plumbing pipes used in residential & commercial real estate, 35% by agriculture and 5-10% by infrastructure and industrial projects. Between FY09-21 industry grew at 10%-12% CAGR, while demand is anticipated to expand at 12%-14% CAGR between FY21-25 and more than Rs 600bn by FY25E led by a sharp increase in government spending on irrigation, WSS projects (water supply and sanitation), urban infrastructure and replacement demand.

Growth Drivers:

- Under Budget 2023-24, capital investment outlay for infrastructure is being increased by 33% to Rs.10 lakh crore (US$ 122 billion), which would be 3.3% of GDP and almost three times the outlay in 2019-20.

- Under the National Infrastructure Pipeline (NIP), projects worth Rs.108 trillion (US$ 1.3 trillion) are currently at different stages of implementation.

- Under Budget 2023-24, the Government has allocated a massive Rs.70,000 Crore for the implementation of the Jal Jeevan Mission. It is almost 12x increase in outlay since 2018-19.

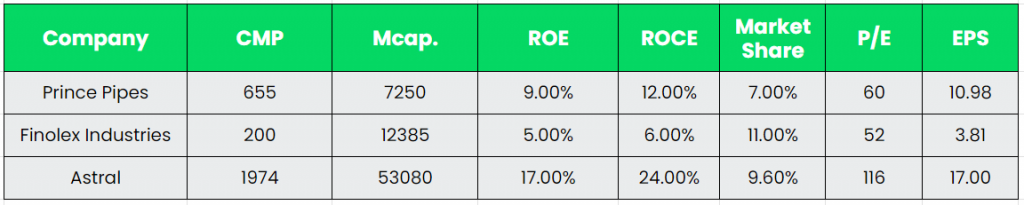

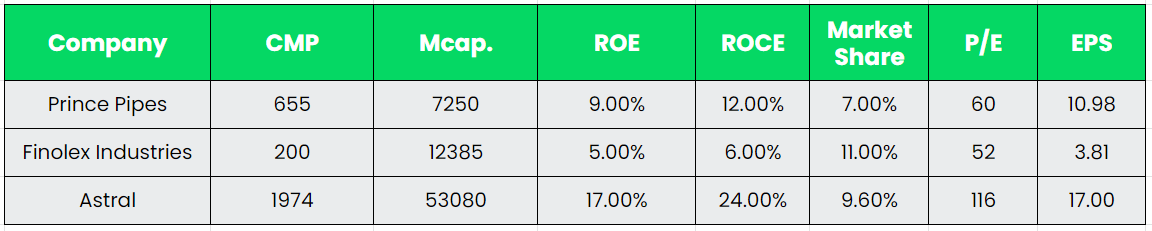

Competitors: Finolex Industries, Astral, etc.

