This one’s a little different. Normally these reports focus on a single company. Today we’re covering a very young industry with plenty of threats and controversies. So we’ll start with an overview of the cannabis industry and then look at three possible investment options to cover the different business models and risk profiles that can be incorporated into a balanced portfolio.

1. Executive Summary

In the middle of rising geopolitical tensions and a tech stock meltdown, it is easy for investors to feel there is nowhere to hide. That would be ignoring a sector with an expected yearly growth of 25% from 2022 to 2030. I am talking about the US cannabis industry.

It is an industry still in its infancy, facing complex regulations. It is still very fragmented, even if it is consolidating rapidly. It is also mired in controversy due to the illegal status of this product until recently in many states and until now at the US federal level. To top it all, it is also an industry famous for absurdly high volatility in valuation multiples.

These limitations have reduced the participation in the sector to retail investors only. Most institutional investors are simply unable to invest in the sector legally. This has led to extremely low valuation multiples during slumps and high funding costs for cannabis companies.

Nevertheless, ignoring a sector ready for explosive growth because it is still early can be a massive missed opportunity for investors. If you have the ability and the risk tolerance to invest in it, this could a unique opportunity to buy cheap assets before any large institutional investors can come and plow money into the sector. In this way, it is the opposite of early tech investing: only retail investors are allowed to get in early.

In this report, we will see how the industry works, what its future could hold, and 3 different ways to invest in it: a large recreational cannabis company, a medical cannabis company, and a cannabis-focused REIT (Real Estate Investment Trust).

This report first appeared on Stock Spotlight, our investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 rational investors!

2. Extended Summary: Why Invest in Cannabis?

The US Cannabis Industry

The US Cannabis industry has recently moved from an illegal black market to a fully legal and established line of business in almost half of the USA. This followed a massive change in the public’s perception of cannabis. It is also coming as a result of the realization of the flaws and negative impact of the so-called “war on drugs.”

Industry Overview and Legalization

Legalization is a state-by-state business, leading to an extremely complex regulatory landscape. The persistent Federal ban is a constant headache for cannabis companies and creates plenty of extra costs and inefficiencies. The hope of changes in legislation has created a very unstable market, with several cannabis bubbles rising and popping in just a few years.

A Selection of Cannabis Companies

In this section, we cover one of the largest, fastest-growing, and most profitable MSOs (Multi-State Operator) in the cannabis industry, a niche medical cannabis company in protected markets, and a dividend-yielding industrial REIT catering exclusively to the cannabis industry.

3. US Cannabis Industry

From Illegal Drug to Consumer Good

You might have strong feelings about cannabis. People have widely-ranging opinions on the topic: some say it’s an evil, life-destroying drug some say it’s a miracle of nature. This is going to be a report that stirs some controversy, but we’ll try to approach it purely from an investment perspective.

Before we study the industry, let’s look at the plant itself.

Cannabis is a common plant that’s quite easy to grow, hence its moniker of “weed.” The plant is also known as hemp and consists of 2 species: Cannabis sativa and Cannabis indica. Hemp used to be a commonly grown plant all over the world for its valuable fiber, which was used to make clothing, ropes, paper, and much more.

Most of the controversy is due to some varieties having psychoactive effects. These effects have been known for millennia by cultures ranging from classic Roman and Greek to Daoist Chinese and Sufi Muslims. Its usage has been on the rise since its discovery by the hippie culture of the 70s.

The psychoactive effect is mostly due to THC molecules. Another molecule of interest is CBD, which has no psychoactive effect but is nowadays considered beneficial for some medical conditions.

The psychoactive effect is relatively strong, in the range of alcohol, but weaker than so-called “hard drugs” like cocaine. Addiction is possible but seems to be less of a factor than it is with alcohol. While debated, it is generally recognized that consumption at a young age is to be discouraged, and abusive consumption has undesirable effects. Overdose is very rare, again, putting it below alcohol in terms of toxicity.

In the last decade, most Western countries have started to relax regulations around non-psychoactive cannabis-related products. Quite logically, making hemp-fiber shopping bags or anti-convulsion drugs is not that controversial. The same holds true for painkillers, cancer treatment, and anti-convulsive medications.

Full legalization, including for recreational purposes, is currently hotly debated.

