The mortgage cliff is here, with millions of homeowners rolling off record low fixed interest rates into repayments that have jumped by thousands of dollars per month.

This has caused the property market to teeter on the “edge of a financial nightmare that promises to devastate borrowers who are likely to buckle under the pressure as they scale this insurmountable cliff” – at least that’s how it’s being presented through public discourse.

But amid the waves of mortgage cliff panic sweeping the nation, a closer examination reveals that the fear may be more exaggerated than justified, according to Todd Sarris (pictured above), managing partner at mortgage advisory firm Spartan Partners.

“I appreciate that people have different interpretations of the ‘fixed rate cliff’ or ‘mortgage rate cliff’,” Sarris said. “To me, it suggests that when consumers’ fixed rates are adjusted to higher variable rates, they might struggle with repayments.”

“Where my heart breaks is that it will be true for a small minority of customers, however everything that I read and follow suggests that it is thankfully not true for the vast majority of consumers.

“Hence my agitation when finfluencers fearmonger the ‘mortgage cliff’ without ever providing proper context.”

The context: RBA data

The first place to look for context, according to Sarris, is the Reserve Bank of Australia, which forged the so-called mortgage cliff after raising the official cash rate by 400 basis points in 14 months.

For example, the RBA’s six-month Financial Stability Review released in April 2023 indicated that the household sector balance sheet in Australia remained strong at the end of December 2022.

Although the value of household assets fell by 2% in 2022, it was still 25% higher than at the end of 2019, and households had a large stock of liquid assets equal to their liabilities.

The report also showed that household finances were supported by a “strong labour market”, and most borrowers had built savings buffers to handle rising interest rates.

“Broader measures of liquid savings, beyond funds held in redraw and offset accounts, indicate an even larger degree of resilience to rising interest rates and higher costs of living,” the RBA report stated.

At this point, the RBA had increased interest rates by 3.50% so the impact was being felt.

Other RBA releases, such as a bulletin and speech both published in March, reached a similar conclusion.

Even the newly appointed RBA governor Michele Bullock had expressed this sentiment in July last year stating that that households were in a “fairly good position”.

“All-in-all, the conclusion off the back of data and analysis is that Australian households have strong cash balances, were many months ahead of repayments, and could accommodate a reasonable degree of interest rate increase,” Sarris said.

The context: Arrears data

While it may be coming from the RBA, the sentiment above could be just drowned out by more commentary. However, Sarris said that the data painted a similar picture.

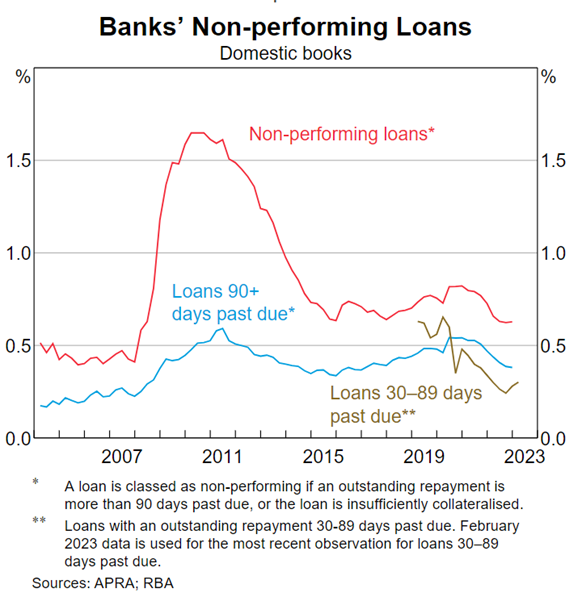

The graph below by APRA and the RBA illustrated that major banks in Australia have reported below long-run averages in terms of 30- and 90-day arrears. Foreclosure data has also tracked below long run averages.

This data suggested that an explosion in arrears because of expired fixed rates has not occurred. Instead, it showed that these measures were trending lower, and Sarris said this was likely due to the strength in the labour market and the economy.

“Having said that, I personally do expect 30- and 90-day arrears and foreclosures to increase through this year, but it won’t get to levels seen during the global financial crisis,” Sarris said.

“Banks will do anything and everything to keep their names out of newspapers following the Royal Commission. They will remain incredibly accommodative, which will be to the benefit of borrowers.”

The context: Tight lending policies

With interest rates dropping to below 2% at the start of the pandemic, it would be fair to suggest that there would be some easy money floating around.

However, Sarris said that the beginnings of the mortgage cliff coincided with a period where bank credit underwriting policy was at its “absolute tightest”.

“As such, the actual servicing position for borrowers was actually much better in reality,” Sarris said.

For instance, Sarris said rental income was heavily scrutinised, with some banks considering only 50% of the actual rental income when assessing borrowers’ capacity to service loans.

Moreover, Sarris said banks showed hesitancy in lending to JobKeeper recipients.

“As brokers, we had to populate exceptions documents if lending was proposed to a JobKeeper recipient where we needed to cover off on the client’s diversified income and asset position,” Sarris said.

Additionally, bonus, overtime, and commission income were subjected to heavy scrutiny. Sarris said some banks chose to exclude these types of income from loan assessments entirely.

For self-employed borrowers, the impact was even more pronounced.

Some banks assessed loans based on the worst financial year, often influenced by the adverse effects of the pandemic. As a result, borrowing capacity was reduced, and Sarris said it was “near impossible” to obtain exceptions to this rule.

The “most crucial point”

Another crucial factor was the serviceability buffer, a rate regulated by APRA that lenders use to protect borrowers against future rate rises.

Sarris said banks did not assess fixed rates at the APRA-imposed 3% buffer and instead opted for assessment rates that were “considerably higher”, usually around 5% to 6%.

But the most important point, according to Sarris, was that these buffers were not the “actual normalised assessment rates”.

“When you factored in the highly sensitised income treatments, the normalised assessment rates were probably between 6% to 7%. Everyone misses this critical point. So, this normalised assessment rate is, in most cases, higher than current discounted home loan and investment loan interest rates,” Sarris said.

“However, in the time since the fixed rates were first taken out, self-employed income has likely dramatically increased off the back of open domestic and international borders and removal of all pandemic-induced restrictions. For PAYG customers, they have experienced increased income albeit inflation is high.”

Cushioning the impact of the mortgage cliff

There’s no question that the mortgage cliff exists for a portion of borrowers. But Sarris said that there were also many support programs available and it was up to industry to help educate and make them aware of what was available when facing financial hardship.

“Banks have established dedicated Financial Hardship Teams to understand consumers’ circumstances and offer potential loan restructuring options, such as longer loan terms, interest-only periods, or temporary repayment suspensions,” Sarris said.

“Some banks also provide automatic variable rate discounts when fixed rates expire, and fast-tracked refinance processes are available for consumers seeking to refinance to higher-tier banks, subject to loan conduct and income confirmation.”

Nonetheless, Sarris said brokers were “exceptionally well placed” to support consumers that could experience financial hardship.

“Supporting valued clients in times of need is what we live for. It’s our passion, it’s our purpose,” Sarris said.

What do you think about the mortgage cliff? Comment below.

{kind=link}