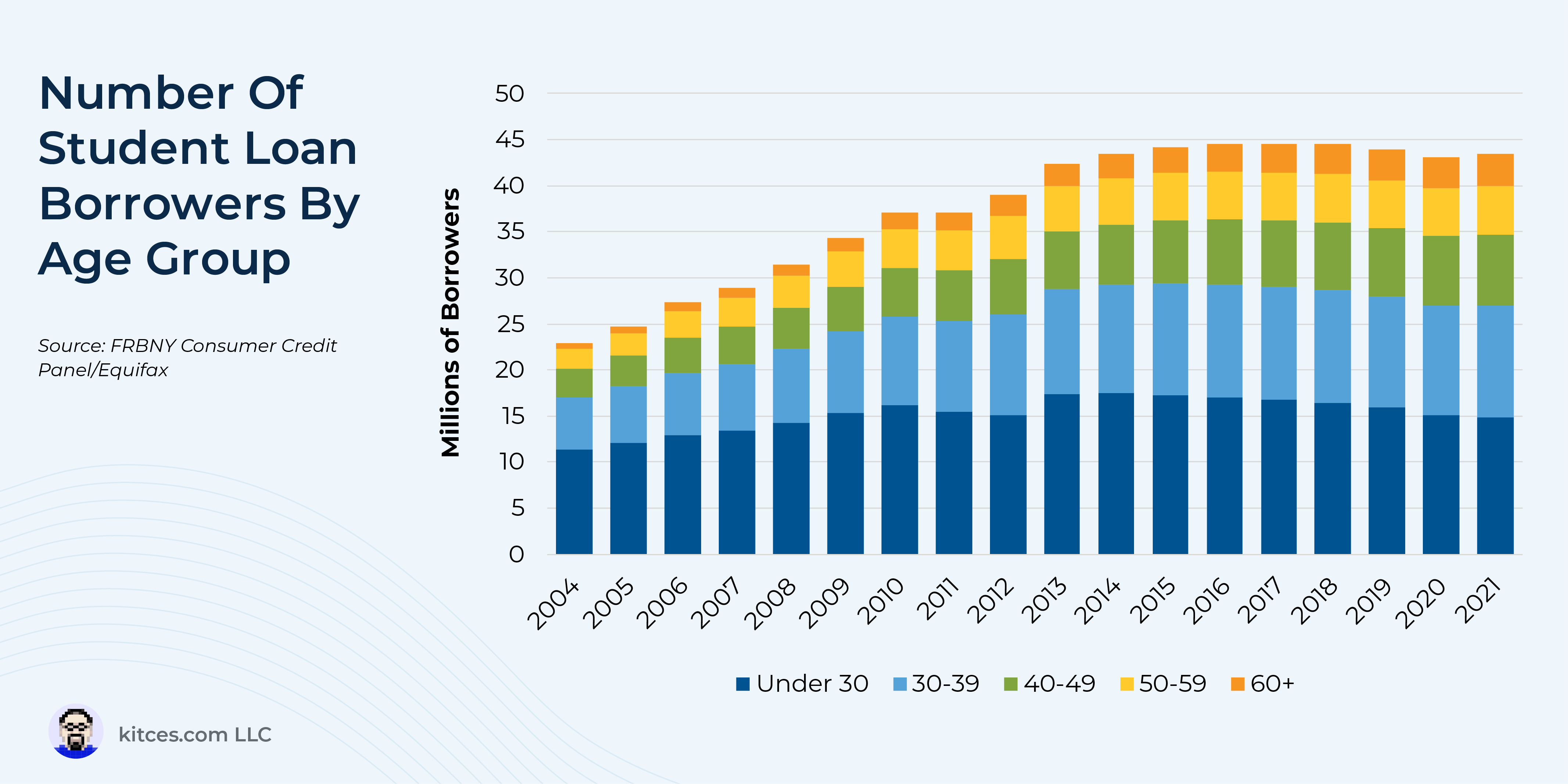

When it comes to advising clients on student loan issues, many financial advisors might first think about recent graduates seeking advice regarding the most effective way to pay down their balances. However, the number of Federal student loan borrowers over the age of 50 has increased significantly in the past 20 years, with many of these borrowers holding Parent PLUS loans that were used to help fund their children’s undergraduate education.

While student borrowers of Federal Direct loans are eligible for a range of Income-Driven Repayment (IDR) plans – including the newly introduced Saving on a Valuable Education [SAVE] plan – that can reduce required monthly payments significantly compared to the standard repayment option (depending on the borrower’s income), available IDR plans for those with Parent PLUS loans are much more limited, often resulting in substantially larger monthly loan payments. Which not only cuts into a parent’s current cash flow, but also limits their ability to save for their (potentially fast-approaching) retirement.

Nonetheless, Parent PLUS borrowers (and their advisors) have an opportunity (until July 1, 2025) to access more generous IDR plans by using a “Double Consolidation” loan strategy. With this option, a parent borrower first consolidates their existing Parent PLUS loans into 2 Direct Consolidation loans, and then consolidates these 2 Direct Consolidation loans into a single new Direct Consolidation loan. The resulting loan would be eligible for more favorable IDR plans, including the SAVE plan, otherwise unavailable for those with Parent PLUS loans. Importantly, while this process might seem relatively straightforward on the surface, the multi-step process must be completed accurately and completely to ensure that the resulting Direct Consolidation loan is eligible for preferential IDR options.

Notably, given the looming July 2025 deadline and the importance of completing the Double Consolidation process (which can involve many paper forms and take 3–6 months in total) accurately and in a timely manner, advisors can play an important role in guiding clients with Parent PLUS loans through each step of the process. Further, advisors can help clients who complete the process choose the best IDR option for their situation and take steps to minimize required payments, from deciding whether to elect to file taxes separately (for married couples) to finding ways to reduce the borrower’s Adjusted Gross Income.

Ultimately, the key point is that as more individuals 50 and older hold student loans, financial advisors may find that an increasing number of clients are facing the challenge of paying down loans taken out for their children’s education expenses while also trying to save for their own retirement. And for those clients who currently have Parent PLUS loans (or who are planning to have such loans and who can complete the consolidation process before July 2025), advisors can add significant value by supporting them through the complex process of Double Consolidation, which could be an effective way to help them save on their children’s education and, at the same time, to free up more of their wealth to pursue more of their other important financial goals!

{kind=link}