The War on Drugs Debate

For many, cannabis is a drug, making it a different category than other milder substances like caffeine. I personally would put it on par with alcohol: a powerful psychoactive substance, but less dangerous and destructive than “harder” drugs like cocaine, methamphetamine, or heroin.

Prohibitionists tend to believe such substances should never be freely available. Remarkably, the same arguments were at the heart of the 1920s Prohibition period. Prohibition’s defenders argued that the destructive nature of alcohol, inducing violence, poverty, and addiction, fully justified its ban from public life.

Here I would fully agree that unlimited and unconstrained consumption of either alcohol or cannabis can be destructive to a person’s life. The problem for me with a prohibitionist stance comes with the social and economic consequences of prohibition.

The truth is that prohibition is rather inefficient at stopping the consumption of illegal substances. People seem to be ready to endure considerable personal or financial costs to keep consuming substances like alcohol or cannabis. Currently, half of adult Americans have tried cannabis in 2021. In 1985, before any sort of legalization was even on the horizon, it was already 30%.

Making desirable substances hard to find and illegal instantly creates a black market that gangsters can use to generate a high-profit margin. This is because the illegality creates scarcity, while the drug itself is cheap to manufacture, leaving a large potential margin for criminals.

The 1920 US alcohol prohibition notoriously created powerful criminal organizations like Al Capone’s. Alcohol consumption might have dropped a little, but the cost in the form of violent crimes and corruption proved to be unbearable for society as a whole.

The current prohibition is similarly funding criminal organizations, which use that money to run gang wars and other criminal activities. In recent years, it has become generally accepted that the “war on drugs,” started by Nixon in the 70s, failed.

Even if you personally disapprove of cannabis usage, it’s worth considering the possibility that moving that income stream away from violent criminals and transferring it to tax-paying legal companies might still be a good thing.

4. Industry Overview and Legislation

The Gradual Legalization of Cannabis

Currently, cannabis is legal in Canada, Uruguay, and several US states. Some US states and countries ban recreational use but authorized controlled medical use.

Several other countries like the Netherlands or Portugal have partially or fully decriminalized all usage of cannabis. Selling and producing are still illegal, but users are no longer prosecuted or imprisoned.

When looking at the US map, the situation is:

- Almost half of the country has legalized cannabis (44% of the population).

- A quarter has authorized medical usage and/or decriminalized cannabis.

- Cannabis is still illegal for the last quarter.

At the federal level, the drug is still fully illegal, putting federal law at odds with most state laws.

Federal law lags behind public opinion. Only 9% of American support a completely illegal status for cannabis. 31% support medical use only, and 60% support full legalization, according to the Pew Research Center.

This is also a bipartisan opinion that transcends divisions in an otherwise very polarized political environment. The only American groups with a majority opposing full legalization are Asian Americans, those 75+ years old, and conservative republicans. Even those groups do not differ that much when it comes to legalizing medical use.

Despite that general acceptance, 40,000 Americans are currently incarcerated for cannabis offenses.

Legal? Yes, But It’s Complicated

Legalization might sound like the endpoint for cannabis companies. They can now sell the product to anyone interested, right? Wrong!

When voting for legalization, state legislations wanted to keep tight control over an industry managing a recently illegal product. So each state has its own set of (somewhat arbitrary) rules, licensing limitations, special taxes, special controls, etc…

This has made the sector very complex, as the ever-changing regulations affect the business models and operation of cannabis companies. It has also affected the ability of the industry to compete with the illegal black market. If taxes and regulations are excessively pushing prices up, illegal supply is cheap enough to defend its market share. Over time, new tweaking of the cannabis laws tends to solve these issues, but recent legalization comes with a lot of legal headaches for cannabis companies.

As a result, the sector is now rather difficult to understand for outsiders. This is partly the reason why we decided to present companies that did not depend on selling on the fully legalized market.

Federal Hurdles

US federal classifies cannabis as a fully illegal Schedule 1 drug, the same classification it imposes on LSD, Mescaline, Ecstasy, and several other drugs.

Notably, banking has been a persistent issue for cannabis companies. This led many companies to sell their products and pay employees and suppliers only in cash. This creates costs and even risks (robberies) for the companies and their workers. It can also make taxes and tax audits extra complicated. Lastly, poor banking access limits the possible sources of funding through debt, leading to sometimes absurdly high costs of capital, sometimes above 10% or 15% rates for secured debt.

