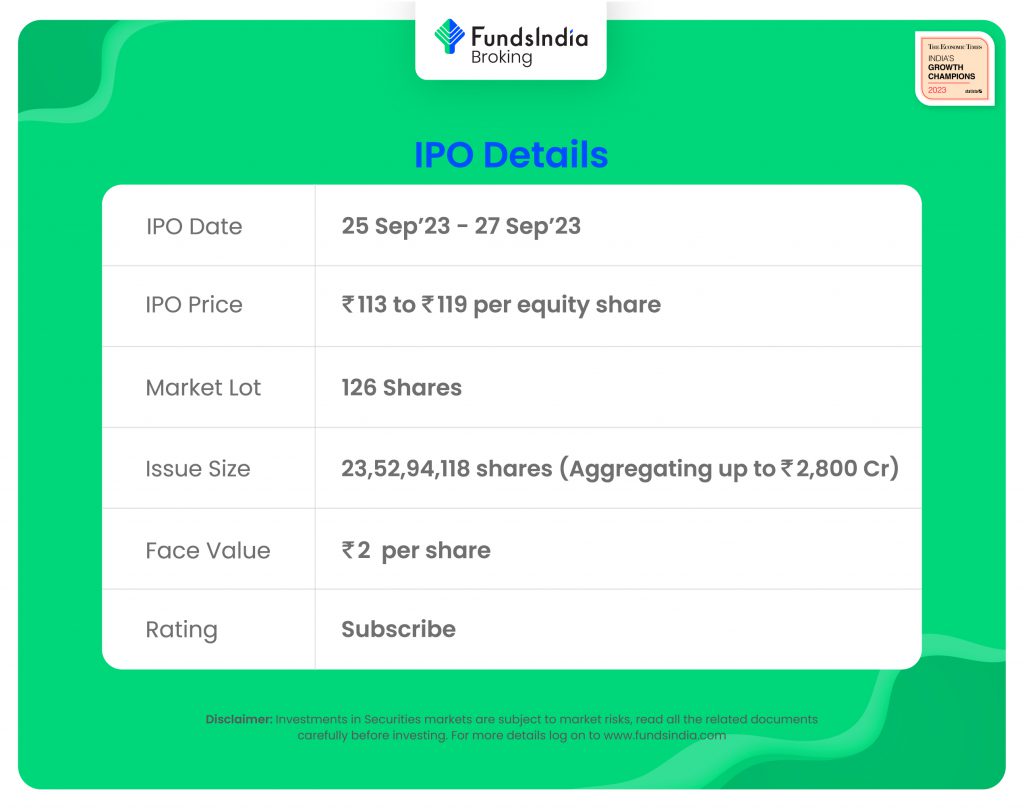

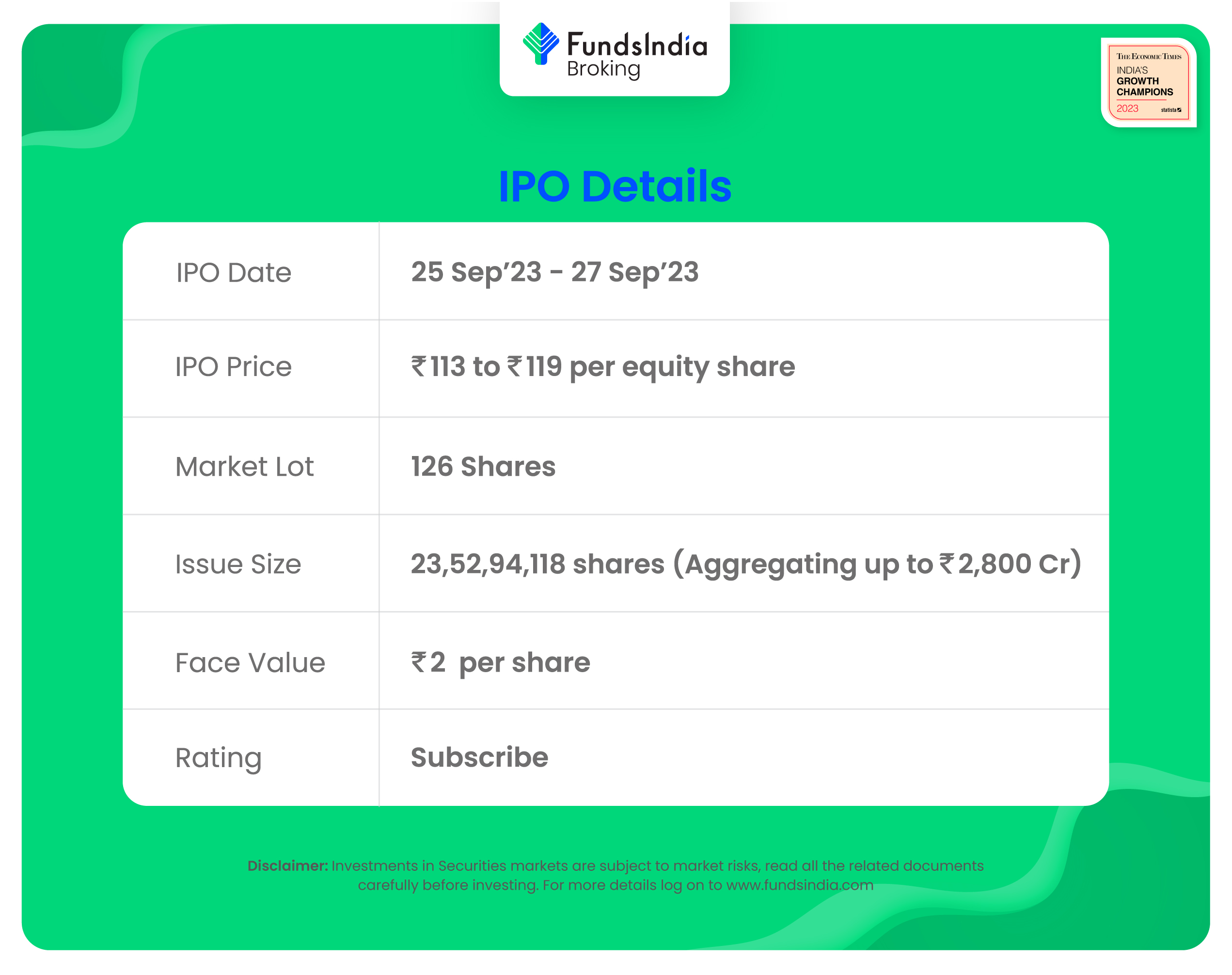

Company Overview:

JSW Infrastructure Ltd (JSWIL), incorporated in the year 2006, is a part of the JSW group and is engaged in the business of developing infrastructure and operations for ports across India. They are the fastest growing port-related infrastructure company in terms of growth in installed cargo handling capacity and cargo volumes handled during Fiscal 2021 to Fiscal 2023, and the second largest commercial port operator in India in terms of cargo handling capacity in Fiscal 2023. The company’s operations have expanded from one Port Concession at Mormugao, Goa that was acquired by the JSW Group in 2002 and commenced operations in 2004, to nine Port Concessions as of June 30, 2023 across India, making them a diversified maritime ports company. They provide maritime related services including, cargo handling, storage solutions, logistics services and other value-added services to their customers, and are evolving into an end-to-end logistics solutions provider.

Objects of the Offer:

- Prepayment or repayment, in full or part, of all or a portion of certain outstanding borrowings through investment in their wholly owned Subsidiaries, JSW Dharamtar Port Private Limited and JSW Jaigarh Port Limited.

