I had mentioned it several times in the past: I don’t think it makes sense to do quarterly updates on portfolio companies, as some of my holdings don’t even report quarterly and it would take away a lot of time.

It is also weirdly fascinating to watch how many investors seem to see quarterly earnings as something of a holy grail that you must follow and react on as quickly as possible (“Beat -buy” etc.). Personally, I prefer to let the dust settle and then, with a time lag of a few weeks have a look at earnings if they are roughly in the direction I had initially envisaged. Sometimes you might miss the best time to sell, but more often in my opinion quarterly earnings are very “noisy” and distract from a longer term picture. I also deliberately ignore analyst expectations and only measure earnings against my own expactions.

Nevertheless, looking at the portfolio every 6 months or so makes some sense. As not all companies report timely, I split this into 2 parts.

So let’s jump into the first part (in no particular order, sorry for that. I will look at Admiral, Alimentation Couche-Tard, Logistec, SFS, TFF Group, Thermador, Solar Group, DCC, Sto, Italmobiliare, Sixt, Nabaltec and Schaffner.

- Admiral

Admiral had reported 6 months results a few days ago and the market seems to have been positively surprised. In Admiral’s case, which is a long term holding (~9 years), I actually did “re-underwrite” the stock last year in July, so it makes sense to compare against my business case from last year.

2022 EPS turned out to be 1,24 GBP per share against my estimate of 1,20 GBP. So far so good. However, the 0,576 GBP EPS per share for the first 6M are a bit on the low side if they want to reach my estimated 1,47 GBP EPS for 2023.

One thing that is worrying me a little bit is that still, all the other activities besides UK motor, in aggregate are producing a small loss. For instance, I do not understand, why after 5 years, the “Admiral loan” division is not making profits. And expense ratios are still creeping up, too, especially in UK motor. In the “old days”, they had something like 15-17% of expenses, now they are at 22% in UK motor and has been going up every year without a good explanation.

Somehow my feeling is that they are losing their edge in the UK and the rest of the activities are mostly threading water. If the cycle is turning for Car insurance, than Admiral will be most likely a good investment for the next 6-12 months but because of the cost issue, I will put them on “mid term watch”.

One obvious mistake that I made with Admiral was to think that they would do better than FBD. I sold FBD in April 2022 because I was worried about inflation.

Looking at the stock price, keeping FBD instead of Admiral would have been a lot better.

2) Alimentation Couche-Tard

ACT had released its annual numbers 2022/2023 end of June already. The past financial year was a good one for ACT, with EPS up around +20%. They keep buying back shares and increase their dividend.

They continue to acquire businesses, the biggest one the Total gas station activities in Europe for 3,1 bn EUR. Margins have been increasing, Returns on capital (ROE/ROIC) too. The trailing P/E is 17,5x, next year’s according to analyst’s 16,5. The stock is clearly not cheap, but considering the quality is also not too expensive. I would say that this is a “keeper”.

3) Logistec

Logistec is one of my more recent holdings. Very luckily, they announced a “strategic review” which could result in a potential M&A transaction which pushed the share price significantly up. On the operating side, things look good. Sales and profits are up double digits. Short term, the biggest risk here is clearly that the strategic review ends up being a dud, but operationally the business seems to do well. Nothing to do here for the time being.