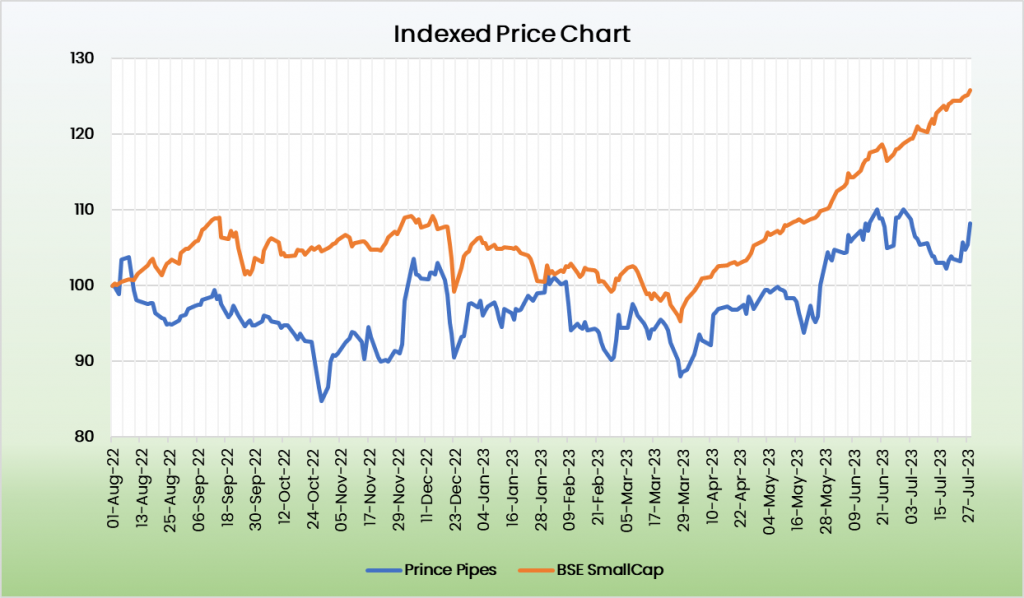

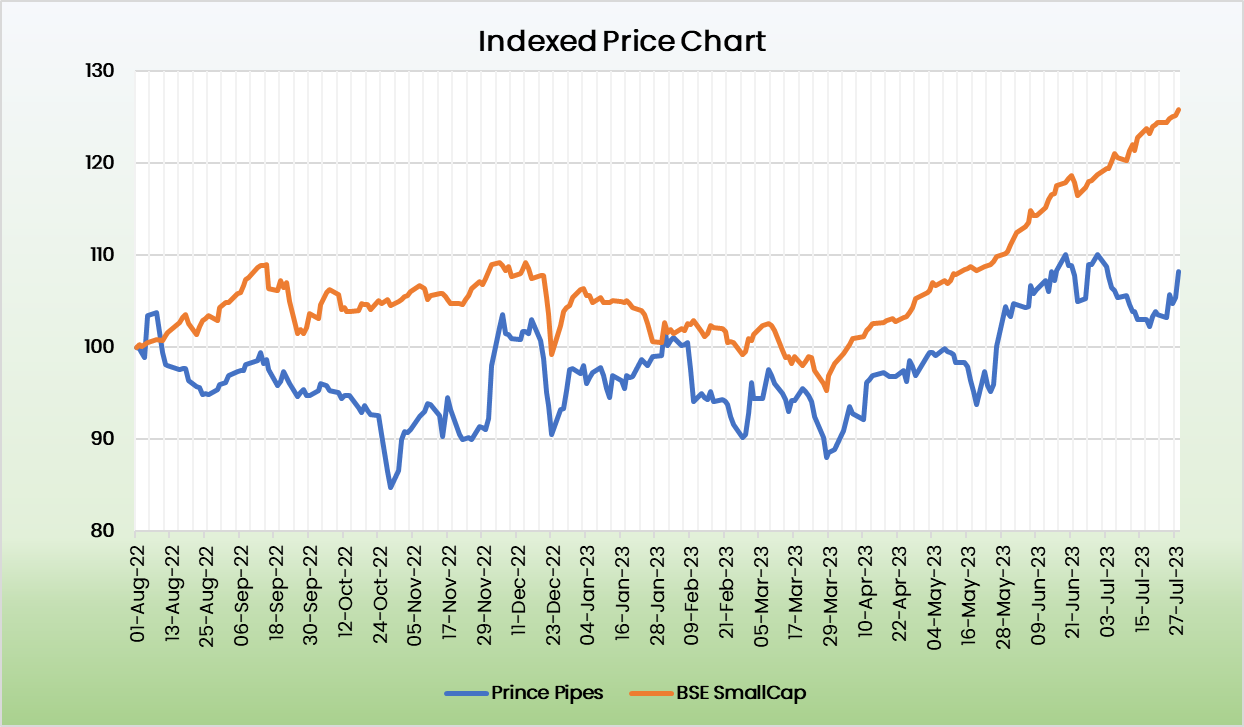

Peer Analysis:

From the below comparison, it is evident that Prince Pipes has less penetrated and has a huge market share gap to capture. In terms of Fundamentals, Astral Pipes remains strongest as it has a diversified business other than Piping. So, Prince with its complete focus on Piping & Fitting segment will pave way for a strong growth.

Outlook:

The company has guided for a 12-14% volume growth in FY24 (excluding Q1FY24 impact). On EBITDA margins, company reiterated their guidance of 13-15%. On-going Agri demand is robust due to better affordability & past-2/3 seasons have been muted. Management stated that demand from Jal Jeevan Mission is also very healthy, however company does not deal directly. The company has announced greenfield expansion in Bihar to cater the demand in East. Overall Capex in FY24 will incur a cost of Rs.150 crore (including land, plant and equipment costs) & the Bihar Plant will be operational from Q4FY25. The breakup will be Rs.75-80 crore for land and building for Bihar plant & Rs.80-85 crore for regular capex. By FY25 end, company will have 315k MTPA existing capacity, 35k MTPA coming in East + brownfield addition in planning stages. Besides, the company plans to continue adding value-added products to its portfolio – such as: surface drainage system and silent drainage system – which were introduced in Q3FY23.

Valuation:

We remain optimistic on the company’s long term growth prospects, given its constant portfolio enhancement and brand building, widening reach and healthy industry outlook. We recommend a BUY rating in the stock with the target price (TP) of Rs.770, 30x FY25E EPS.

Risks:

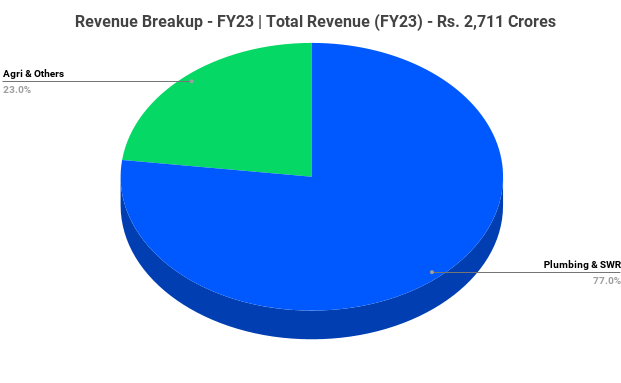

- Economical Risk – Any slowdown in real estate and infrastructure will directly impact the demand for plumbing and sewerage infrastructure piping system which contributes ~77% of Company’s revenue.

- Raw Material Risk – Any fluctuations in raw material prices like PVC or CPVC resins or forex will negatively impact profitability of the company.

- Competitive Risk – The pipes and fittings industry are highly competitive, especially in the commoditized products segment, which has low differentiation, thus resulting in the brand facing competition from both organized and un-organized segments. Any increase in competitive intensity may negatively impact business and financials.

Other articles you may like

{kind=link}

{kind=link}

{kind=link}