Today, Jerome Powell is making the opening remarks at the 24th Jacques Polak Annual Research Conference in DC. I’ll be on Bloomberg Radio today 3:00 pm-6:00 pm, and it’s the first topic we will address.

I wanted to gather a few thoughts and recent discussions together in preparation for that. These are what is driving my thoughts on Jerome Powell & Co and the risks future FOMC action present.

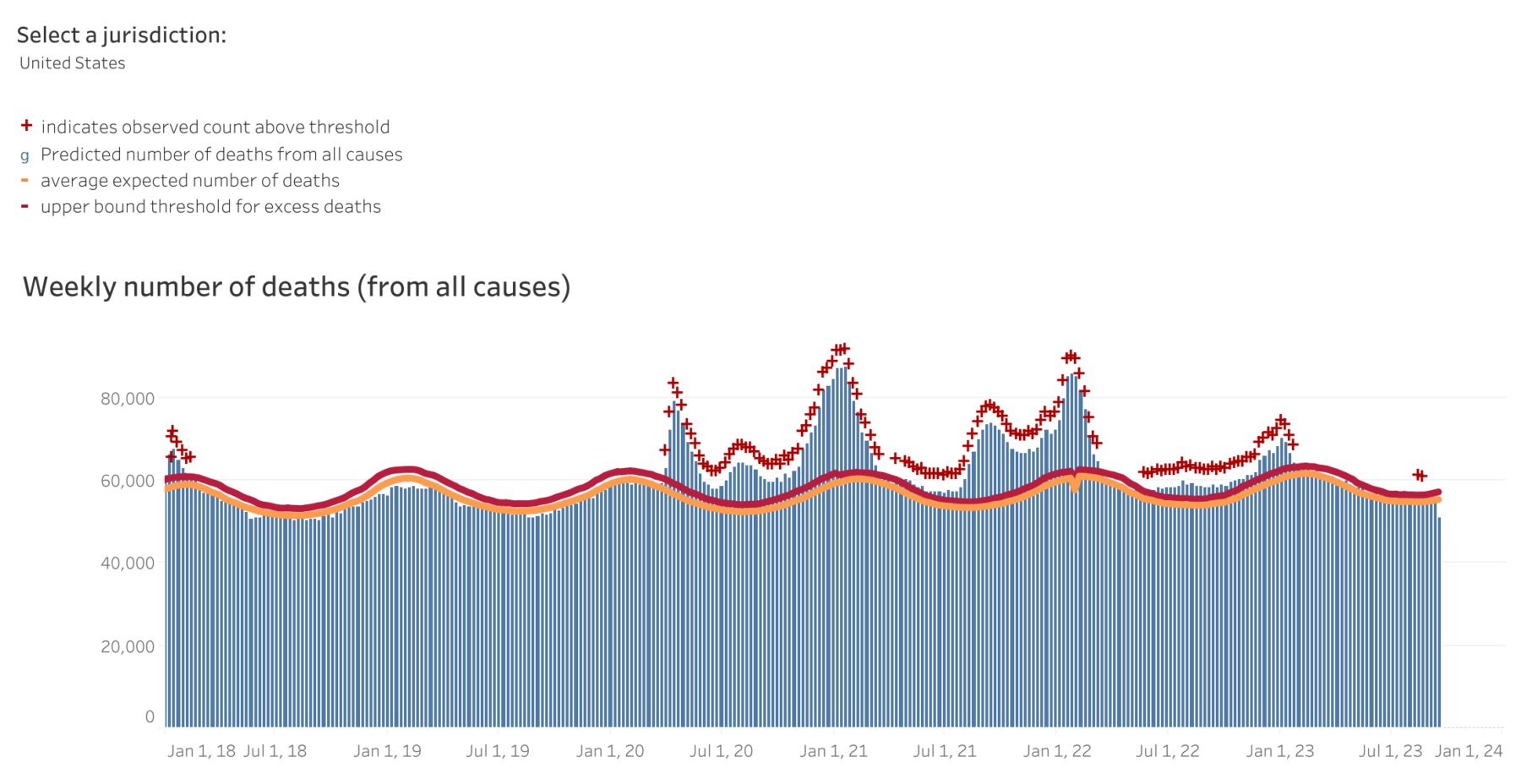

1. The post-lockdown economy is returning to normal.

The chart up top shows the impact of Covid-19 on excess deaths in America. Squint and you can see the economic impact of the early surge of deaths in 2020, which slowed during lockdowns (and summer); the 2nd wave in the Fall of 2020 into Winter; the 3rd surge in the Summer of 2020 (Omicron variant) which ebbed then peaked in January 2022; then the Fall/Winter surge in 2022-23.

Then we re-opened in earnest.

The inflation surge really began in the Spring of 2021: Everyone came out of their lockdowns, armed with CARES Act cash in their bank accounts, bored out of their minds and ready to party. First, it was Goods from Cars to Houses to anything else they could buy; then, it was Services, including entertainment and (especially) travel.

But supply chains unraveled and people got vaxxed & boosted. Eventually, after all the pent-up demand caused by 18 months of cabin fever broke, things began to normalize. We are mostly there, but some issues still remain.

2. Shortages remain a big source of persistent inflation.

We wildly underbuilt single-family homes for about 15 years; Semiconductors are still not available in quantities needed to hit pre-pandemic levels of new car sales of 16-17 million annually; There is a huge shortage of laborers as people have upskilled and moved on to better gigs. As evidenced by the successful strike resolutions in labor’s favor, the balance of power has shifted ion the labor markets.

I do not see how higher rates in general or higher for longer will solve these problems.

3. The Fed is done raising rates.

It was obvious to me the Fed was done (or should have been) raising rates in May. I insisted they were done before the most recent meeting (November 1st). There are many reasons for this, but the most =important ones are:

a) They are making housing much worse;

b) Rates came down despite — not because — of the Fed;

c) Inflation peaked last June and has continued to subside since.

The chart above explains much of what happened.

4. The Fed’s models are old and broken.

I don’t have a problem with using econometric models — the issue is that all models are limited, incomplete, and often erroneous depictions of reality. You forget that at great peril.

I was aghast to hear Minneapolis Fed president Neel Kashkari say “It’s not that our models are wrong, it’s the dark matter.” This reflects a failure to understand the limitations of models in general and the issues with your own models specifically. It seems that I must continuously go to George E. P. Box‘s quote “All models are wrong, but some are useful.”

Who are you gonna believe, your models or your own lying eyes?

~~~

The risk today is that the FOMC will tip us into an unnecessary recession, and send the unemployment rate over 5%.1 There are few things more frustrating than self-inflicted, avoidable errors.

Previously:

The Fed is Finished* (November 1, 2023)

Inflation Comes Down Despite the Fed (January 12, 2023)

For Lower Inflation, Stop Raising Rates (January 18, 2023)

Why Aren’t There Enough Workers? (December 9, 2022)

How the Fed Causes (Model) Inflation (October 25, 2022)

How Everybody Miscalculated Housing Demand (July 29, 2021)

Who Is to Blame for Inflation, 1-15 (June 28, 2022)

__________

1. It could also give us a second term of President Trump, assuming Chris Christie is wrong and he stays out of jail. But it’s not too difficult to see either outcome…

{kind=link}