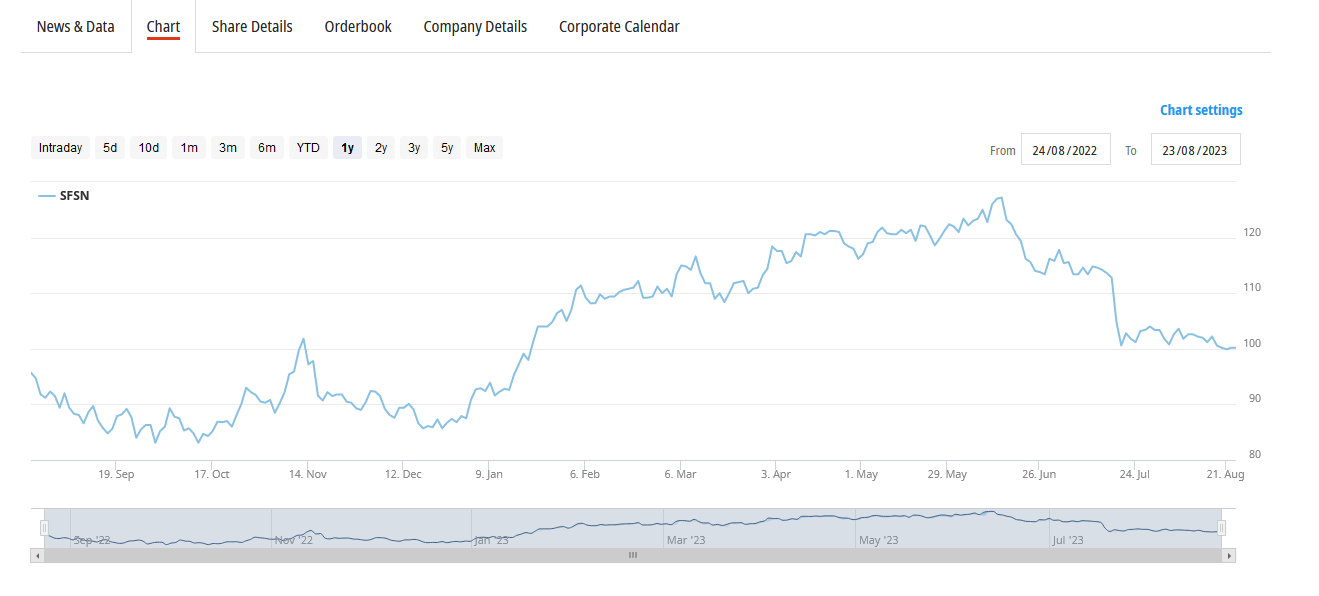

4) SFS

SFS reported 6M numbers a few weeks ago. In a nutshell, the Hoffmann Acquisition seemed to have worked well, whereas the core business has been suffering a little due to a slow down in Asia.

Distribution and Logistics, that includes Hoffmann, was ~50% of EBIt for the first 6M 2023. The market seems to have been disappointed from these result:

After selling Meier & Tobler and the take over offer for Schaffner, SFS is currently my only Swiss investment. This is one where I might add on weakness, provided that we don’t run into a full fledged recession.

5) TFF Group

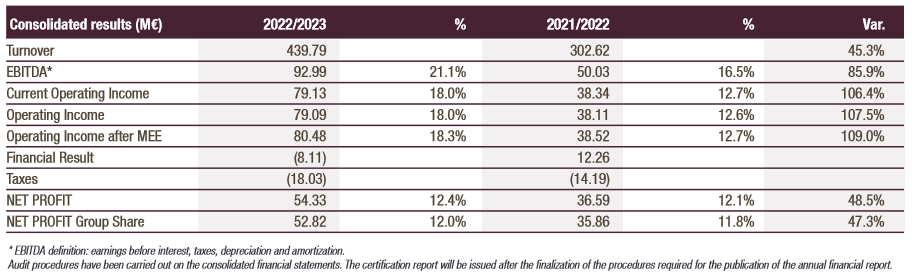

Finally, after some delays, the US business really kicked in and delivered a “monster year” 2022/2023 for TFF Group. This is from the annual report released in mid July:

For the current year they predict a growth rate of +10%. With a 17x trailing P/E and a forward P/E of ~15 according to TIKR, the stock is not expensive for the quality it offers. I have been holding TFF now for more than 12 years and I expect to hold it for some years more.

6) Thermador

Thermador has issued very decent 6M numbers, although Q2 was a lot weaker (~2-% you) vs Q1 which still showed growth of +10%.

Thermador will clearly be affected by the slowdown in housing, but the exposure should be manageable and in the past, Thermador has used to take over competitors and/or adjacent businesses at attractive valuations.

7) Solar Group

Solar was clearly one of my weaker picks in the last few years. I bought them while identifying them in my “All Danish Stock series” as 2022 was a very good year for them and they traded at around 6-7x 2022 P/E.

My thesis was that especially the focus on everything electrical should shield them to a certain extent for the interest rate driven slowdown in construction. Whereas Q1 2023 still looked good, Q2 was already significantly weaker than last year.

Management however confirmed their initial outlook of 900 mn DKK EBITDA for 2023. This would be roughly the amount of 2021 and still ~80% higher than pre pandemic 2019. Assuming that they manage to deliver, this would mean ~60 DKK EPS and a P/E of 8. I actually listened to the earnings call and they were quite optimistic about the situation. In addition, the acquired large heat pump business looks like a nice “free option” to the upside.

So despite the negative performance, Solar Group is a stock that I will continue to hold as fundamentally things look pretty OK.

8) DCC Plc

DCC’s annual 2022/2023 numbers and EPS were overall roughly in line with my expectation or rather at the higher end. The Q1 trading statement was a little bit weaker. The energy business is still doing very well, but the two smaller segments are struggling a little bit.

DCC still expects decent growth in all relevant KPIs. Excluding purchase price amotization, DCC trades at ~9x P/E which for such a high quality business is very cheap. But patience is clearly required here as the stock is maybe also suffering some kind of Uk malus.

