I always wanted to have a quick look at A&O and was finally motivated again reading about it several times in my Twitter timeline. In my All Danish Stocks series, A&O didn’t make the cut because I had already Solar in the portfolio, but still I want to look at them as this often yields some insights into the other company.

Both companies are headquartered in Denmark and in principle distribute supplies for craftsmen/installers.

From what I understand, Solar Group is focused a little more on electrical equipment, A&O has a broader assortment but focused on renovation and remodeling. A&O Johanson has a small B2C segment that makes up ~12% of sales but less in profits, as margins in B2C are smaller.

A&O is active in Denmark, Sweden and Norway, however 90% of sales seem to be in Denmark. A&O has a dual share structure, with “super voting” shares owned by the family and CEO giving copntrol to the family. Also Solar Group has a dual share class structure, with the majority of the votes owned by the heirs of the original founder (4th generation).

Solar is active also in Denmark, Sweden and Norway, but also has a sizeable business in the Netherlands and Poland. Denmark is around ⅓ of sales and 45% of profits for Solar. Apart from craftsmen(installers, 33% of their sales go to industrial clients and a small “trade” segment. Interestingly, the craftsmen/installer segment is the lowest margin segment.

In 2023 they acquired a heat pump business (large pumps for commerce), so they are branching out to a certain extent into manufacturing. That is clearly a risk but SFS for instance shows that a company can do both successfully.

Numbers, numbers, numbers

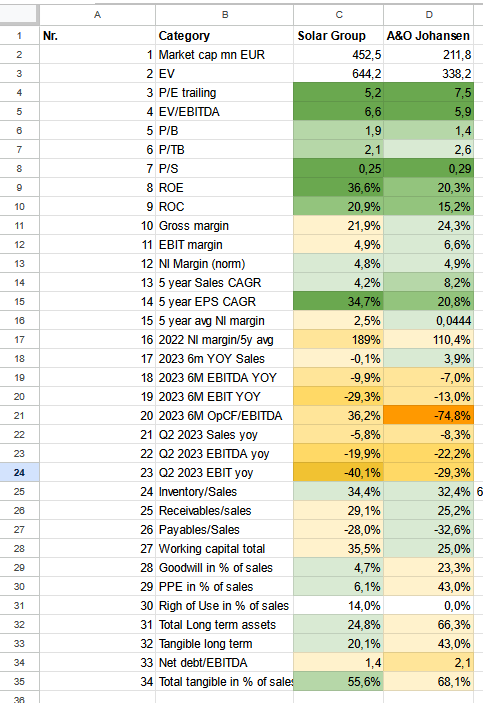

Here are a number of KPIs that I found interesting to compare with some color coding attached:

Both companies look very cheap on 2022 numbers and have decent return on capital which is quite important for distributors.

One thing that stands out is that Solar has been earning much higher margins in recent years than some years before. In my understanding the reason for this is that up to 2017, Solar was basically a turn-around case and they brought in a new CEO to fix things.Going through the annual reports since then, there is a clear effort (and success) in focusing the business and making it gradually more profitable every year.

The main difference between Solar and A&O is that Solar seems to carry more inventory, whereas A&O has a lot more fixed assets. Solar is more capital efficient (even without the goodwill) and therefore lower margins nevertheless translate into higher ROCEs and ROEs despite slightly lower leverage.

Both companies are struggling a little bit this year, interestingly Solar Group more than A&O after depreciation. However, when looking at Cash flow, things look different: Solar has managed to return to positive Operating cashflow whereas A&O had still negative operating CF. I am not sure why and this could turn quickly but it is something to watch.

Solar has been writing off Goodwill quite aggressively in the first 6M, however there is no detailed explanation. A&O doesn’t show amortization separately in the 6M numbers.

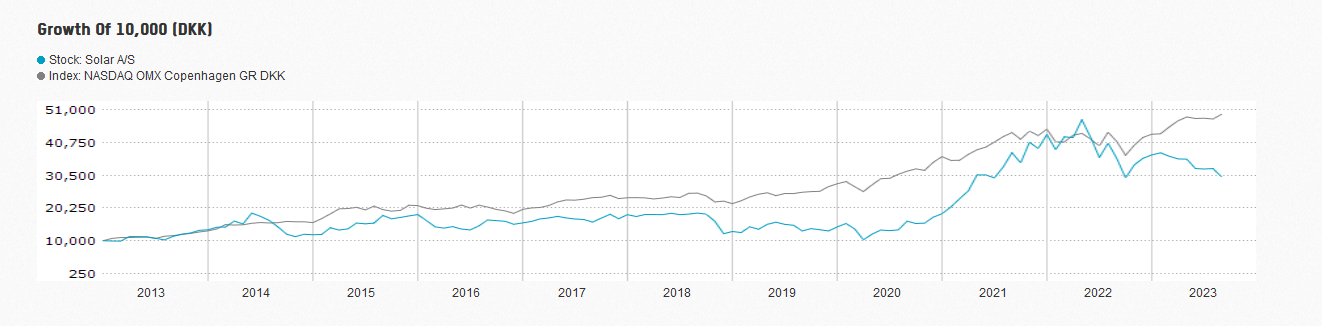

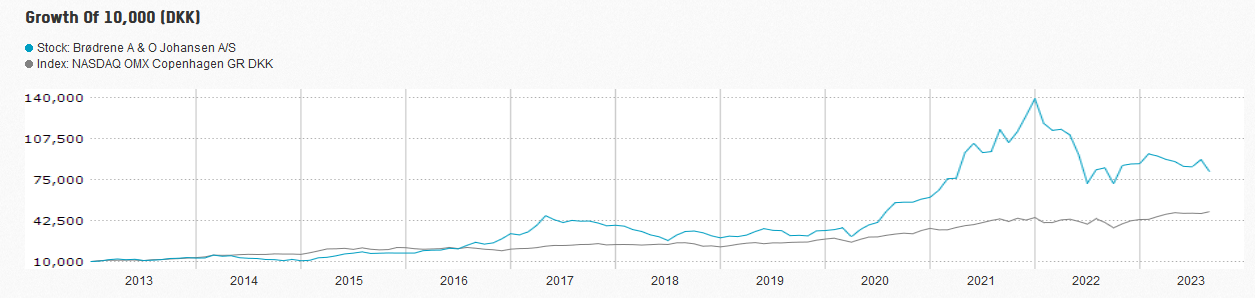

Stock Performance (incl. Dividends):

These are the Total return charts from NAsdaq Nordic, unfortunately I found no way to show them in one chart. Over 10 years, A&O has clearly outperformed Solar.

I guess the main reason is that Solar made a loss in 2014 and no profits both in 2017 and 2019. A&O clearly has the more consistent track record.

Capital allocation wise, both companies seem to prioritize dividends before share buy backs.

Summary:

Overall, I think both are very good companies. A&O has a very good Denmark focused strategy whereas Solar has a more complex business model with different customer groups and jurisdictions. However, this might also allow them to find more growth opportunities.

A&O has a better long term track record, however Solar’s trajectory since the CEO change in 2017 is quite encouraging and the turn-around seems to have been confirmed.

For both companies, investors most likely think that they have massively “over earned” in 2021 and 2022, otherwise the single digit P/Es for these really nice distribution businesses with very good returns on capital make no sense. They will clearly see some headwinds if construction slows down but in my understanding, both companies have limited exposure to new building construction.

I’ll therefore stick with Solar for the time being, but will monitor A&O as well. This seems to be also a cheap but good quality business “under the radar” of many investors and should do both well over the next 3-5 years despite significant short term headwinds.