When an investor is seeking to work with a financial professional, there’s a substantial difference in expectations about the nature of the relationship when the professional being consulted is an advisor versus when they’re a salesperson. In hiring an advisor, the investor is presumably seeking to put their trust and confidence in someone with their best interests in mind who can advise them on a course of action. Whereas in a sales transaction, the investor is most likely aware that a salesperson’s job is simply to sell a product, which puts the onus on the investor (rather than the professional) to evaluate the salesperson’s pitch and decide whether or not to act on it.

The difference between an advice and sales relationship isn’t necessarily problematic on its own, since some people truly do just want to buy a product from a salesperson, rather than go through the time and cost it takes to be thoroughly advised on the best strategy. However, if an investor is unable to recognize whether they’re engaged with an advisor (where they would expect the advice is truly in their best interest) and when they’re engaged with a salesperson (specifically intended to sell products), they may be persuaded to take actions that are not truly in their best interests.

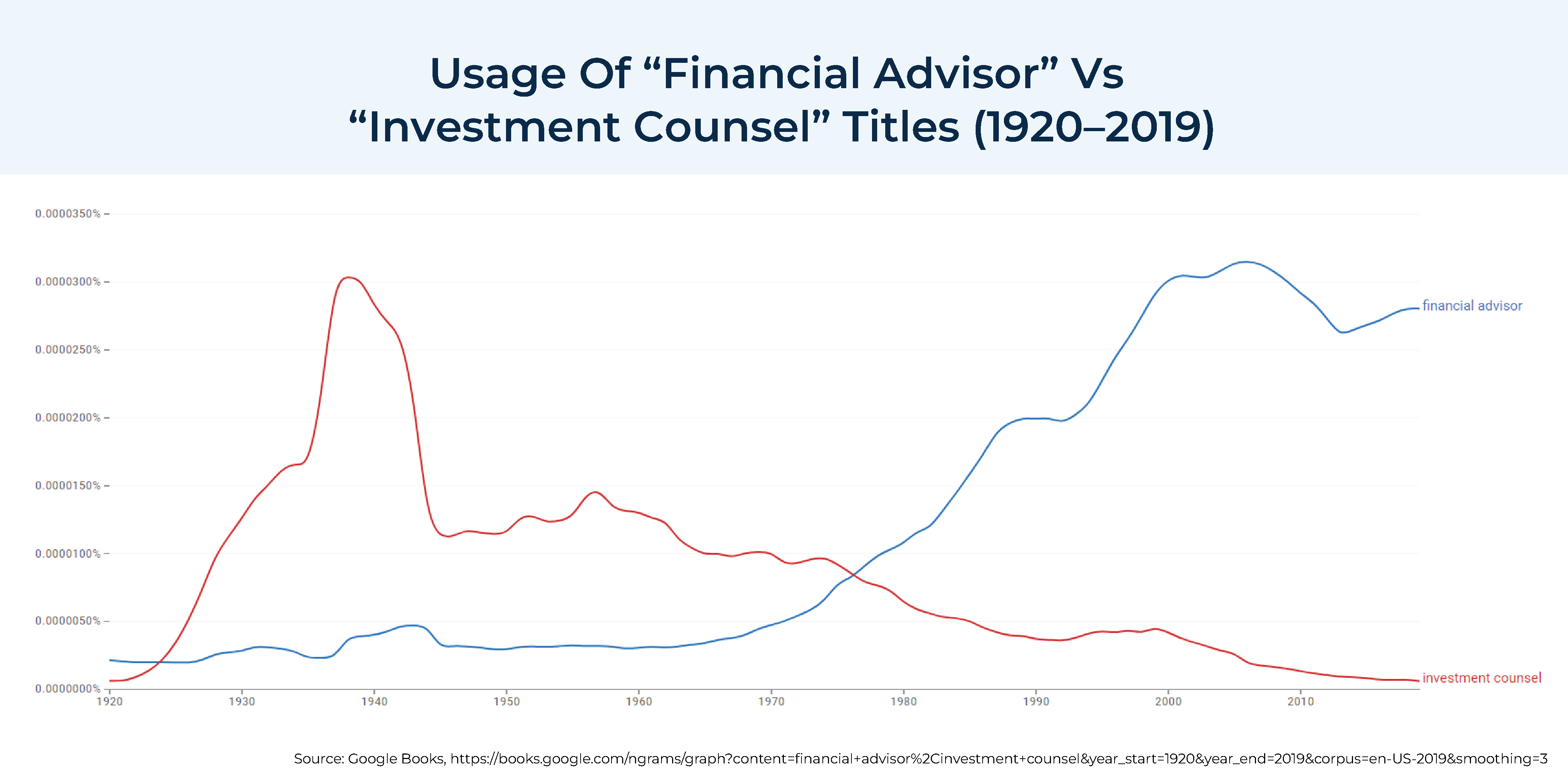

As a result of this dynamic, there is a long regulatory history of separating sales and advice, going all the way back to the Investment Advisers Act of 1940, which strictly limited the use of the then-popular “investment counsel” title to be used only by those who were actually in the business of giving investment advice, and forbidding its use by those primarily providing brokerage services. However, by the 1970s, the “investment counsel” term had largely fallen out of use in favor of the more generic (and less regulated) “financial advisor”, which grew in popularity as insurance and mutual fund salespeople began to co-opt the title and position themselves as “advisors” while still being both compensated and regulated as salespeople. To this day, slews of professionals from the investment, brokerage, and insurance industries still use the “financial advisor” title without being registered as being in the business of giving investment advice – leaving many investors who hire them confused about how their “advisor” might not actually be an advisor expected to give them advice in their best interests.

Against this backdrop, the U.S. Department of Labor (DoL) has released a new proposed Retirement Security Rule that aims to apply new fiduciary standards to professionals who give investment advice to retirement investors when a relationship of trust and confidence exists between the advisor and the client, which would encompass both registered investment advisers, and insurance agents and brokerage representatives offering advice recommendations as well. But while DoL’s proposed rule applies to professionals based on the functions they engage in (e.g., the level of personalization/customization of the advice recommendations), it has also expressed interest (via a Request for Comment on its proposed rule) in how a retirement advice provider’s title may or may not create an expectation of trust and confidence. For example, if a professional holds themselves out as a “financial advisor”, a prospective retiree who hires them may presume that the professional will provide advice – recommendations that are in their best interest – even if that professional isn’t actually obligated to do so.