9) Sto SE Prefs

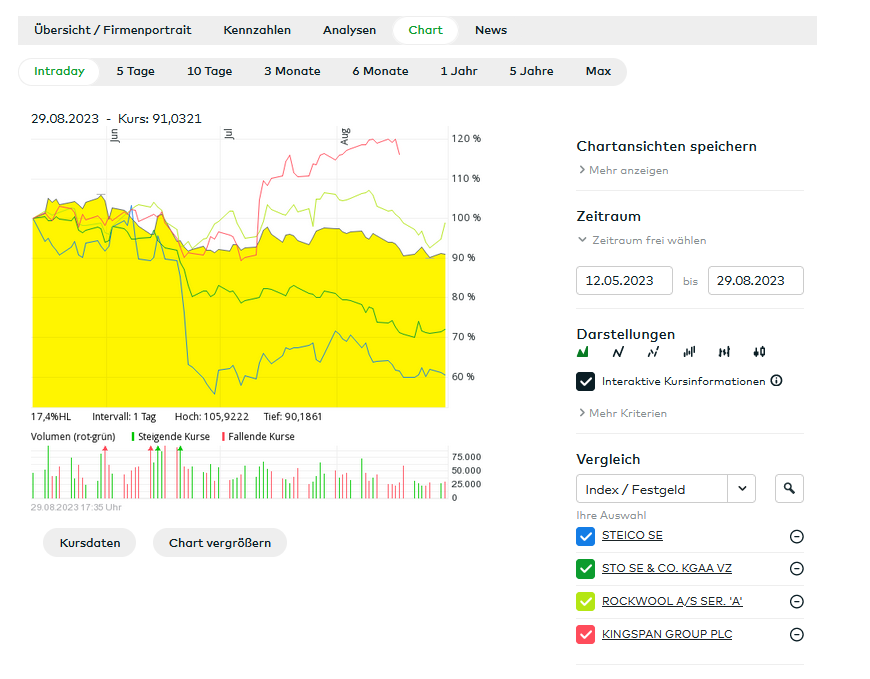

My investment and especially the increase in Sto, the German based maker of insulation systems, turned out to be badly timed. The stock is down more than -20% from my entry point. Clearly, the currently dramatic slow down in new built construction activity play a role, but also the delay in German policy making on renovation and heat pumps didn’t help.

Nevertheless is was my own decision to concentrate on Sto in May and so far this turned out to be a bad decision, as only Steico performed worse (despite the announced take over by Kingspan):

Interestingly, Sto’s half year numbers were not so bad. They reduced their sales forecast but stuck to their profit forecast, which, to tell the truth, is a wide range.

Sto currently trades at around 10x 2023 P/E and 6x EV/EBIT, has net cash and is well equipped to profit from a (in my opinion) inevitable renovation boom. Despite all the other factors (KgAA, pref shares), this is extraordinarily cheap.

The only question is how deep the fall in new construction will be and how hard this will hit Sto. There clearly is a risk that they might reduce their profit outlook for this year.

Sto is clearly a “pain trade” but in my opinion, these investments often turn out to be the best ones. On further weakness, I might increase the position as I am quite optimistic that this will turn out well over the next 3-5 years despite the strong current headwinds.

10) Italmobiliare

There is not much to add since my recent write up. The only new thing to mention is that the CEO, Carlo Pesenti is buying stock on a daily basis as can been seen here in this overview.

Interestingly, this is not published on their own website. I did increase the position slightly to 4% of the portfolio in the meantime.

11) Sixt Pref

Despite very good Q2 numbers, Sixt shares have given up much of their 2023 gains in the recent days as can be seen in the chart:

At the current level, the pref shares are valued at a single digit P/E ((7-8) which I find quite cheap considering the track record of Sixt. Especially their move into the US seems to pay off quite well and in my opinion adds significant growth runway going forward.

12) Nabaltec.

The timing of the initial Nabaletec investment in the beginning of February 2022 was “not optimal” to put it mildly, 3 weeks before the invasion of Ukraine started and the world changed. As a energy-intensive chemicals business with the main operation in Germany, this clearly was not long-term positive for Nabaltec.

Initially, Nabaltec actually profited from Supply chain issues as I outlined in a June 2022 post. It looks like that companies ordered extra material at whatever price in 2022.

Looking at the stock price, Nabaltec has suffered more than other chemical companies as can be seen in this chart.

Nabaltec’s Q1 2023 was still Ok, however the second quarter was really not good. Although Sales are “only” down -4% you for the first 6M, profitability has declined by almost half. The 2023 outlook had already been significantly reduced in the beginning of August. Operationally, both, the “old” business as well as Boehmit sales are far behind expectations.

Using their guidance mid-pont, 2023 would result in an EBIT of 14,6 mn EUR, significantly lower than the 29 mn in 2022 and 24,6 mn in 2021. This is clearly below my initial case, although 2022 was significant above my initial case.

I am currently really unsure what to do here. It seems that Management really seems to have been surprised by the downturn in 2023. The currently expected EBIT Margin midpoint of 7% would be the lowest one since 2011. This seems to be reflected in the share price which has dropped to levels to 6 years ago. The big question is if and how they can reach the profitability levels from the earlier years or if the business is somehow permanently impacted.

There is clearly a risk that this could happen, i.e. that profitability remains lower due to higher energy prices in Europe for the foreseeable future and maybe competitors could gain a lasting competitive advantage. On the other hand, my understanding was that their products are not so easily replaceable due to quality requirements etc.

So overall this is clearly a position to watch closely. At the moment I would neither sell nor increase the position.

13) Schaffner

As mentioned in the blog, the take over offer came as a total surprise. My best guess is that after reorganizing Schaffner for quite some time, the largest investor Buru wanted to see some money sooner rather than later and jumped on this opportunity.

As I don’t want to bet on the Swiss Franc until the offer gets finally closed, I have started to sell down the position.