Mastek Ltd. – Cloud Transformation Partner

Mastek, is a turnkey and trusted digital engineering and Cloud transformation partner that delivers Innovative solutions and business outcomes for clients in Healthcare & Life Sciences, Retail, Manufacturing, Financial Services, Government/Public Sector, etc. It enables customer success and decomplex digital for enterprises by enabling them to unlock the power of data, modernize applications to the Cloud, and accelerate digital advantage. A preferred Oracle partner with a strong pool of 2000+ Oracle experts and 100+ industry-specific solutions. Mastek’s ~5500 strong workforce operates out of 40+ countries (in the UK, Americas, Europe, Middle East, and APAC) to deliver business value with velocity. MST Solutions, a Mastek company, is a Summit-level Salesforce consulting partner trusted by several Fortune 1000 enterprise clients.

Products & Services:

The company’s primary services include application development, application maintenance & support, ERP and cloud migration, business intelligence & analytics, agile consulting, assurance & testing and digital commerce.

Subsidiaries: As on FY23, the company had 22 subsidiaries.

Key Rationale:

- Established Position – Mastek’s established business profile is supported by its strong track record in the digital transformation business and healthy presence in Oracle cloud-based solutions implementation through Evosys. The company now also has presence in the Salesforce consulting business with the acquisition of MST Solutions. The company’s key service lines include digital application engineering, including application development work, cloud native development, DevSecOps work, and cloud and enterprise application, which includes implementation of Oracle cloud and enterprise applications. Mastek has a strong track record in the Government & education, Health & life Sciences, Retail, Manufacturing and Financial services verticals with each generating 45%, 15%, 12%, 17% and 11% respectively, of total revenue in Q1FY24.

- Recent Acquisition – Mastek Inc. has informed that it has approved to sign the definitive Membership Interest Purchase Agreement to acquire the 100% Membership Interest of BizAnalytica LLC. BizAnalytica LLC is an independent data cloud and modernization specialist in the Americas region. The purchase consideration includes an upfront payment of $16.72 million and an earn-out of up to $24.0 million subject to achieving financial targets. The indicative time period for completion of the acquisition is expected to be, on or before September 30, 2023.

- Q1FY24 – Revenue from operations stood at Rs.725 crore in Q1FY24, up 2% QoQ/27% YoY. Revenue growth was driven by demand for Digital Engineering, Experience, and Cloud Transformation services. Middle East and USA have shown robust performance, while the UK was impacted by fewer working days in the quarter. Geographically, Middle East recorded strong growth, up 33.5% QoQ/57% YoY. Key market Europe declined, down 1% QoQ while US and ROW declined 0.5%/3% QoQ. EBITDA margin stood at 17.5%, down 20 bps QoQ. The 20-bps reduction was largely due to increments which was offset by currency and other operating levers. Net Profit stood at Rs.74 crore was flat QoQ and a decline of 12% YoY. The Company added 22 new clients in Q1FY24. Total active clients during Q1FY24 were 436 as compared to 464 in Q4FY23. As on 30th June, 2023, the company had a total of 5,592 employees. Last twelve months attrition at 20.4% in Q1FY24 in comparison with 21.0% in Q4FY23.

- Financial Performance – The 5 Year revenue and profit CAGR stands at 26% and 33% respectively. The balance sheet of the company is strong with a debt-to-equity ratio of 0.2x. 12 months order backlog of the company is around Rs.1,763.9 crore ($215.0 million) in Q1FY24, as compared to Rs.1,509.3 crores ($191.1 million) in Q1FY23, up 16.9% in rupee terms and 9.7% in constant currency terms on YoY basis and Rs.1,794.1 crore ($218.3million) in Q4FY23, down 1.7% in rupee terms and decline of 2.6% in constant currency terms on QoQ basis.

Industry:

India’s technology industry revenue is estimated to be $245 Bn in FY23. Technology exports at $194 Bn, are expected to grow at 9.4% in reported currency terms. In FY23, the technology industry is estimated to have 5.4 Mn employees and contribution of 53% in India’s service exports. With 23 new unicorns, India became the 2nd highest country in terms of number of unicorns added in 2022. 1300+ new tech startups emerged in 2022. Indian software product industry is expected to reach US$ 100 billion by 2025. By 2026, widespread cloud utilisation can provide employment opportunities to 14 million people and add US$ 380 billion to India’s GDP. Indian companies are focusing on investing internationally to expand their global footprint and enhance their global delivery centres. Indian SaaS companies saw 2x growth in share of global markets. India has as many as 59 number of SaaS unicorns and potential unicorns. Internet connections rose to 83.69 crore in 2022 from 25.15 crore in 2014.

Growth Drivers:

- In the Union Budget 2023-24, the allocation for IT and telecom sector stood at Rs. 97,579.05 crore (US$ 11.8 billion).

- The computer software and hardware sector in India attracted cumulative foreign direct investment (FDI) inflows worth US$ 94.92 billion between April 2000-March 2023.

- Over 45 new data centres to come up in India by 2025. Data centres in India attract investment of $10 Bn since 2020.

Competitors: Cyient, Zensar Technologies, etc.

