While homeowners have certainly felt the impact of 12 cash rate increases in 13 months, new data has revealed that banks have been comparatively restrained, not passing on all of the Reserve Bank’s official cash rate increases over the past year.

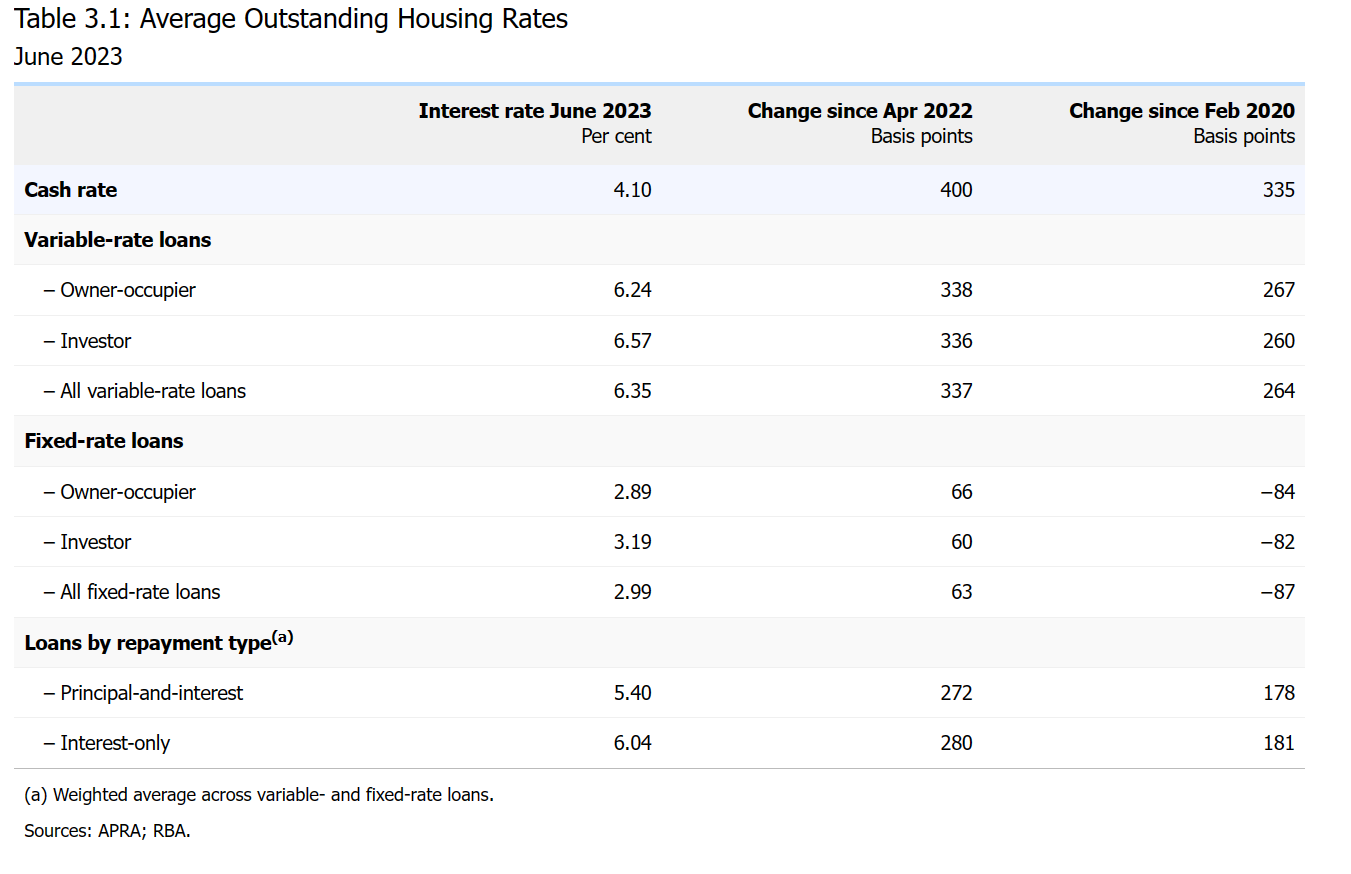

The RBA increased the cash rate by 400 basis points between April 2022 and June 2023, from 0.10% to 4.10%. However, lenders only increased their variable rates by an average of only 337 basis points.

This means that homeowners could be facing rates that are nearly 16% higher across the board if the banks had strictly followed the OCR.

So why is this? Well, the Reserve Bank puts it down to “strong competition in the mortgage market.”

Benjamin Cooper (pictured above), a mortgage broker from Sydney’s Shore Financial, said mortgage brokers played a central role in fostering this competition, by helping consumers compare loans from many different lenders.

“As a mortgage broker, you have relationships with the BDMs of the banks which allows for small, and crucial reductions on rates for the clients,” Cooper said. “We also have technology allowing us to see the best rates and products available for the clients, which in turn puts pressure on the banks and BDMs to have the lowest rates.”

A new rate cycle

The split between the OCR and the rate at which lenders raised rates was even more stark over a longer period.

Since February 2020, when the OCR was at the then-record low of 0.75%, the official cash rate has risen 335 basis points to June whereas lenders only increased variable rate loans by 264 basis points, representing a 22.6% difference.

This was roughly consistent across both investor and owner-occupier variable rate loans.