Speaking of taxes, there are also “sin taxes” at the state level, but also local municipal-level taxes. So from a taxation point of view, the cannabis industry is similar to the tobacco industry, except with even more complexity.

This is not necessarily a bad thing from an investment point of view, as tobacco has been one of the most profitable industries to invest in for the last decades. Complex regulation tends to protect the largest actor in the industry against the competition, cementing the leadership position by creating an artificial barrier to entry.

In addition to cannabis-specific taxes, regulations block the industry from benefiting from some tax deductions available to any other company. This effectively pushes the effective tax rate of cannabis companies to much higher levels than any other sector.

The Impact of 280E

| Industry | Non-cannabis | Cannabis |

|---|---|---|

| Revenues | $ 1,000,000 | $ 1,000,000 |

| Cost of goods sold | $ (500,000) | $ (500,000) |

| Gros profit | $ 500,000 | $ 500,000 |

| SG&A expenses | $ (200,000) | $ (200,000) |

| Pre-tax income | $ 300,000 | $ 300,000 |

| Taxable income | $ 300,000 | $ 500,000 |

| Federal tax (21%) | $ (63,000) | $ (105,000) |

| State tax (9,5%) | $ (28,500) | $ (47,500) |

| Net income | $ 208,500 | $ 147,500 |

| Gross margin | 50.0% | 50.0% |

| Net income margin | 20.9% | 14.8% |

| Effective tax rate | 30.5% | 50.8% |

Example of tax deduction effect –

Source: Green Thumb CEO2021 letter

The SAFE banking act, which would let banks work with the cannabis industry, has been pushed in the US legislature in various forms since 2013 but has never actually reached a vote. When it might happen is anyone’s guess, and the regular setbacks have played a big role in souring the mood of cannabis investors.

Another issue stemming from federal-level legislation is the prohibition of the interstate trade of cannabis, even between or among states that have fully legalized it. This creates a lot of inefficiencies, as cannabis companies are forced to operate in each state as a mini-independent operation instead of being able to scale up. Will that change? Most likely, but it’s anyone’s guess when. When it happens, it will most likely speed up the consolidation of the fragmented industry into a few leading companies, especially as it will let companies export cannabis from low-cost states to high costs states.

Lastly, but maybe of the greatest interest for this report, federal bans have created problems for listing cannabis companies on stock markets. Illegal activity cannot be promoted on markets like the main market of the NYSE or the Nasdaq. For these reasons, all major cannabis companies are listed in the less regulated OTC markets or on the Canadian stock market.

Institutional investors might be prohibited from getting involved in federally illegal transactions or buying companies trading on OTC markets. Many have internal policies against buying penny stock (companies whose shares are below $1). This means that 99% of institutional money is unable to invest in the sector. This, of course, had a negative impact on valuations, as the pool of available money is much smaller. Roughly 80% of US stocks are held by institutional investors.

The Many Types of Cannabis Companies

Here are the main business models that form the cannabis industry ecosystem:

Bulk Growers

These companies focus on growing a lot of cannabis efficiently at the lowest possible cost and selling it in bulk. This assumes a strategy where the buyer buys it like a commodity instead of as many differentiated products.

Initially successful, this model worked when there was a shortage in production. But it contradicts the nature of the product, which is more akin to tobacco (with strong brands and taste fidelity from consumers) than (for example) potatoes, a commodity where branding is nearly impossible.

Multi-State Operators (MSOs)

Multi-State Operators are companies selling cannabis in more than one US state. This gives them the scale to spread administrative, regulatory, and operating costs over larger operations. They will be the first to benefit from the lifting of restrictions on inter-state trade by, for example, centralizing their growing operations in the most efficient locations.

Medical Marijuana Companies

These might be focused only on non-psychoactive products (notably CBD) or on cannabis products in general. The difference with other MSOs is a focus on specific formulations aiming for a specific therapeutic effect. They are overall much less controversial than cannabis for recreational use and rely on medical prescriptions to support their sales, operating much like pharmaceutical companies. They are less dependent on full legalization.

Service Providers

The explosive growth of the industry has created an opportunity for other companies to help provide service to the industry. This can include companies selling farming equipment (including vertical hydroponic indoor farming), packaging, SaaS software for handling sales and operations, funding and financing, or, like one company below in this report, REITs building and operating the real estate infrastructure required to grow cannabis.

