30 years ago, when financial plans relied mainly on constant investment return projections derived from straight-line appreciation and time-value of money calculations, financial advisors began acknowledging and accounting for the variable and uncertain nature of investment returns. And by turning to tools that incorporated historical or Monte Carlo simulations, advisors were able to examine the potential impact of sequence-of-return risk on an investor’s portfolio, modeling those risks across hundreds or thousands of scenarios into a client’s personal retirement plan and refining the design of realistically sustainable spending strategies for the client. But despite recognizing the impact of investment variability and sequence of return risk on a financial plan, advisors have generally ignored the same historical trends for inflation in their clients’ financial plans. Ironically, while treating investments as uncertain and risky, inflation has generally been modeled as static and risk-free. Which misses the mark with respect to the impact of inflation’s historical variability and potential sequencing risk on consumers and investors.

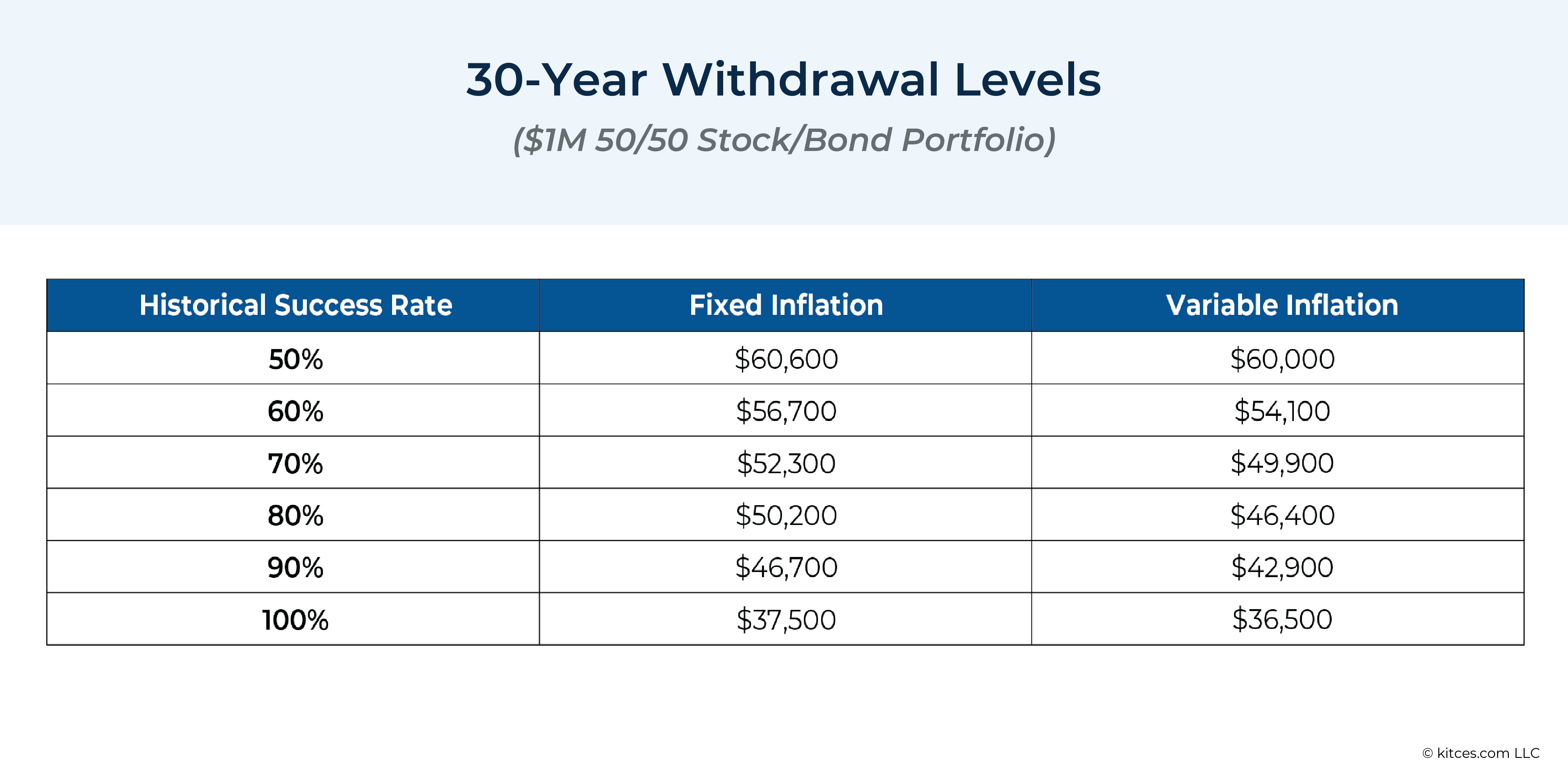

The high variability of inflation over the last several decades – with the high rates of the early 1980s dipping down to the lows in the late 2000s (even in just the last decade, the US has seen both mild deflation in 2015 and inflation of over 9% in 2022) – makes a strong case for treating inflation as uncertain and variable in financial planning. Sequence-of-inflation risk can substantially impact a financial plan and failing to consider this risk can lead advisors to overestimate sustainable spending and underestimate risk in retirement. Though most plans are affected at least somewhat by inflation risk, certain factors make accounting for it especially important. If inflation is expected to be high or especially variable or uncertain, or a plan has substantial not-adjusted-for-inflation cash flows (as found in many pensions), a higher bond allocation, or a higher probability of success (>70%), failing to consider the variability of inflation and sequence-of-inflation risk will likely distort plan results and make them less dependable. In these situations, modeling variable inflation can help reveal risk that isn’t otherwise apparent when inflation is kept constant. By exploring high-inflation, low-inflation, and mixed-inflation scenarios, advisors have the flexibility of customizing advice that can more holistically balance a client’s spending goals with their risk tolerance.

Ultimately, the key point is that inflation is far from a static factor and is just as variable and uncertain as the other key aspects of the plan. And when its variability is not accounted for, the quality and resilience of the advice in a client’s financial plan can suffer, especially for those with lower portfolio returns and higher probability-of-success expectations. But by treating inflation realistically, accounting for its variability, and acknowledging the sequence-of-inflation risk that clients are faced with, advisors can leverage multiple scenarios to create a robust plan and ensure they are offering the best recommendations for their clients!

{kind=link}