Although numerous tax-advantaged vehicles are available for retirement savings, Health Savings Accounts (HSAs) have particular benefits for individuals saving for retirement. Specifically, HSAs offer a “Triple Tax Benefit” that includes tax-deductible contributions, tax-deferred growth, and tax-free withdrawals for qualified medical expenses. This can allow individuals to save a significant amount that can be withdrawn tax-free for medical expenses later in retirement. Therefore, for workers looking to boost their savings towards the end of their working years, HSA contributions can be the most tax-efficient vehicle available.

The caveat, however, is that to be eligible to contribute to an HSA, an individual must be covered by a qualifying High-Deductible Health Plan (HDHP) with no other non-HDHP coverage. And because government-funded health insurance options such as Medicare are not considered qualifying HDHP coverage, enrolling in Medicare – either directly through its website or by applying for Social Security benefits (which automatically enrolls someone in Medicare once they reach age 65) – means that an individual will no longer be eligible to contribute to an HSA.

For retirees, self-employed workers, and others who rely on Medicare as their sole option for health insurance after reaching age 65, this means there is effectively no way to contribute to an HSA after age 65. However, people who continue working beyond age 65 (or whose spouse does so) and have access to an employer-provided HDHP can continue making HSA contributions as long as they don’t enroll in Medicare or apply for Social Security benefits. And because there’s no age cap on HSA contributions, it’s possible to keep contributing for as long as the person is still working and remains on a qualifying HDHP (although retiring and subsequently enrolling in Medicare will ultimately end HSA eligibility).

Advisors can help their clients who want to keep contributing to HSAs after age 65 by planning strategies that help to preserve their eligibility and maximize the amount they can contribute. For instance, if someone has applied for Social Security benefits and inadvertently enrolled in Medicare (which would make them ineligible for HSA contributions), they may be able to withdraw their Social Security application within 12 months and cancel their Medicare coverage to restore their eligibility – although doing so would require paying back any Social Security benefits actually received.

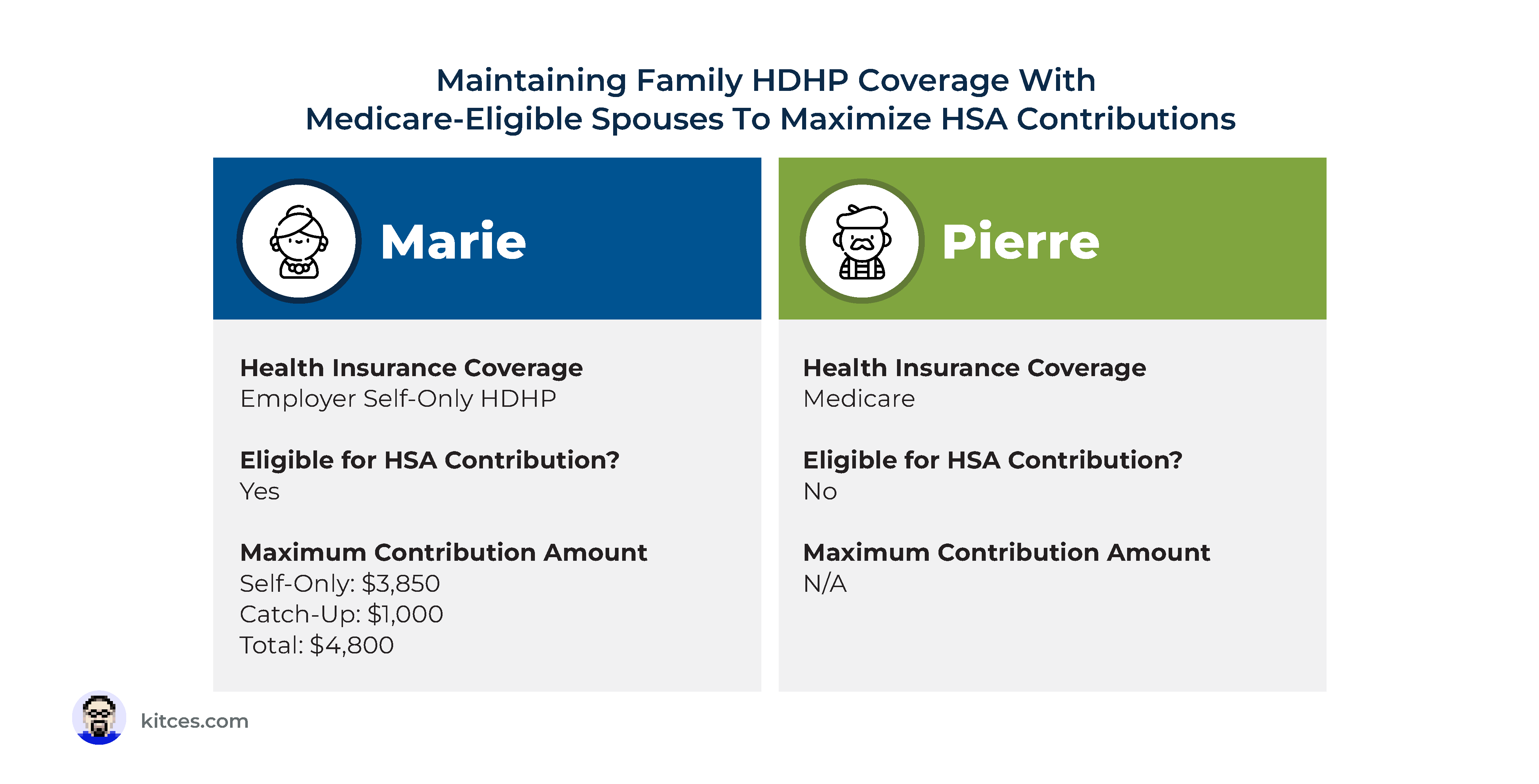

Additionally, when married couples have one spouse with HDHP coverage, the other spouse can enroll in Medicare without affecting the HDHP-covered spouse’s HSA eligibility (and if the HDHP covers both spouses, one spouse can still contribute up to the higher family contribution limit even if the other spouse is covered by Medicare and ineligible to contribute to their own HSA).

And when someone working past age 65 does decide to retire, they will need to navigate the “6-month rule”, where Medicare coverage is considered to begin 6 months before applying for benefits. This means the individual will need to plan carefully to calculate their maximum allowed HSA contribution to avoid inadvertently overcontributing to their HSA, since they may become ineligible for contributions well before they actually retire and apply for Medicare!

The key point is that while it’s possible to contribute to an HSA after age 65, the specific rules around HSAs and Medicare introduce an additional layer of planning that’s needed once an individual crosses the age-65 threshold. But given that the point of working past 65 is often to boost retirement savings, and given the tax-efficient benefits of HSAs as a retirement savings vehicle, the extra planning can ultimately be worthwhile on account of the additional tax-free savings for those who can navigate the challenges of doing so!

{kind=link}