Future of the US Cannabis Industry

A Brief History of Cannabis Investing

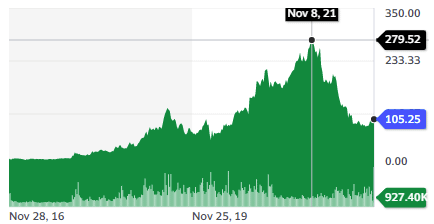

The first rush in cannabis investing followed Canada’s full legalization of cannabis for recreational uses in 2018 (medical use has been legal in Canada since 2001). Market reaction was a “green rush,” leading to massive gains, followed by the bursting of this “Cannabis Bubble 1.0” in 2019. At that time, the supply chain was far from established, and investor enthusiasm was certainly premature.

The second wave followed a series of individual US state legalizations. The narrative was that this would trigger quick legalization at the federal level. This would have grown the market dramatically, increased profitability, and allowed institutional investors to push stock prices higher.

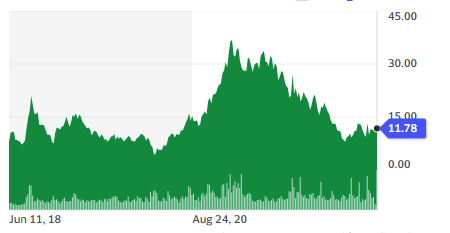

This did not happen. As a result, the US-centric cannabis bubble 2.0 burst as well in 2021. We can see this from the chart of the AdvisorShares Pure US Cannabis ETF (MSOS), a fund devoted exclusively to cannabis stocks:

After 2 bubbles in less than 4 years, early cannabis investors are rather burned out and despondent. I think the key part to surviving such a volatile sector is to adopt one of two strategies:

- Act like a trader and know when to take gains off the table

- Act like a long-term investor and ignore the short-term volatility.

In both cases, being aware of where we are in the cycle is important. After a drop of 80% in stock prices, we are likely closer to a new bottom than a top.

Long-Term Changes in the Cannabis Business

The constantly soon-to-happen but never-happening target is Federal legalization. One positive sign was the recent comment by Joe Biden (see tweet below), including the plan to change the way cannabis is considered as a drug:

The next steps in the coming years, before full federal legislation, are likely to be (in no particular order):

Positive events:

- SAFE banking act finally voted, allowing the cannabis industry to be banked “normally” and access capital at a lower cost.

- Interstate trade regulation allows for the transfer, at least of raw materials, at best of finished products, between states that both have fully legal recreational use.

- Generalization state by state or at the federal level of medical usage.

- More prohibitionist states decriminalize or authorize some usage.

- More medical-uses-only state switching to full legalization.

Some negative events might occur as well and this should stay in the mind of cannabis investors:

- Restrictions on products with very high concentrations of THC or CBD.

- Restrictions on products that are suspected to be too easily used by minors, like what recently happened to vape products.

- An increase in taxation by cash-strapped municipalities and states.

Any of these could add additional headwinds to the sector.

5. A Selection of Cannabis Companies

In the short term, the cannabis industry is highly exposed to the rumor mill regarding new state or federal-level legalization. This does not change the fundamentals of the industry:

- Strong demand for a product that has lost its stigma with most of the population and is regularly used by tens if not hundreds of millions.

- A substance as addictive as tobacco and alcohol.

- A sector where premium branding can create significant barriers to entry and higher margins.

- Non-recreational use cases (medical cannabis) are almost fully normalized today and are increasingly accepted by the medical community.

These factors explain the strong growth projections for the US market.

Because of these strong fundamentals, I have selected 3 companies offering different risk levels as possibilities for exposure to the industry.

5.1. Green Thumb Industries (GTBIF)

Quick Stock Overview

Ticker: GTBIF

Source: Yahoo Finance

Key Data

| Industry | Cannabis/MSO |

| Market Capitalization ($M) | 3,119 |

| Price to sales | 3.1 |

| Price to Free Cash Flow | – |

| Dividend yield | – |

| Sales ($M) | 998 |

| Free cash flow/share | $- |

| Equity per share | $7.22 |

| P/E | 33.6 |

The company offers a wide range of cannabis products, from “classical” cannabis to burn (including pre-rolled like a cigarette) to vaping concentrate, edible candies, and pastilles. It also has a line of medical cannabis in the form of essential oils, balms, creams, and concentrated extracts.

The company operates 77 shops in 15 states, covering 50% of the US population, with 4,000 employees, making it one of the largest MSO companies.

