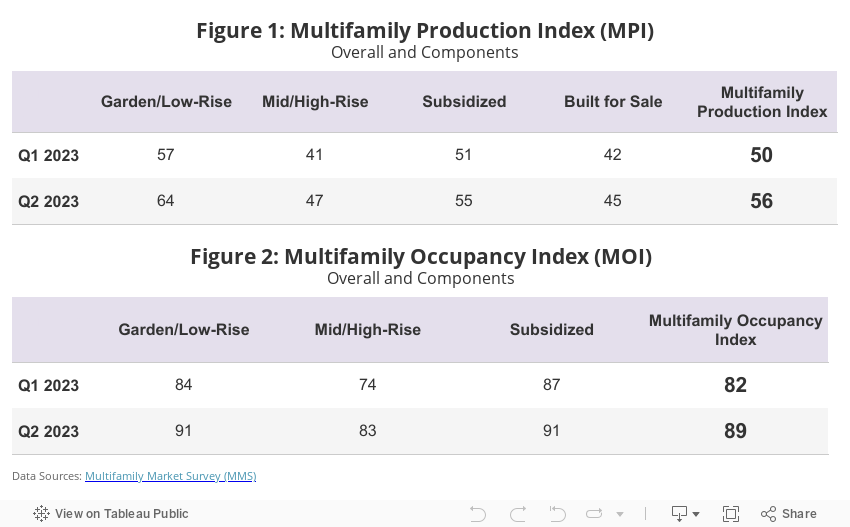

Confidence in the market for new multifamily housing was in positive territory for the second quarter, according to results from the Multifamily Market Survey (MMS) released today by the National Association of Home Builders (NAHB). The MMS produces two separate indices. The Multifamily Production Index (MPI) had a reading of 56 for the first quarter while the Multifamily Occupancy Index (MOI) reading was 89.

The MPI is a weighted average of four key market segments: three in the built-for-rent market (garden/low-rise, mid/high-rise and subsidized) and the built-for-sale (or condominium) market. The survey asks multifamily builders to rate the current conditions as “good,” “fair, or “poor” for multifamily starts in markets where they are active. The index and all its components are scaled so that a number above 50 indicates that more respondents report conditions are good than report conditions are poor. For the second quarter, the component measuring garden/low-rise units had a reading of 64, the component measuring mid/high-rise units had a reading of 47, the component measuring subsidized units had a reading of 55 and the component measuring built-for-sale units had a reading of 45 (Figure 1).

The MOI is a weighted average of three built-for-rent market segments (garden/low-rise, mid/high-rise and subsidized). The survey asks multifamily builders to rate the current conditions for occupancy of existing rental apartments in markets where they are active as “good,” “fair” or “poor”. Similar in nature to MPI, the index and all its components are scaled so that a number above 50 indicates more respondents report that occupancy is good than report it is poor. For the second quarter, the components measuring garden/low-rise and subsidized units each had a reading of 91 and the component measuring mid/high-rise units had a reading of 83 (Figure 2).

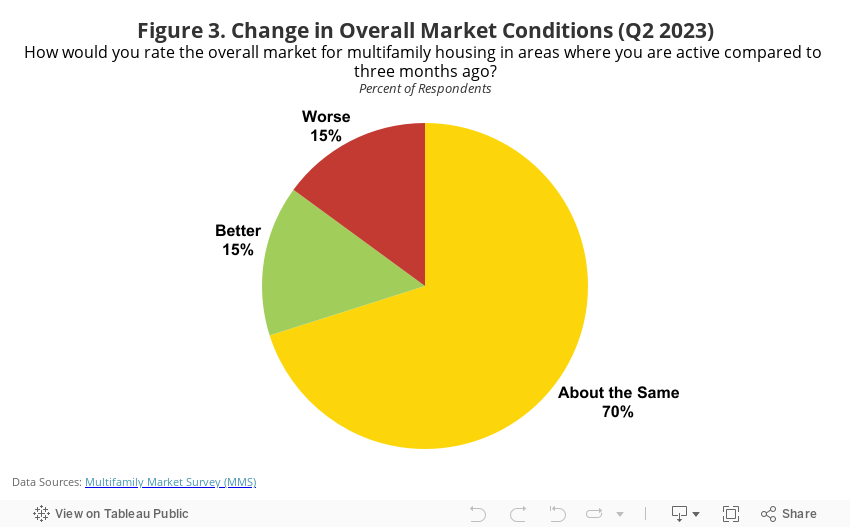

Because the previous version of the MMS series can no longer be used to compare with this quarter’s results, the redesigned tool asked builders and developers to compare market conditions in their areas to three months earlier, using a “better,” “about the same” or “worse” scale. Seventy percent of respondents said the market is “about the same” as it was three months earlier while 15 percent each indicated market conditions were “better” or “worse” (Figure 3).

Even though demand for multifamily housing remains solid due to the low availability and the high cost of single-family homes currently on the market, builders and developers face headwinds which are limiting new development and creating problems for getting projects approved in many parts of the country. The “measured hawkishness“ from the Federal Reserve is causing tighter lending standards which is adversely impacting the multifamily sector. This combined with local concern over supply and significant increases in operating expenses explain why NAHB is forecasting that multifamily starts will decline during the second half of 2023. Property, casualty and liability insurance has also emerged as a major issue facing the multifamily industry, further constraining new supply.

Please visit NAHB’s MMS web page for the full report.

Related

{kind=link}