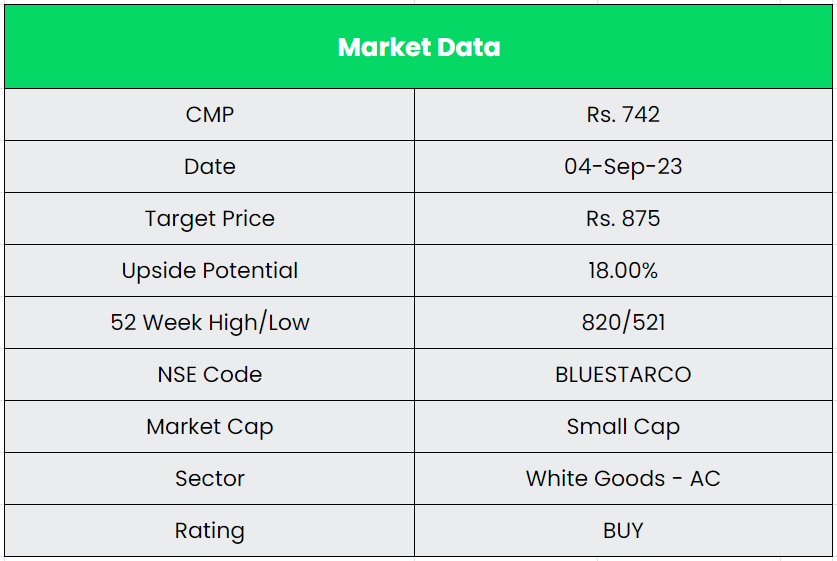

Blue Star Ltd. – Diversified Cooling Solutions

Blue Star is India’s leading air conditioning and commercial refrigeration company, with an annual revenue of over Rs.7,000 crore, a network of 32 offices, five modern manufacturing facilities, and 4,040 channel partners. The company has over 8,000 stores for room ACs, packaged air conditioners, chillers, cold rooms as well as refrigeration products and systems. Blue Star’s integrated business model of a manufacturer, contractor, and after-sales service provider enables it to offer an end-to-end solution to its customers, which has proved to be a significant differentiator in the marketplace. The company fulfils the cooling requirements of a large number of corporate, commercial as well as residential customers. Blue Star has also forayed into the residential water purifiers business with a stylish and differentiated range, including India’s first RO+UV hot and cold-water purifiers as well as air purifiers and air coolers.

Products & Services:

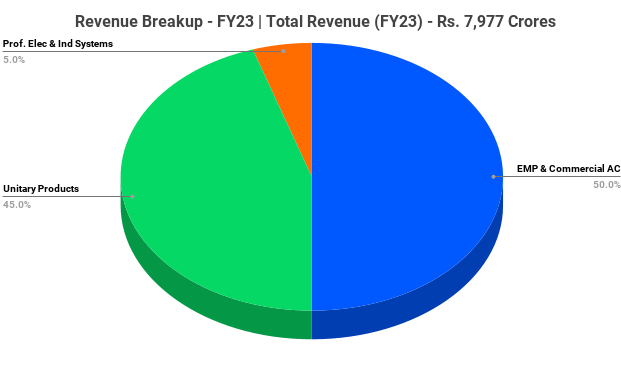

The Company caters to three types of segments.

- EMP (Electro-Mechanical Projects) and Commercial Air Conditioning systems – This segment covers the design, manufacturing, installation, commissioning and maintenance of central air conditioning plants, packaged/ducted systems and Variable Refrigerant Flow (VRF) systems to Commercial Buildings, Retail, Hospitals, Hotels, Education, Industrial Facilities, etc.

- Unitary Products – This segment focuses on a wide range of contemporary and highly energy-efficient room air conditioners (RAC) for both residential as well as commercial applications. It also manufactures and markets a comprehensive range of commercial refrigeration products and cold chain equipment. The range of unitary products further includes water purifiers, air purifiers and air coolers.

- Professional Electronics & Industrial Systems – This segment includes solutions and system Integration in MedTech, Industrial Systems and Data Security through the company’s subsidiary, Blue Star Engineering & Electronics Limited.

Subsidiaries: As on FY23, the company has 9 subsidiaries and 2 Joint Ventures.

Key Rationale:

- Strong Market Position – Blue Star is one of the strong players in the consumer durable business, particularly in commercial, RAC systems and across project business in related segments with an established track record of over six decades and demonstrated capabilities in executing projects across project businesses in domestic and international markets. It commands a leadership position in ducted AC segment, while #2 position under variant refrigerant flow (VRF) and chiller product segment. As on March 31, 2023, the company has 13.5% market share in RAC alongside extensive distribution network with over 8,000 stores.

