The latest PPF, SCSS and Post Office Term Deposit Amendment Rules 2023 were introduced on 7th November 2023. Few rules are investor-friendly and few are harsh.

The government notified these changes on 7th November 2023. As I mentioned above, few rules with respect to PPF and SCSS look investor-friendly. However, the new rules with respect to a 5-year term deposit look too harsh. Let us see all these changes in detail.

PPF, SCSS and Post Office Term Deposit Amendment Rules 2023

1) PPF or Public Provident Fund (Amendment) Scheme, 2023

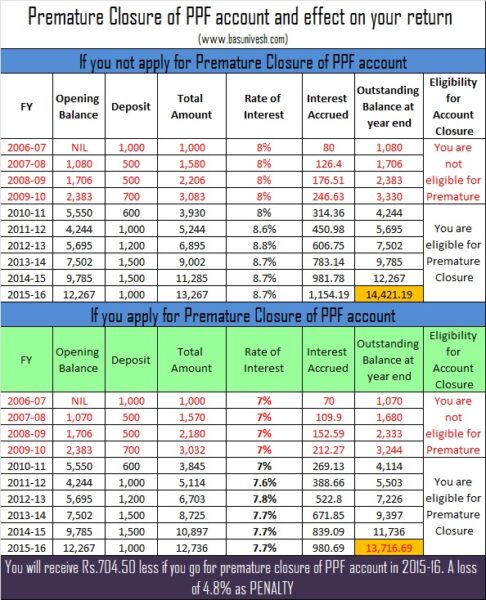

Let me explain to you at first the existing rules of PPF premature withdrawal rules (I wrote an article on this “Premature Closure Of PPF Account – New Rules 2016“).

You are allowed for premature closure of your account or for the account where you are a guardian for minors or a person of unsound mind by submitting Form-5. You are allowed for premature closure only for the below reasons.

(a) Treatment for a life-threatening disease of the account holder, his spouse or dependent children or parents, on the production of supporting documents and medical reports confirming such disease from the treating medical authority.

(b) Higher education of the account holder, or dependent children on the production of documents and fee bills in confirmation of admission in a recognized institute of higher education in India or abroad.

(c) If your residential status changes, then you are allowed for premature closure on the production of the copy of your Passport and visa or Income-tax return.

Along with that, please note the below points to understand more about the premature close of PPF account rules.

# You are allowed to close the account before maturity if the account is completed 5 years from the end of the year in which the account was opened. This rule is not applicable to the death of the account holder.

# Regarding the amount required for the treatment of serious ailments or life-threatening diseases, you must produce supporting documents from the competent medical authority.

# Regarding the amount required for higher education, you must produce the documents of fee bills in confirmation of admission in a recognized institute of higher education in India or ABROAD.

The old rules can be tabulated with the below example.

What has changed NOW?

The earlier sentence was “Provided further that on such premature closure, interest in the account shall be allowed at a rate which shall be lower by one percent. than the rate at which interest has been credited in the account from time to time since the date of opening of the account, or the date of extension of the account, as the case may be“.

The new sentence will be “Provided further that on such premature closure, interest in the account shall be allowed at a rate which shall be lower by one percent. than the rate at which interest has been credited in the account from time to time since the date of opening of the account, or from the date of commencement of the current block period of five years“.

It means earlier let us assume that your account is around 17 years old, and if you wish to close the account, then you will receive 1% less interest on whatever the interest credited for the whole 17 years. However, due to the new rule, there will not be any 1% deduction for the 15-year period. The interest credited on the 16th and 17th year will only be less than 1%.

Same way let us assume that your account is around 24 years old, and if you wish to close the account, then you will receive 1% less interest on whatever the interest credit is for the period of the 21st year to the 24th year. There will not be any change in interest for whatever you earned up to 20 years (15 years regular term and 5 years 1st extension).

The penalty of 1% less interest will be applicable for the current block only. The earlier interest accumulated either from the 15 years or from the earlier block of 5 years will not be impacted.

This seems to be a BIG relief for those whose PPF account completed more than 15 years. However, this new change will not impact to those whose account is less than 15 years old.

2) Senior Citizen’s Savings (Fourth Amendment) Scheme, 2023

In terms of SCSS, there are few changes in rules introduced and I will share the same one by one.

a) You can extend SCSS as long as you WISH!!

Earlier the extension for SCSS was allowed only once. Now you can extend the SCSS after the completion of 5 years as many times as you wish for in the block of 3 years. This is really a good move for senior citizens.

b) Penalty and liquidity for premature withdrawal during extended SCSS

Earlier during the extended SCSS period, you are allowed to withdraw the amount after one year without any penalty. However, now you are allowed to withdraw before one year. But you have to pay a 1% penalty on the deposited amount.