Peer Analysis:

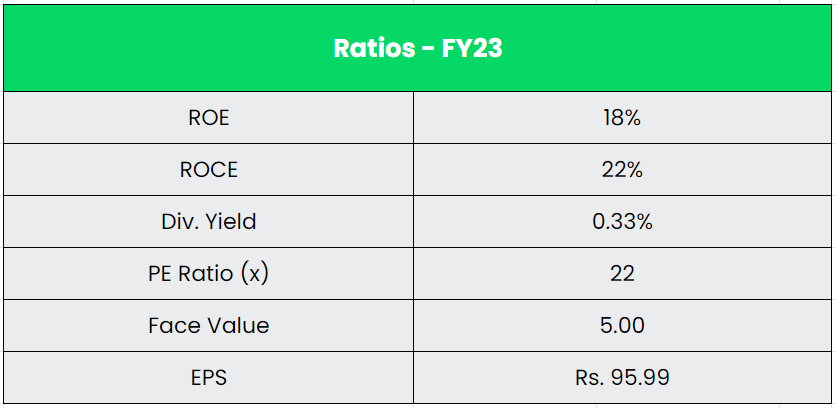

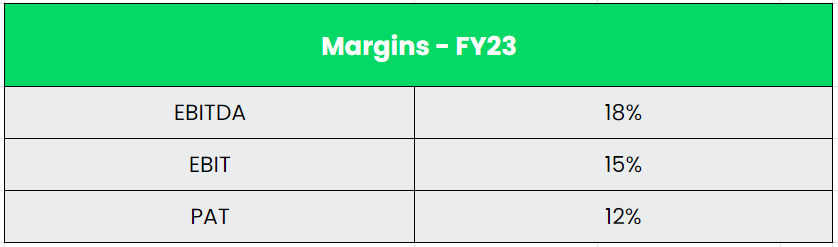

In terms of fundamentals, Mastek is way better than its peers with high return ratios and margins. Also, Mastek is trading at a discount (P/E) when compared to its competitors.

Outlook:

The management conveyed their contentment with the order book in the US and Americas region, notwithstanding certain deals requiring extended finalization periods. They foresee robust revenue growth stemming from consecutive order bookings in this geographical area. In the UK, substantial deals are in the pipeline, evoking optimism. The management affirmed that in the ongoing quarter, with incremental progress, minor margin fluctuations might arise, yet the company aims to restore a margin range of 17% to 19% by Q3 and Q4. The company expressed a sanguine growth outlook both quarter on quarter and year-on-year, striving for industry-leading expansion. Mastek has cultivated a steady and foreseeable revenue stream from the UK’s public sector in recent years, propelled by the UK government’s introduction of the Digital Outcomes and Specialists (DoS) framework in 2016 as a successor to the Digital Services-2 framework. The management indicated that the momentum of revenue growth in the UK public sector will persist in upcoming quarters due to amplified expenditures on digital transformation initiatives by the UK government and the acquisition of new clients. Additionally, an acceleration of growth momentum in the US business is anticipated, attributable to strong demand for integrated digital commerce solutions, burgeoning deal sizes, and the addition of new clientele.

Valuation:

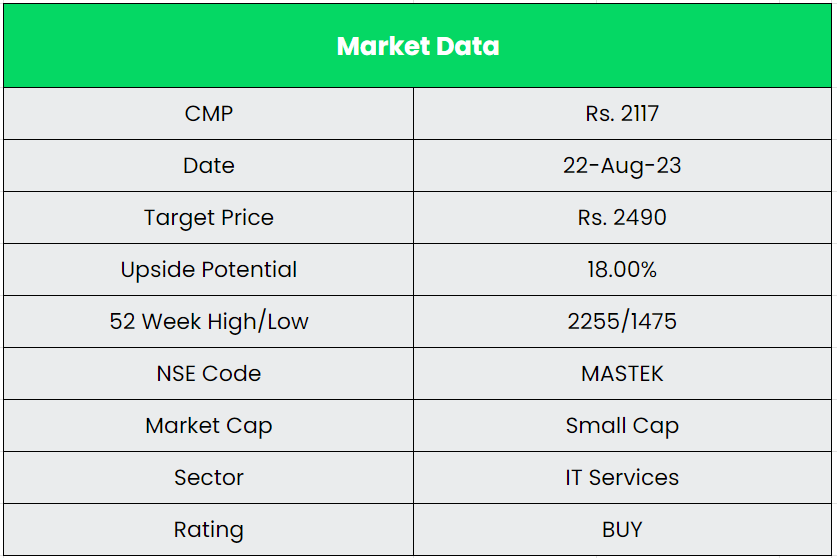

We believe the company is well placed due to the complete package portfolio, the strong tie-up with the UK public sector as well as the momentum in both Americas and Middle East markets which is delivering the strong growth. We recommend a BUY rating in the stock with the target price (TP) of Rs.2490, 18x FY25E EPS.

Risks:

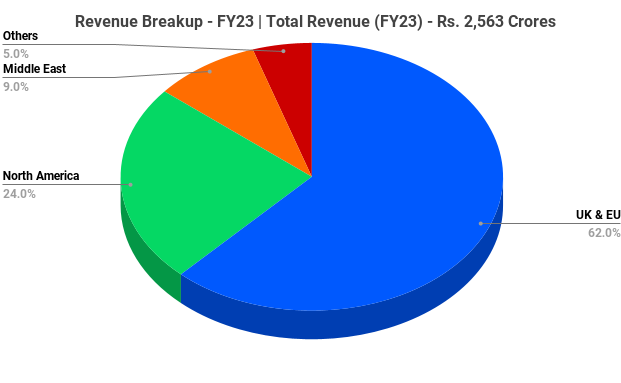

- Concentration Risk – Mastek derived 62% of its operating revenue in FY2023 from the UK and EU markets. The company continues to generate most of its revenues from the UK’s public and healthcare sectors, which exposes it to risk of any changes in the UK Government’s policy on IT spending.

- Competitive Risk – Given the intense competition in the industry, Mastek’s profit margins are susceptible to pricing pressures and wage inflation.

- Forex Risk – Much of the revenues and margins are exposed to forex risks, although Mastek’s hedging mechanisms mitigate this risk to an extent.

Other articles you may like

Post Views:

10

{kind=link}