The company is looking to acquire licenses and expand in both legal markets where it is not yet active (Oregon, Washington, etc…) and is entering or has just entered states with newly opening markets (Virginia, Rhode Island). It also entered Minnesota through an acquisition.

Most of the expansion to new states seems to be using a strategy of buying a smaller license-holding competitor in a state where Green Thumb does not operate yet. Once the license is acquired, they expand by progressively opening new shops in that state. So far, Green Thumb has been mostly focused on states where cannabis is fully legalized.

The company’s main revenues come from smokable products (vape + flowers). Consumers’ tastes are evolving beyond the usual “joint” to other product categories previously unavailable from illegal street vendors, with flower sales growing at a slower pace than the rest of the product selection.

Beyond the growth from new legalizations, same-store sales are growing by 10% per year. This is unlikely to reflect a rise in total consumption, as most studies show little overall increase in consumption after legalization. This is more likely to reflect a growing trend of replacing illegal supply with established legal brands and increased customer fidelity.

Green Thumb has sold and leased back its growing facilities in 2019 and 2020 (more on lease-back when we discussed the third company covered in this report).

The rationale behind this move was to have a more flexible production capacity and to move toward an industry structure where MSOs require less capital for expansion (leasing instead of paying directly for new greenhouses). Growing and manufacturing are still handled internally.

Financials

When looking for a good MSO to feature in this report, I was surprised to notice how many failed to be profitable. Green Thumb consistently turns over a profit, which was a big factor in picking this company over its competitors. This way, if federal legalization takes a lot longer than expected or if capital markets close up (recession, financial crisis), the company would not be put at risk the way its cash-burning competitors would.

85% of the company stock is floating, and insiders’ stock options and warrants are not a risk of significant dilution (less than 5% of total stocks).

The company grew its revenue by 15% year-to-year with a stable income per share. EBITDA margin has been somewhat stable in the 25%-35% range.

Its P/E ratio is 33. Free cash flow is negative at -$91M due to a large $214M in CAPEX. The company has $145M in cash for $253M in debt. Total assets, excluding goodwill and intangibles assets (from acquisitions), are $1.17B, compare to $0.75B in total liabilities.

Debt was secured at an industry low of 7% rates (which tells you a lot about how bad it can be for Green Thumb’s competitors) and has been recently refinanced in 2020.

At this cash spending level, the company is not at any immediate risk but might be forced to slow down expansion or raise more money (through stock sales or debt) in the next 2 years if cash flow does not improve.

Conclusion

Green Thumb has a good business position and product/brand selection, combined with a solid balance sheet. It has a rather typical profile for a growth stock (rather high P/E, high CAPEX to fund growth), with the bonus of being already profitable and having cash flow-positive operations and positive free cash flow.

This puts the company in a relatively safe position regardless of the pace of legalization and of normalization for the cannabis industry. Would this happen slower than expected, the reduced need for CAPEX would likely turn it cash flow positive. It would even give a good opportunity for further acquisition of distressed, less profitable, or less cautious competitors.

Alternatively, would the SAFE banking act be voted or interstate trade authorized, the company, with its established network, should be able to optimize its operation even further.

Overall, Green Thumb seems like a reasonable way to bet on the major MSOs consolidating the sector into a profitable oligopolistic industry.

5.2. MariMed (MRMD)

The Healing Virtues of Cannabis

MariMed is a cannabis MSO focused on wellness and health rather than the recreational side of the industry. The Company has been active since 2012. It operates as a vertically integrated business “from seeds to sale,” operating 300,000 square feet of cannabis facilities.

The company aims to be more technical, scientific, and technology-driven than its competitors. It is also more centered around medical and food products compared to traditional cannabis for smoking.

Quick Stock Overview

Ticker: MRMD

Source: Yahoo Finance

Key Data

| Industry | Medical cannabis |

| Market Capitalization ($M) | 183 |

| Price to sales | 1.6 |

| Price to Free Cash Flow | 97.2 |

| Dividend yield | – |

| Sales ($M) | 129 |

| Free cash flow/share | $0.01 |

| Equity per share | $0.14 |

| P/E | – |

MariMed’s Operations

The company operates in 6 states, with only one dispensary per state, with the exception of 4 dispensaries in Illinois. This put MariMed at a much smaller scale than some of its larger MSOs competitors (like Green Thumb).