Arguably, though, the DoL still misses the true significance of the role that advisor titles play. As ultimately, there may be no actual functional difference between the type of questions and the specificity of recommendations made by advisors versus salespeople; instead, the difference between sales and advice is driven by the consumer’s expectation of whether they’re working with someone in an advice or sales capacity in the first place. Which is first and foremost defined by the way the financial professional titles themselves and markets their services.

As a result, one of the most straightforward ways to re-assert a clearer line for consumers between advice and sales is simply for the DoL to permit insurance agents and brokerage representatives to continue to be salespeople… so long as the professional does not hold themselves out as being a financial advisor or market that they offer financial planning.

Such a “Salesperson’s Exemption”, which would allow insurance and brokerage salespeople to avoid the DoL’s fiduciary obligation in the Retirement Security Rule, would apply to salespersons who (1) avoided holding themselves out as financial advisors or financial planners, (2) avoided marketing that they offer any financial advice or financial planning services, (3) and provided disclosures on all sales presentations or illustrations to the effect that the engagement does not constitute advice and that the consumer should consult an actual financial advisor about the appropriateness of the sales recommendation.

The benefit of such an approach is that it would allow insurance companies and brokerage firms to continue acting in a purely sales function, without meeting the additional regulatory burdens of being a fiduciary advisor. Which would also help the DoL defend against the court challenges it faced with its last fiduciary rule – struck down when the courts agreed that the fiduciary standard should only apply to advisors, and not to salespeople who are not in a “relationship of trust and confidence” with their clients. All of which helps to preserve the regulatory distinction between sales and advice, and also continues to allow retirement investors the opportunity to choose between sales and advice (according to their own needs).

The key point is that even though regulatory bodies have recognized the distinct nature of advice relationships of trust and confidence and applied higher standards of care for such advice relationships in the past, the line between sales and advice has blurred in more recent years. The DoL could help clarify the distinction with a more “truth-in-advertising” approach, by requiring those who market themselves as advisors acting in a position of trust and confidence to retirement investors to be accountable to the fiduciary standards that go along with it, while also providing a path for those who wish to avoid the burdens of fiduciary status to avoid it… by being clear that they really are not advisors, and are simply acting in a sales capacity, so the consumer is clear about the true scope of the relationship.

{kind=link}