- Financing capital expenditure requirements through investment in their wholly owned Subsidiary, JSW Jaigarh Port Limited, for proposed expansion/upgradation works at Jaigarh Port i.e., i) expansion of LPG terminal (“LPG Terminal Project”); ii) setting up an electric sub-station; and iii) purchase and installation of dredger.

- Financing capital expenditure requirements through investment in their wholly owned Subsidiary, JSW Mangalore Container Terminal Private Limited, for proposed expansion at Mangalore Container Terminal (“Mangalore Container Project”).

- General corporate purposes.

Investment Rationale:

- Fast Growing Company: JSW Infra is the fastest growing port-related infrastructure company in terms of growth in installed cargo handling capacity and cargo volumes handled from Fiscal 2021 to Fiscal 2023. Their installed cargo handling capacity in India grew at a CAGR of 15.27% between March 31, 2021 and March 31, 2023, and the volume of cargo handled in India also grew at a CAGR of 42.76% from Fiscal 2021 to Fiscal 2023. Further, the company’s 190 installed cargo handling capacity in India grew from 153.43 MTPA as of June 30, 2022 to 158.43 MTPA as of June 30, 2023, and the volume of cargo handled by the company in India grew from 23.33 MMT for the three-month period ended June 30, 2022 to 25.42 MMT for the three-month period ended June 30, 2023.

- Diversified Presence: The company has a diversified presence across India with Non-Major Ports located in Maharashtra and port terminals located at Major Ports across the industrial regions of Goa and Karnataka on the west coast, and Odisha and Tamil Nadu on the east coast. The Port Concessions are strategically located in close proximity to the JSW Group Customers (Related Parties) and are well connected to cargo origination and consumption points. This enables the company to serve the industrial hinterlands of Maharashtra, Goa, Karnataka, Tamil Nadu, Andhra Pradesh and Telangana, and mineral rich belts of Chhattisgarh, Jharkhand and Odisha (Source: CRISIL Report), making their ports a preferred option for customers. In addition, they benefit from strong evacuation infrastructure at their ports and port terminals that comprises of multi-modal evacuation techniques, such as coastal movement through a dedicated fleet of mini-bulk carriers, rail, road network and conveyor systems.

- Financial Track Record: The company reported a revenue of Rs.3195 crore in FY23 as against Rs.2273 crore in FY22, an increase of 41% YoY. The revenue has grown at a CAGR of 26% between FY18-23. The EBITDA of the company in FY23 is at Rs.1623 crore and the PAT is at Rs.750 crore for the same period. The PAT has grown at a CAGR of 23% between FY18-23. The EBITDA margin and PAT margin of the company in FY23 is around 51% and 23% respectively. The ROE and ROCE of the company stands at 18% and 19% in FY23, respectively.

Key Risks:

- Dependency Risk – Business heavily depends on concession and license agreements with government and quasi-governmental bodies. Breaching these agreements could lead to termination, causing significant harm to business, financial condition, and cash flow.

- Capital Intensive Business – The nature of port operator’s industry demands significant capital for expansion and development projects, and any inability to raise necessary funds in the future may affect the business growth.

Outlook:

JSW Infrastructure is the first IPO from the JSW Group in nearly 13 years. This makes it a highly anticipated event for investors, as the JSW Group is one of the largest and most successful conglomerates in India. According to RHP, Adani Ports and SEZ Ltd is the only listed competitor for JSW Infra. Adani Ports is trading at a P/E of 34x based on FY23 EPS. At the higher price band, the listing market cap of JSW Infra will be around ~Rs.24,990 crore and it is demanding a P/E multiple of 33x based on post issue diluted FY23 EPS of Rs.3.57. When compared with its peers, the issue seems to be reasonably priced in (fairly valued). Based on the above views, we provide a ‘Subscribe’ rating for this IPO for a medium to long-term Holding.

If you are new to FundsIndia, open your FREE investment account with us and enjoy lifelong research-backed investment guidance.

Other articles you may like

{kind=link}

{kind=link}

{kind=link}