Disclaimer: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!!

What better day to publish a post about an Italian company than Ferragosto, the Italian Public Holiday where virtually any Italian family is somewhere close to a beach and Italian offices only are staffed with the most junior person to take up the telefone in order to say: “No one here, please call next week/next month”.

With Italmobiliare, I fell deeply into a rabbit hole, which lead to a quite extensive analysis. Due to some problems with the WordPress editor, I wrote it with a different Editor and have attached the PDF with the full version. In the blog post I’ll focus on the executive summary, the Pro’s and Con’s and the return expectations. The rest of the gory details can be read in the attached PDF document.

Executive summary:

Italmobiliare (IM) is an Italian Holding company with a market cap of ~1 bn EUR that underwent 2 pivots in its 40 year history as a listed company. The first pivot, in the 1990s, from conglomerate to Cement (Italcementi) and then once again in 2017 after a 2 bn sale to Heidelberger into an Italy focused, “Quality-growth small/mid cap PE” style investment company.

What makes the company very attractive to me, is a very interesting portfolio (including at least two potential “Super Star” holdings), decent value creation, good strategy/transparency and especially a 50% Discount to NAV.

In my opinion, the main reason for the discount is that the story and the quality of the portfolio is not well known and Italian Holdco’s are maybe not the most popular investments right now.

On the other hand, this potentially represents an attractive return/risk profile for the patient investor even without the presence of a “hard” near term catalyst.

Potential Catalysts

Overall, there is clearly no hard catalyst. “Soft” catalysts would be a continuous good or even great performance of the flagship companies and maybe a larger exit in the next 2-3 years. An IPO or even a sale of Caffe Borbone for instance could make a big difference. Or if Santa Maria grows 30-50% p.a. for some, investors might notice as well.

If, and this is a big IF, a share buy backhappens, even a smaller one could compress the discount, but I would not bet on it. The biggest hope would be that the other employees, who also are incentivized based on NAV, keep pressuring their boss who maybe has a much longer time horizon.

Another possibility could be of course once again an activist investor, but I would have no idea who this could be. The absence of such a catalyst might be part of the explanation for the high discount and why Italmobiliare is not very well known.

Valuation/Return expectations

Italmobiliare is not a Serial Acquirer but a “buy and sell” Investor. Therefore, in my opinion, the NAV is the best valuation metric. A consolidated “look through” EV/EBIT valuation or similar does not make a lot of sense due to the heterogeneity of the portfolio. This is also one of the reasons why the stock doesn’t screen well. Screeners only show book values, not NAV.

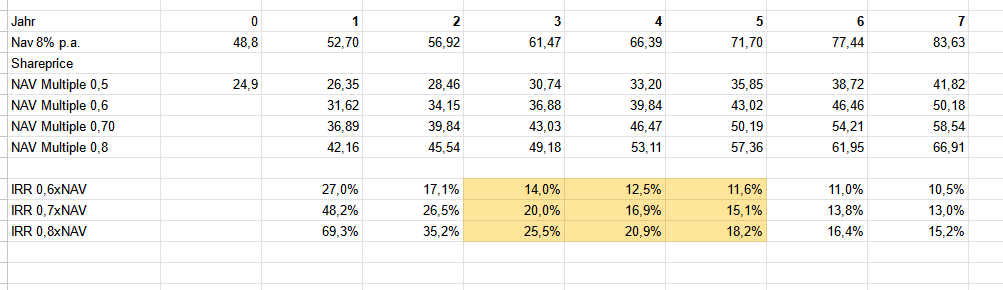

Based on this, the return expectation has two main parameters: NAV growth and assumed discount to NAV. If the discount remains 50% and they manage to increase the NAV with 8% p.a. (incl. dividends) then the return will be 8%. If however the discount narrows, then returns could be Turbocharged.

The following table shows the IRRs based on an 8% NAV growth, a share price of 60-80% of NAV along the time axis.

The orange box is the area that I think is realistic. In the low case, it takes 5 years to reach 60% of NAV which will return 11,6% p.a. (incl. dividends). In the best case, I will double my money after 3 years if the share price reaches 80% of NAV in this time. Of course , returns could be better or word, but I think that the “expected” return is something like 15-17% p.a. over 3-5 years. Which I think is attractive.

Pros/Cons

As always, even after a quite excessive deep dive, time for a Pro/Con list:

+ Significant discount to NAV

+ No holding debt (only at participation level) or other structural issues

+ good reporting

+ interesting portfolio with some potential “Star Companies” (Caffé Borbone, Prof. Santa Maria)

+ does not screen well

+ story is not well known

+ Family owned, owner operated, aligned incentives

+/- pretty OK NAV track record (8% p.a.)

– partial “Family office” character

– Holding cost + taxes

– No “hard” catalyst

Summary

Overall, I do think that Italmobiliare is a very interesting case. The current transformation doesn’t seem to be well known, but in my opinion, Italmobiliare is a very interesting “family investment” vehicle run by a very smart owner operator.

Their portfolio looks interesting and has good growth potential. The only disadvantage is the absence of a “hard catalyst”. This however is compensated by a more than comfortable discount of 50% to the NAV.

For the patient investor, this creates a great opportunity over a time horizon of at least 3-5 years. Therefore I allocated 3,3% of the Portfolio into Italmobiliare at 24,20 EUR per share.