MariMed is focused on states with limited licenses, which allows it to be one of the dominant actors in these areas. It also means the company is less dependent on rapid and generalized legalization for its immediate future. Instead, the limited licenses provide it with protection through high barriers to entry in these markets.

Each state has a maximum number of dispensaries authorized for one company. This means MariMed can be authorized to triple or quadruple the existing number of dispensaries, depending on the state.

Besides the focus on limited licenses, the smaller scale comes from a focus on profitability, with careful and slow CAPEX and acquisitions.

MariMed has made extra efforts to develop its own varieties of cannabis plants. This was done by building a large library of cannabis plant genetics. Improved proprietary horticultural methods are also part of the company’s assets.

The company operates an array of brands catering to different needs and market niches:

- Heritage: for the more green and nature-focused consumers.

- Betty’s Eddies: Candies and ice cream with compound mixed specially to help with stress, pain, or sleep problems.

- Bubbies Baked: Organic brownies with cannabis.

- Vibations: Hydrating energy drink with caffeine and cannabis, quite far away from the usual “stoner” image.

- K Fusion: low-dose chewable tablets.

- Florance: non psychotropic CBD based pills and medicine

- It is also reselling partner brands: Healer, a supplier and training platform for doctors willing to learn about cannabis-based treatments; and Tikun Olam, the leading medical cannabis product in Israel.

That variety allows the company to tap different niches within the medical cannabis market.

Financials & Valuation

MariMed’s EBITDA margin stands at 35%, among the highest in the industry, something that played a large role in picking the company. (Green Thumb’s EBITDA margin is 25%-35%).

Revenues grew to $121M in 2021, up 142% year-to-year. EBITDA grew similarly by 142% year-to-year. Growth is expected to slow down for 2022 to the 5%-15% range.

Regarding valuation, some dilution needs to be incorporated in the price calculation. This comes from preferred stock, options, and warrants, which are equal to 30% total basic shares outstanding. In addition, the company has the right to issue more stock (up to double the current count, see page 15 of the annual report). So while strong dilution is not certain, it is a risk to consider.

The company has $29M in cash, matching the $27M in current liabilities. The $59M in long-term liabilities are split between $22M in debt and $37M in preferred securities.

The company is free cash flow positive ($2M), even with an $18M CAPEX. P/E is high at 51, with the company having turned a positive net income only since 2020.

Conclusion

MariMed has strong brands, efficient vertically integrated operations, and positioning in selected markets with high barriers to entry. It is profitable, though not as much so as Green Thumb. It is also not growing as quickly.

The main strength of MariMed is its positioning in the food supplement and medical markets instead of the more classic recreational uses. This gives it a hedge in case legalization takes a slow pace and medical cannabis stays the main market for half of the US.

The opposite is also true. A speed-up legalization could threaten MariMed with the arrival of bigger competitors in its (for now) protected markets.

The medical angle also makes it an investment more friendly to people reluctant to invest directly into recreational marijuana but acknowledging its potential as a medical treatment for pain, stress, sleep disorders, PTSD, spasms, etc… (9 out of 10 Americans support medical cannabis legalization).

Lastly, its valuation is not high when considering the price-to-sale ratio but includes a lot less built-in growth than for larger, more aggressive MSOs. The company is somewhat profitable but will need to cut CAPEX to really turn cash flow positive.

5.3. Innovative Industrial Properties (IIPR)

The boom in cannabis sales has created an entire ecosystem for service providers to cannabis-selling companies. Industry-specific software or marketing services are difficult to judge, as this is a sector evolving very quickly.

More constant is the basic requirement of any cannabis operation: growing the plant itself and in industrial quantities. Some companies like MariMed have insisted on keeping all their operations integrated, allowing them to focus on unique plant genetics.

Others, like Green Thumb, are happy to keep their sparse and expensive capital to feed growth, licensing to newly legalized states, and acquisitions to open new markets. This is the core of IIPR’s clients, as it builds and operates greenhouses dedicated to cannabis cultivation.

Quick Stock Overview

Ticker: IIPR

Source: Yahoo Finance

Key Data

| Industry | Cannabis REIT |

| Market Capitalization ($M) | 3,196 |

| Price to sales | 11.7 |

| Price to Free Cash Flow | 14 |

| Dividend yield | 6.3% |

| Sales ($M) | 248 |

| Free cash flow/share | $0.84 |

| Equity per share | $69.81 |

| P/E | 22 |

REIT structure and dividends

IIPR is structured as a REIT (Real Estate Investment Trust). This means it essentially deals with real estate properties, in this case, industrial properties dedicated to cannabis cultivation.