This means liquidity is provided in the 6th year which was not there earlier but comes with a 1% penalty.

c) Relaxation to open the account for those whose age is 55 years to 60 years and who received retirement benefits

The earlier rule of eligibility to open SCSS was as below.

# An individual who attained the age of 60 years of age or above on the date of account opening.

# An individual who attained the age of 55 years or more but less than 60 years of age and has retired on superannuation or under a voluntary or special voluntary scheme. But they can open this account only on the condition that the account is opened within one month of receipt of retirement benefits and the amount should not exceed the amount of retirement benefit.

# Retired personnel of Defence Services (excluding civilian Defence employees) on attaining the age of fifty years subject to the fulfillment of other specified conditions.

# NRIs and HUF are not eligible to open this account.

What has changed NOW?

Below are the changes.

# An individual who attained the age of 55 years or more but less than 60 years of age and has retired on superannuation or under a voluntary or special voluntary scheme. But they can open this account only on the condition that the account is opened within THREE MONTHS of receipt of retirement benefits and the amount should not exceed the amount of retirement benefit.

Earlier the time limit was one month to open but not it is increased to three months. More flexibility for senior citizens.

b) The spouse of a Government employee can open the SCSS account

The earlier rule was as below.

“The successor or legal heir of a deceased serving personnel shall not be eligible to deposit the terminal

benefits of such deceased personnel under this Scheme.”

The current rule is as below.

“The spouse of the government employee shall be allowed to open an account under this Scheme, if the government employee who has attained the age of fifty years and has died in harness, subject to the fulfillment of other specified conditions.”

It means if a government employee dies while working and is 50 years and above, then his spouse is allowed to open the account.

Because of this, the definition of retirement benefits has also changed. The earlier definition was ” “retirement benefits” means any payment due to the account holder on account of retirement on superannuation or otherwise and includes Provident Fund dues, retirement or superannuation gratuity, commuted value of pension, cash equivalent of leave, savings element of Group Savings Linked Insurance Scheme payable by the employer on retirement, retirement-cum withdrawal benefit under the Employees’ Family Pension Scheme and ex-gratia payments under a voluntary or a special voluntary retirement scheme.”.

The new definition of retirement benefit is “retirement benefits” means any payment due to the account holder on account of retirement on superannuation or otherwise and includes Provident Fund dues, retirement or superannuation or death gratuity, commuted value of pension, cash equivalent of leave, savings element of Group Savings Linked Insurance Scheme payable by the employer on retirement, retirement-cum-withdrawal benefit under the Employees’ Family Pension Scheme and ex-gratia payments under a voluntary or a special voluntary retirement scheme and in case, if the employee died in harness, the “retirement benefits” shall also mean the above-mentioned benefits to employee who died in harness.”

c) Default continuation not allowed in joint account SCSS

The earlier rule was “Provided further that in case of a joint account, or where the spouse is the sole nominee, the spouse may continue the account on the same terms and conditions as specified under this Scheme if the spouse meets eligibility conditions under the Scheme on the date of death of the account holder.”

The new rule is “Provided further that in case of a joint account, or where the spouse is the sole nominee, the spouse may continue the account by applying to the accounts office, on the same terms and conditions as specified under this Scheme, if the spouse meets eligibility conditions under the Scheme on the date of death of the account holder”.

It means the surviving spouse has to apply for the continuation of the account without which I think it is not acceptable.

3) National Savings Time Deposit (Fourth Amendment) Scheme, 2023

Under this, the new rules are introduced strictly towards the 5 year term deposit liquidity. I think it is too harsh.

a) 5 years term deposit liquidity curtailed

The earlier rule was “where a deposit in a one-year, two-year, three-year or five-year account is withdrawn prematurely after six months, but before the expiry of one year from the date of deposit, interest shall be payable to the account holder at the rate applicable to Post Office Savings Account for the completed months;”

The rule is “where a deposit in a one-year, two-year or three-year account is withdrawn prematurely after six months, but before the expiry of one year from the date of deposit, interest shall be payable to the account holder at the rate applicable to Post Office Savings Account for the completed months;”.

Hence, it is now clear that a 5-year term deposit can’t be liquidated after six months but before the expiry of a year. Even a 5-year deposit withdrawal condition after one year is also removed.

According to a new rule, the liquidity for a 5-year deposit is allowed only after 4 years of completion. But again the rules are stricter now with huge penalties. Earlier if you close the deposit after 4th year, then you are allowed to earn the interest rate applicable for 3 years term deposit. However, now you will earn the interest rate applicable to the Post Office Savings Account.

{kind=link}