Alice Crundwell and William Bennett

Accurate measures of the number of firms at risk of failure are becoming increasingly important for policymakers, as corporate insolvencies are continuing to rise and interest rates are expected to remain higher than over much of the past decade. The share of vulnerable firms is often assessed by looking at debt-servicing ability via the interest coverage ratio (ICR) – companies’ earnings before tax and interest divided by their interest expense. But several other factors are also associated with a higher probability of firm failure. This post will explore the merits of looking at a combination of financial indicators of corporate distress to better measure the share of firms at risk of failure and the associated level of debt at risk.

Why does corporate distress matter for financial stability?

The share of financially distressed firms is important to monitor as firm failure can have implications for financial stability if it results in the firm defaulting on their debt. Real economy impacts such as job losses and reduced investment may also be felt, as shown in Figure 1 below.

While the failure of one firm is unlikely to have financial stability implications, the failure of many firms with high outstanding debt could impact bank capital positions and bondholders’ investments. In turn, a wave of corporate defaults could lead lenders to tighten their appetite to lend to real economy borrowers, amplifying financial stress.

Figure 1: Financial stability channels from corporate debt vulnerabilities

How is corporate distress typically measured?

The Bank of England’s Financial Policy Committee aims to ensure that any build-up of debt vulnerabilities in the UK corporate sector does not pose risks to the wider financial system. Historically, one of the ways they have assessed this risk is by looking at the debt-weighted share of UK corporates with an ICR below 2.5 – that is, their earnings before interest and tax are less than 2.5 times the interest paid on outstanding debt. Companies with low ICRs are more likely to experience difficulties in making their debt payments.

While this remains an accurate measure of corporates at risk of experiencing repayment difficulties, there are other financial variables that have been identified as key for firm survival. This raises the question of whether there are benefits to using multiple measures to assess corporate vulnerability.

Analysis in the December 2023 Financial Stability Report suggests nearly 30% of debt-weighted firms had an ICR below 2.5 in 2022. Though this seems very high, it likely captures firms which have a low ICR for reasons other than being in poor financial health. For example, a firm may have a low ICR if it has made an early repayment on a loan. This would lead to the firm being classed as ‘at risk’ even if they are financially stable in reality.

Developing a broader measure of corporate distress

This post extends the econometric analysis underlying the ICR threshold to identify additional financial ratios, and associated thresholds, that predict corporate failure within three years. These financial ratios give a more holistic view of corporate vulnerabilities instead of just focusing on debt-servicing pressures.

Our analysis uses data on firm financials from the Bureau van Dijk Fame database covering the period 2000–20 and applies a probit regression methodology to test the significance of ICRs and the five additional financial ratios flagged in the literature as critical for firm survival: liquidity, return on assets, turnover growth, leverage, and leverage growth.

We then ran a second set of probit regressions, regressing firm failure within three years on a single dummy variable representing whether or not a firm’s financial ratio has breached a given threshold. This specification included a vector of firm specific and time fixed effects to isolate the effect of the indicator on the probability of firm failure. We repeated this regression for different threshold values for the dummy variable. For example, when looking at return on assets (RoA) we ran this regression 20 times, with the threshold for the low RoA dummy ranging from -0.5% to +0.5% in 0.05 percentage points increments.

We used the results of this probit regression analysis to determine at which point the relationship between each financial ratio and the probability of failure strengthens. Put simply, at which value of each financial ratio there is a sudden increase in the probability of firm failure within the next three years.

Regression analysis results

The results of the incremental regression analysis on RoA are shown in Chart 1. When a firm’s RoA falls below zero, the marginal effect coefficient for failure within three years picks up significantly. As expected, this means firms with a negative RoA are much more likely to fail within three years than firms with a positive RoA.

Chart 1: Incremental regression analysis on RoA shows steepening at a value of 0

Chart 2: Incremental regression analysis on ICR does not show notable steepening

Unlike RoA there isn’t a notable steepening at any point in the results of the incremental regression analysis on ICRs (Chart 2). We conducted further tests and determined that the fit maximising point is 1.5, slightly lower than the 2.5 threshold used previously.

Using a lower threshold for what constitutes a firm with a low ICR means this now captures a narrower set of firms. However, while it may be appropriate to continue to use the 2.5 threshold when looking at ICRs alone, using a tighter threshold when looking at ICRs in combination with other metrics may be justified. First, due to the broader set of metrics this work considers to be relevant corporate vulnerability – a firm may no longer be considered as having a low ICR, but may still breach one or more of the other ratios that makes firm failure more likely. Second, previous analysis assessed firms of all sizes, whereas the data in our current sample only covers large firms. This lower threshold for larger firms is intuitive; in general, large firms have better access to credit, higher turnover, and larger cash buffers than smaller firms. This means they are able to withstand higher debt-servicing pressures before going insolvent.

