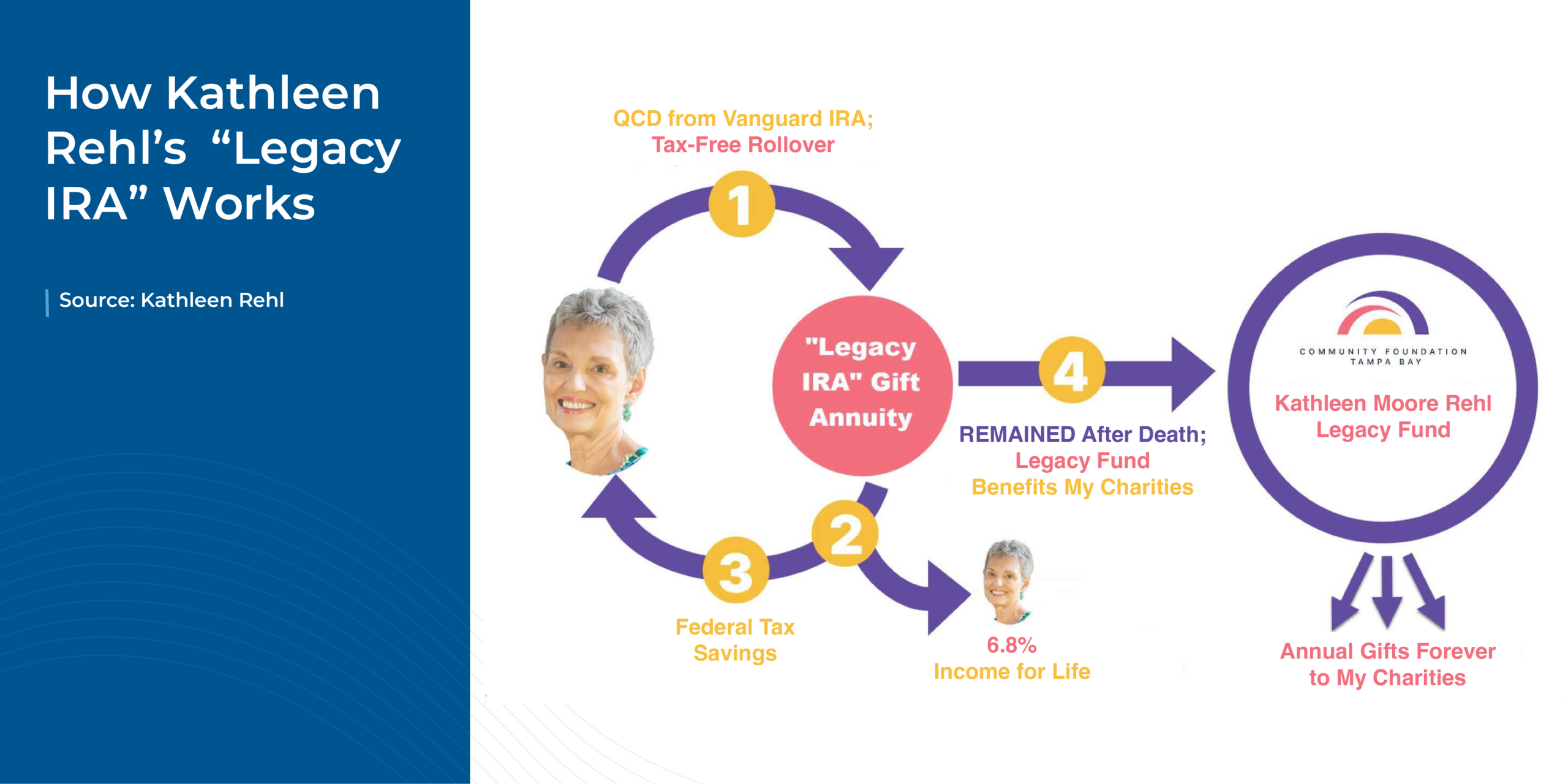

Charitable Gift Annuities (CGAs) have long been a popular way for individuals with charitable intentions to plan their legacies. By contributing a lump sum to a charity in exchange for fixed recurring payments for life (with any leftover funds after the donor’s death going to the charity), the individual can ensure that their funds are directed towards a purpose that aligns with their values, while also retaining a steady source of income for the rest of their life. However, the caveat with current CGAs has been that they could only be funded with after-tax dollars before the donor’s death, meaning that if an individual only had tax-deferred funds (e.g., in an IRA or 401(k) plan) to contribute to the Charitable Gift Annuity, they would need to withdraw – and be taxed on – those funds first. Testamentary CGAs, on the other hand, can be established after a donor’s death, funded with IRA or other assets to provide income for another person. But the SECURE 2.0 Act, passed in December 2022, created the ability for individuals over age 70 1/2 to make a one-time Qualified Charitable Distribution (QCD) of up to $50,000 of IRA funds into a CGA, with the amount distributed to the CGA being excludable from the donor’s taxable income.

In this guest post, Kathleen Rehl, a semi-retired financial advisor and educator now focusing on her own estate planning considerations, shares her experience with creating her “Legacy IRA” rollover to a Charitable Gift Annuity to support her chosen nonprofits after Congress passed the SECURE 2.0 legislation at the end of 2022.

The potential benefits of the new Legacy IRA rules are threefold. First, they allow donors to enhance their charitable giving legacy and ensure their future charitable intentions are fulfilled. Second, they reduce the donor’s tax bill in the year the CGA is created by excluding the amount contributed to the CGA from taxable income. And third, they create a stable lifetime income stream that can be paid to the donor and/or their spouse.

All of which is important during a time when members of the Baby Boomer generation, who have accumulated unprecedented levels of wealth compared to previous generations, are preparing to make decisions on how to balance their intentions for transferring that wealth – whether that be passing it on to the next generation of family members or friends, or providing for causes that are meaningful to them – with their own needs for sustainable retirement income. And while a Legacy IRA may only be one piece of the puzzle (since the $50,000-per-person lifetime limit may only represent a small portion of the assets of many high-net-worth families), it can still serve as a unique and valuable legacy and tax planning tool – and given the minimal expense and hassle of setting up and maintaining the CGA (since the charitable organization typically handles all of the administrative aspects of doing so), there may be no reason for any individual with charitable intentions and lifetime income needs not to use it to the extent that the one-time $50,000 limit allows!

Ultimately, for financial advisors, the Legacy IRA can be one part of a broader toolkit for helping retired clients with values-based, purposeful legacy planning. By understanding the eligibility requirements and rules around the new law and gift annuities in general, and having a ‘recipe’ that clients can follow for establishing their own Legacy IRAs, advisors can help plant the seeds with their clients around strategic giving (while also differentiating themselves to potential new clients as a go-to resource for estate planning and charitable giving)!

{kind=link}