To learn more about REITs, you can consult my article about them here.

To learn more about REITs, you can consult my article about them here.

As a REIT, IIPR has to distribute at least 90% of its taxable income to its stockholders. This means that this is one of the only cannabis industry-focused investments that also gives away a strong dividend yield. The company started giving growing dividends in 2017 and is now distributing a yield of 6.5%.

The company is one of very few following this business model. IIPR stands at $3.2B in market cap. Its two next competitors are NewLake Capital Partner ($320M capitalization), and Power REIT ($30M), which is not exclusively a cannabis-centered business.

IIPR was founded by Alan Gold, previously the founder and manager of BioMed Realty Fund, which was, until its sale in 2016, managing laboratories and production facilities for the biotech industry.

IIPR Assets & Clients

IIPR operates 110 assets all over the USA. This includes both greenhouses and laboratories to extract the active compounds.

Because every plant variety has different requirements, with different goals in terms of THC, CBD, and other chemical compound production, plant growth has to be done in a very regulated environment.

So IIPR focus on delivering optimal growth conditions for all the possible requirements of its clients. Indoor cultivation allows for the perfect mix of nutrients, light, temperature, and humidity to obtain a more potent product and much higher cultivation yields all year round.

Due to its scale, IIPR can also build the greenhouse facilities at a cost advantage, as it has a massive scale and negotiating power when it comes to sourcing equipment like sensors, piping, electrical (lamps, heater, etc…), ventilation, security, etc… Being a REIT and not a cannabis MSO, it also has access to capital at lower rates than its (still unbanked) clients.

| Indoor | Characteristic | Outdoor |

|---|---|---|

| ~60 days | Growth Period | 2 – 8 months (depending on region, seasons, weather, etc.) |

| 5 – 8 cycles | Cycles per Year | 1 – 3 cycles |

| ~0% | Loss Factor | >0% |

| Superior | Product Quality | Inferior |

| $472/lb. | Cost to Grow | $214/lb |

| ~$1,250/lb | Sale Price | ~$420/lb. |

| 80% | Cultivation Prevalence | 35% |

Difference between indoor and outdoor cannabis cultivation –

Source: IIPR presentation: U.S. Cannabis Sector Primer

Profitability and Risks

Industrial cannabis facilities command a higher average rent price per square foot than traditional industrial facilities ($30 versus $10). The leases are also very long (15-20 years) compared to the average 5-year length for classic industrial leases. All maintenance, capital repair, and replacement costs are paid by the tenant during the full length of the lease (triple net leases).

This high profitability compensates for the inherently more risky profile of the cannabis sector. Most MSOs are not yet profitable, focusing their money on quick expansion.

This makes IIPR tenants inherently riskier than tenants of other, more traditional REITs. Currently, no tenant represents more than 14% of the total portfolio, which at least diversifies the risk of a specific tenant not paying its rent.

IIPR’s yield on invested capital stands at 13%, down from its historic highs of 16% in 2018. The company expected this yield to decline over the next decade to stabilize in the 10%-12% range. This would still put it way above the average REIT’s yields of 6%-8%.

The high degree of customization of IIPR’s assets to its client’s requirements is a bit of a double-edged sword:

- On the positive side, it makes substitution costs very high for IIPR’s clients and puts high barriers to entries for potential competing REITs.

- On the negative side, it reduces IIPR pricing power. The pool of cannabis operators is limited and shrinking quickly, with the sector consolidating through M&A. In addition, new cultivation techniques or changing products requirement could make some details of the greenhouses obsolete earlier than expected.

One strong sales argument of IIPR is the Sale/Leaseback, business model. Essentially, IIPR buys facilities from established MSOs and leases them back. By doing so, IIPR act as a provider of liquidity to the MSOs, freeing money to redeploy toward accelerating expansion. Stronger growth, in turn, increases the need for more of IIPR’s greenhouses by the MSOs.

IIPR Valuation

IIPR real estate is worth $2.2B at cost, slightly less than its current market cap of $3.2B. Other assets are equivalent to all liabilities, including long-term debt. So would put the Market Cap to NAV (Net Asset Value) ratio at 1.45. This ratio would make IIPR appear overvalued, as REITs should trade close to their NAV.