- Diversified Profile – Presence in EMP & Commercial and Unitary Products (Mostly B2C) segments mitigates the risk of slowdown in any one segment or industry. Blue Star relies almost equally on both these segments in terms of revenue and profitability. The Unitary Products segment contributed to around 45% of revenue in FY23, with EBIT margin of around 8% and the contribution of EMP segment was higher at 50% with EBIT margin of ~7%. The company is also becoming self-sufficient by commencing new manufacturing facilities in both RACs as well as commercial refrigeration, which would lead to a reduction in its dependency on imports and cost savings, led by backward integration. It will also help the company to tap the export markets.

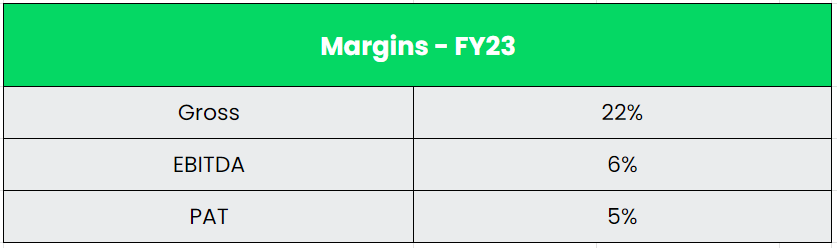

- Q1FY24 – Blue Star’s Q1FY2024 consolidated results were impacted by muted performance of the RAC business. Revenue came in at Rs.2,226 crore (up 13% YoY). Gross margin improved to 22.2% (up 110 bps YoY). EBITDA grew by ~18% YoY to Rs.145 crore. EBITDA margin inched up by ~30 bps YoY to 6.5%. Net profit growth was restricted to ~12% YoY to Rs.83 crore due to the steep increase in the interest cost. The orders gained during Q1FY24 is Rs.1225 crore as against Rs.1366 crore on Q1FY23. The total pending order book as on Q1FY24 stands at Rs.5106 crore (64% of the FY23 revenue). While there were fewer orders from the commercial building sector, the company witnessed healthy bookings from factories and data center sectors.

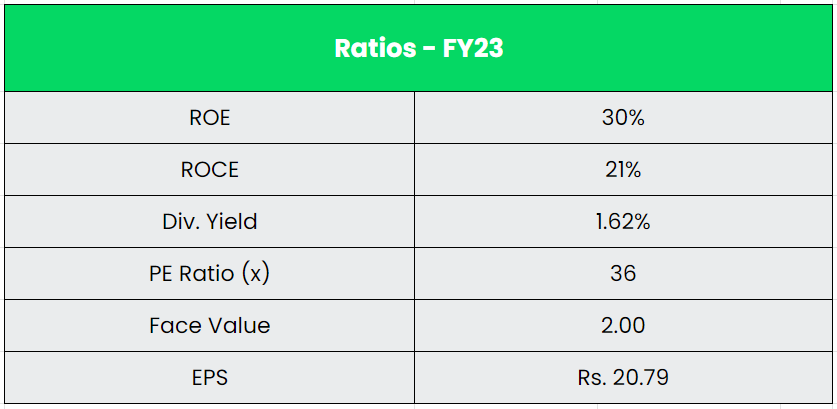

- Financial Performance – The 3 Year revenue and profit CAGR stands at 14% and 24% respectively between FY20-23. The company plans capex of ~Rs.750 crore in the next three years, which is likely to be funded through QIP, subject to board and shareholders’ approvals. The major portion of the capex is likely to be executed in FY2024 and FY2025. Despite significant investments in manufacturing capacity expansion, continued focus on margin improvement and working capital efficiency enabled improvement in ROCE.

Industry:

The White Goods market is estimated to cross $21 Bn by 2025 expanding at a CAGR of 11%. Domestic manufacturing contributes nearly $4.6 Bn on an average to this industry. The Indian room air conditioner market is likely to reach USD 5 billion by FY28 with a compound annual growth rate (CAGR) of 10%. According to the Power Industry, the market share of the more efficient, variable speed (inverter) RACs (room ACs) increased from 1% in FY16 to 77% in FY23, while that of the fixed speed RAC, reduced from 99% to 23% during the same period. The overall market for room ACs reached 6.6 million units by 2020-21 from 4.7 million units in 2015. The volumes of the RAC industry are expected to post a 15-20% growth in FY2024 following the robust growth of 26-28% in FY2023. The cumulative share (by volume) of four and five-star inverter RACs is expected to increase to 30-40% in FY2025 from 20-23% in FY2022. AC Exports increased at a CAGR of 9% from $165 Mn in 2018 to $233 Mn in 2022.