The results of these regressions on all six ratios, shown in the table below, allowed us to establish the thresholds for each financial ratio at which firm failure became significantly more likely when breached.

| Financial ratio | Threshold | Three-year probability of firm failure when threshold is broken |

|---|---|---|

| ICR | <1.5 | 4.5% |

| Liquidity | <1.1 | 3.9% |

| RoA | <0% | 3.7% |

| Turnover growth | <-5% | 3.5% |

| Leverage growth | >5% | 3.0% |

| Leverage | >1 | 2.6% |

The second set of results (column 3) shows the probability of firm failure within three years when each threshold is breached individually. ICRs have the highest associated probability of failure (4.5%), meaning a firm breaching the ICR threshold is more likely to fail within three years than a firm breaching any of the other five thresholds.

Estimating the share of debt at risk

In order to assess changes in corporate vulnerability over time we have used these thresholds to create an aggregate metric which measures debt at risk. The probability of a firm’s failure increases when more thresholds are crossed simultaneously. Our results found that firms breaching three thresholds had approximately a 5% failure rate at the one-year horizon, and a 10% failure rate at the three-year horizon.

Given this, we consider corporates that simultaneously breach the three thresholds associated with the greatest likelihood of firm failure to be at higher risk of default. These are ICRs, liquidity, and RoA. In other words, a company with relatively large debt payments, very little available cash to meet them, and no profits, would be more likely to fail in our analysis.

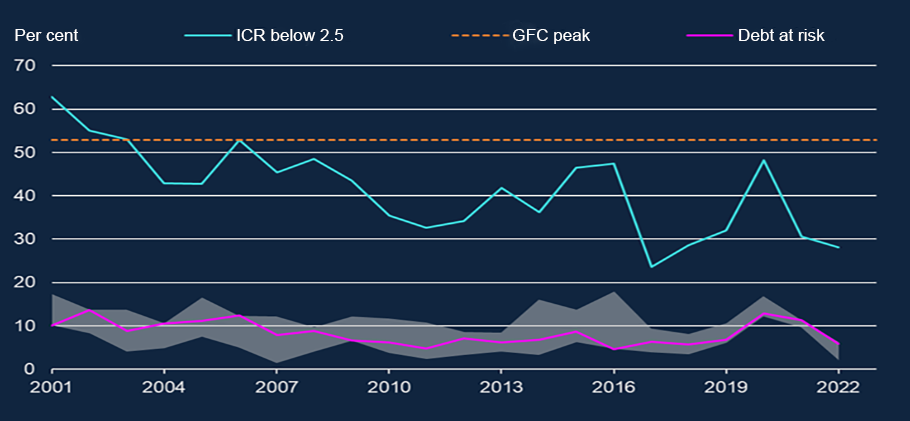

Chart 3 shows the share of debt accounted for by firms which simultaneously breached these three thresholds for each year in the sample. And the swathe represents sensitivity checks done around this metric, comprising of different combinations of three thresholds used to calculate the share of debt associated with vulnerable corporates.

Chart 3: Time series showing debt-weighted share of firms with low ICRs compared to the new debt at risk metric

Looking at the two measures together, the ICR line is much higher. This is because it captures debt associated with firms breaching only one of the six indicators, whereas the debt at risk metric is looking at firms breaching three of the six.

What can we infer from this new measure of corporate distress?

This new metric is a broader assessment of UK corporate vulnerability beyond repayment difficulties. By including firms that breach the liquidity and RoA thresholds as well as the ICR threshold, our approach can better estimate how the macro environment may impact corporate vulnerability. This is becoming increasingly important as high interest rates will continue to apply pressure to leveraged firms, with liquidity buffers expected to be drawn down in cases where firms are unable to meet these higher interest payments through profits alone. In addition, a slowdown in economic activity will likely reduce the earning capacity of many firms, adding further to the pressures felt by the most vulnerable firms.

This new debt at risk metric provides a broader view of corporate vulnerabilities, while simultaneously allowing us to focus in on the firms which have an elevated probability of failure. While analysis solely focusing on ICRs remains useful to determine the share of corporates at risk of being unable to service their debts, this post has shown that it likely overestimates the true share of firms at risk of failure and default. Our approach attempts to more accurately measure the risks facing the UK corporate sector, and the financial stability risk posed by corporates themselves, by assessing debt at risk according to a wider range of financial indicators.

Alice Crundwell works in the Bank’s Macro-financial Risks Division and William Bennett works in the Bank’s Macroprudential Strategy and Support Division.

If you want to get in touch, please email us at bankunderground@bankofengland.co.uk or leave a comment below.

Comments will only appear once approved by a moderator, and are only published where a full name is supplied. Bank Underground is a blog for Bank of England staff to share views that challenge – or support – prevailing policy orthodoxies. The views expressed here are those of the authors, and are not necessarily those of the Bank of England, or its policy committees.

Share the post “Stressed or in distress? How best to measure corporate vulnerability”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}