However, in recent months, there are indications that competition in the housing loan market has become less intense.

Specifically, the average variable rate on new housing loans rose by 29 basis points in June, according to the RBA. This increase surpassed the rise in the cash rate, marking a noteworthy development during this period of tightening.

Also, lenders have reduced discounts on their advertised lending rates, and most have now withdrawn cashback offers for new or refinancing borrowers.

From a record high of 35 lenders offering cashback deals in March 2023, it has dwindled down to just 15 in July.

Out of the major banks, only ANZ is still sticking with a cashback deal, with a $3,000 cashback offer for first home buyers with loans of $250,000 or more, according to Canstar’s August data.

While inflation is still above the RBA’s target band and Reserve Bank governor Philip Lowe indicating that further tightening of monetary policy may be required in the latest cash rate announcement, forecasts are becoming cautiously optimistic that the end of the rate hiking cycle is near.

Cooper said that with the majority of banks starting to ease off on rate rises, it was a sign that the market had “reached the peak” or was “very close” to the end of the rises.

Rolling off record low fixed rates

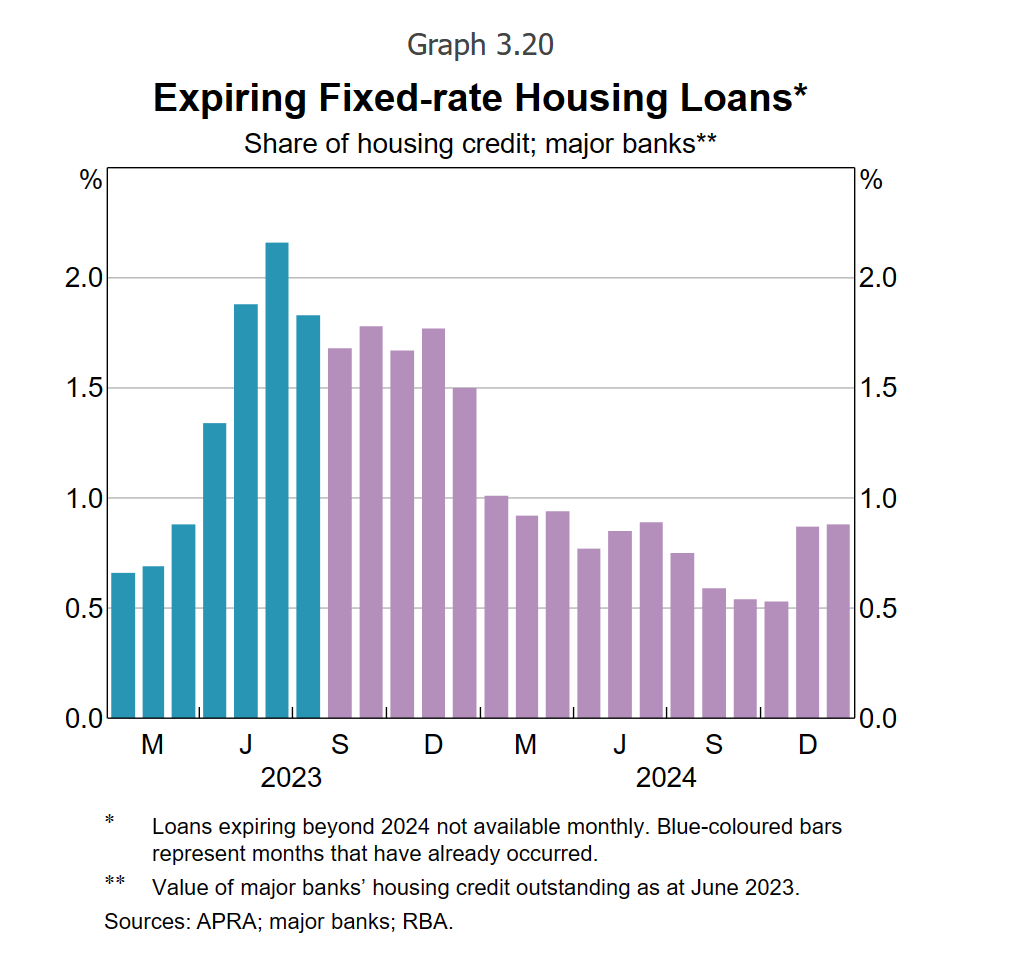

While the signs point to an easing of variable rates, there is still more pain ahead for those on fixed rates who are increasingly suffering from mortgage stress.

Overall, average outstanding mortgage rate has increased by around 275 basis points since May 2022, 125 basis points less than the cash rate, according to the RBA. This divergence largely reflects the high share of fixed-rate housing loans that are still outstanding.

The RBA said that the share of borrowers rolling off fixed-rate mortgages – taken out two to three years ago at low interest rates – onto much higher rates peaked at just under 5.5% of outstanding housing credit in the June quarter.

The central bank forecasts this to stay high for the rest of the year, peaking between July and December before declining in 2024.

As these expiries occur, a larger portion of borrowers will experience the impact of the increase in the cash rate since May 2022, leading to a continued rise in the average outstanding mortgage rate.

Still, according to Cooper, the process will be the same for brokers.

“Keep those relationships strong with the BDMs and work with them to reduce the carded rates alongside their pricing teams,” he said. “And touch base with your clients as much as you can to guide them through this environment.”

What do you think about this issue? Comment below.

{kind=link}