However, we need to consider the real value of the properties instead of how much they cost years ago. Inflation has been especially strong on both real estate prices and base materials. So I assume the replacement costs of the greenhouses are much higher than what they cost a few years ago.

Prices for machinery, steel, aluminum, piping, glass, ventilation systems, etc… have gone up radically, sometimes up 100% for some components of greenhouses.

As a result, I suspect that IIPR’s market cap to NAV is slightly below 1 (maybe 1 to 0.8).

Remarkably, this also means that the company was grossly overvalued at the end of 2021. It is pretty rare to see REITs drift far apart from their NAV. Normally these are rather “boring” investment vehicles that fluctuate little year-to-year.

But it seems the company was caught up in the general cannabis bubble enthusiasm. This should be something to remember for investors in IIPR in the future. Any significant rise above the NAV should be a warning and might justify selling the stock until the valuation comes back in line with the valuation of a “normal” REIT.

Conclusion

IIPR is an interesting way to bet on the cannabis industry for conservative investors who are unwilling to take chance with the more risky MSOs. It also provides a steady income in the form of dividends.

The current valuation seems roughly in line with NAV, especially when taking into consideration recent inflation and the real replacement costs for the company’s extensive network of greenhouses and cannabis extraction facilities.

As an extra bonus, it seems markets have in the past been willing to pump up IIPR’s stock price in tandem with the rest of the industry, despite its REIT status. So there is a chance that IIPR provides upside optionality in addition to the relatively “safer” downside protection from its real estate assets.

Lastly, investors in IIPR should stay aware that its industrial real estate properties are less fungible than for simpler REITs dealing – for example – in apartment buildings. The properties are highly specialized and would need extensive (and expensive) refitting to be used for another purpose than cannabis growing.

If you liked this report, there’s more where this came from! We publish reports like this one every month over at Stock Spotlight.

Subscribe for free and join over 9,000 rational investors!

6. Conclusion

The cannabis industry is still a very young sector. As a result, it is also highly unstable and subject to abrupt changes in both regulation and market conditions.

It is also one of the fastest-growing industries, replacing an enormous but previously illegal market. In the last 10 years, public opinion has radically shifted, with the legalization of at least medical cannabis now an almost society-wide consensus.

Evolving public opinion combined with the appeal of a new source of tax revenues is rapidly changing the political trend regarding the drug. Most likely, it is a matter of when, not if, for cannabis use to be at least decriminalized and likely fully legalized. So the prospects of the industry in a long enough timeframe (5-10 years) are good.

The timing of these changes is more uncertain. Cannabis promoters have a history of being over-optimistic about “imminent” legislative reforms. This has led to no less than 2 successive bubbles popping in less than 4 years. So any potential investor in cannabis should be ready to adapt to extreme volatility and act as much as a trader as a long-term investor.

We are likely to see cannabis operators continuing to consolidate the industry. This would mean the sector might end with an oligopoly of a few companies, something to be expected when an activity is extremely regulated. This trend would benefit Green Thumb.

Even extensive consolidation could still leave space for profitable high-end niches, especially in the non-smoking segments of the market, foodstuff and medical especially. This trend would boost MariMed.

In both cases, there will be a constant demand for highly professional cannabis growing facilities, IIPR’s specialty.

Because of the incertitude about the future structure of the cannabis sector, it is best for investors to diversify their exposure to the industry.

For this purpose, I think it might be interesting to look beyond the companies featured for building a diversified portfolio. So contrary to other reports, I will give a passing mention to other actors in the sectors:

The big 4 beside Green Thumb are CuraLeaf, Trulieve, Verano, and Cresco Labs. They have been aggressively acquiring their smaller competitors in the hope of turning into THE dominant actor in the industry. Of this list, only Green Thumb and Verano are currently profitable.

Other MSO options are the ETF MSOS (providing built-in diversification), Tilray, Aurora Cannabis, or Canopy Growth.

If you are more interested in a “pick and shovel” option similar to IIPR, you might want to give a look at GrowGeneration, the largest hydroponic supplier in the US, and AFC Gamma, a loan provider to the cannabis industry.

Holdings Disclosure

Neither I nor anyone else associated with this website has a position in BWXT, SMR or SNN or plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation from, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this article.

{kind=link}