Growth Drivers:

- Compared with a global average of 30%, only 7% of Indian homes have air conditioners, according to various studies and estimates. Even if the penetration increases to 10 or 12% in the next four or five years, it will translate into millions of air conditioners, signifying the huge growth potential.

- Constantly rising temperatures and extended summers in India has made Air Conditioners a necessity rather than a luxury in Indian households.

- Government has launched a PLI Scheme for AC manufacturers which offers incentive of around Rs.6238 crore. The production-linked incentive (PLI) scheme to help reduce imports dependence on components to 20-30% from the current levels of 60-70%.

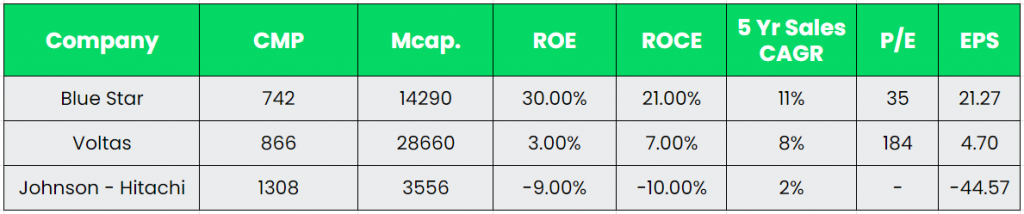

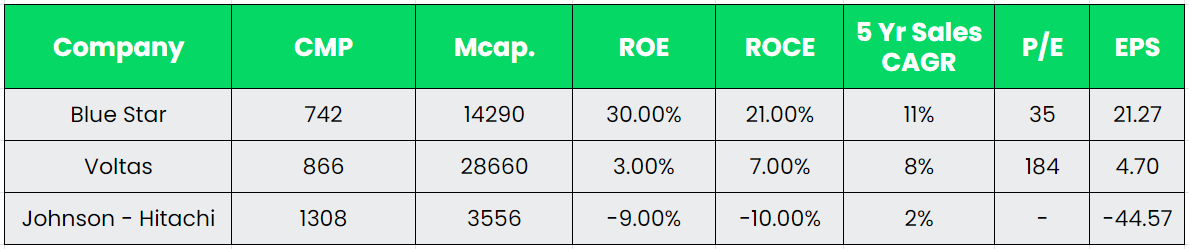

Competitors: Voltas, Johnson Controls – Hitachi.

Peer Analysis:

Voltas and Johnson – Hitachi are the close competitors of Blue Star, having A/C business as their main segment whereas Lloyd’s is one of its many business segments by Havells. In terms of fundamentals, it is clear that blue star is having the upper hand in every aspect.

Note – P/E is based on TTM EPS.

Outlook:

Blue Star has maintained its leadership position in the conventional and inverted duct air conditioning system, deep freezers, storage water coolers, and modular cold rooms. It has received orders from Foxconn Bangalore, IOCL Baroda, and Mindspace Thane for its recently launched centrifugal chillers. In Q1FY2024, the RAC industry has declined by 10% YoY, while the dip in the company’s business was lower than that due to a large share of institutional sales. Management has revised down its revenue guidance for the RAC business to 10-15% for FY2024, similar to the industry’s growth levels, from its earlier guidance of around 15-20% YoY growth. EBIT margin for FY2024 would be in the range of 8.0-8.5%. Blue Star’s strategy is to invest in and build both B2B and B2C businesses as strong engines of growth. Also, the Management’s near-term goal is to cross the total revenue of more than Rs.10,000 crore. The company’s market share has improved from just 12.3% in FY19 to 13.5% in FY23 and it aims to grow the same to 15% in the next 2 years.

Valuation:

We believe Blue Star will continue to capture the market share from its competitors through dealer and capacity expansion. The company also plans to explore export opportunities in countries like USA and Europe. We recommend a BUY rating in the stock with the target price (TP) of Rs.875, 50x FY25E EPS.

Risks:

- Regulatory Risk – All the businesses in the Company’s Unitary Products segment are seasonal in nature. Unforeseen weather patterns such as extended winter, pleasant summer, less than normal monsoon, excess monsoon or any kind of disruptions during the peak selling seasons may impact the revenue growth.

- Competitive Risk – Several Indian and global players in the air conditioning business are in the process of setting up or expanding their own manufacturing facilities in India to tap the underpenetrated market. Such players could resort to aggressive pricing to capture market share leaving the company vulnerable to significant loss of business to the competitors.

- Raw Material Risk – Key components such as compressors, copper tubes, electronic parts, indoor units for split air conditioners, and inverter drives, are sourced from vendors in China and some other countries. Any disruption in supply caused due to geopolitical reasons, imposition of non-tariff barriers may significantly impact the company’s production.

Other articles you may like

{kind=link}

{kind=link}

{kind=link}