This framework was first circulated to FundsIndia clients on 01-Mar-24, as we exited from our Small Cap Tactical call

Are Small caps in a bubble?

Here is our 6 lens framework (Price Cycle – Long & Short, Valuations, Flows & Sentiments, Earnings Growth Environment, Past Returns) to evaluate where we are in the small cap cycle.

Instead of taking a unidimensional view, the attempt is to view the small cap cycle from 6 different vantage points to identify the ‘elephant’!

What qualifies as a ‘Bubble’ in small caps?

The valuations are so high that even after a 25% correction, it would still remain expensive and doesn’t make sense to enter!

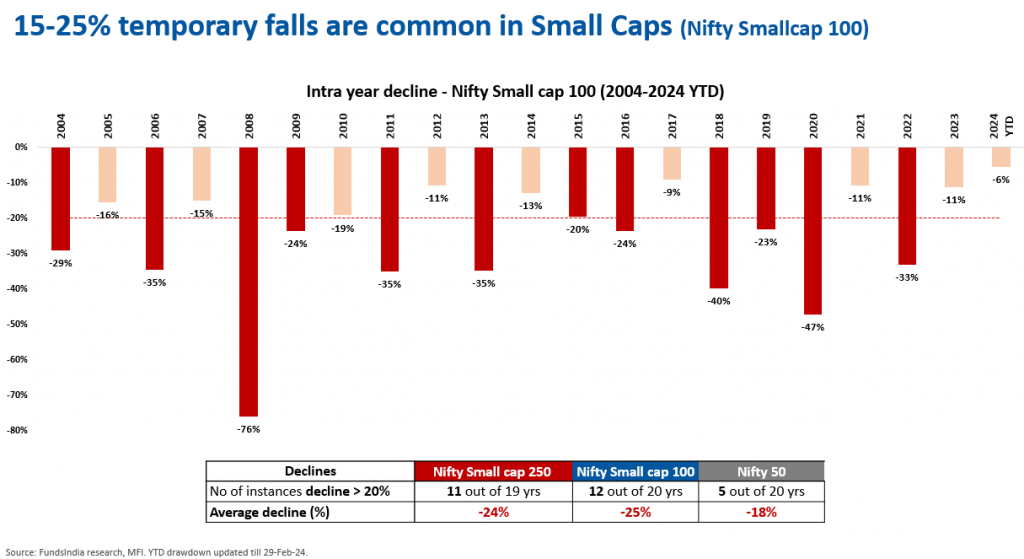

Why 25% correction?

6 Lens Framework to Analyse Small Cap Segment

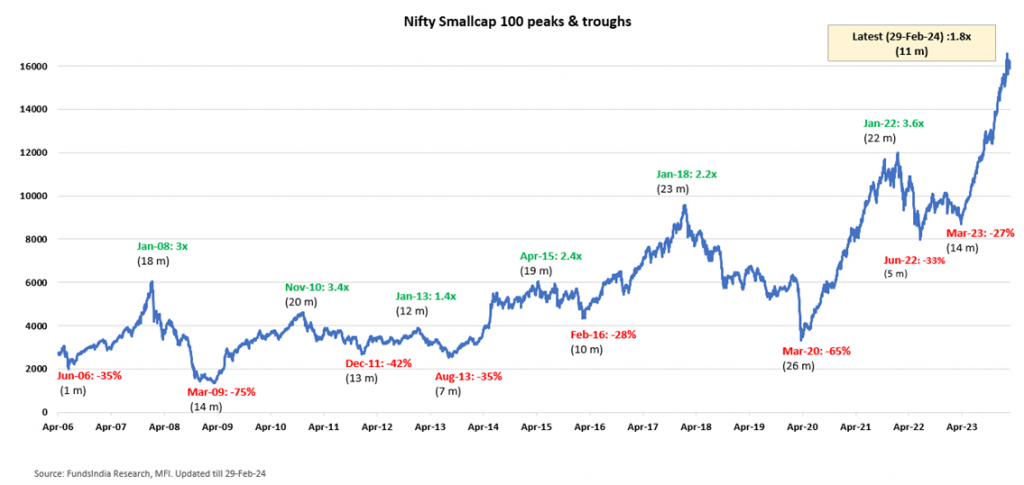

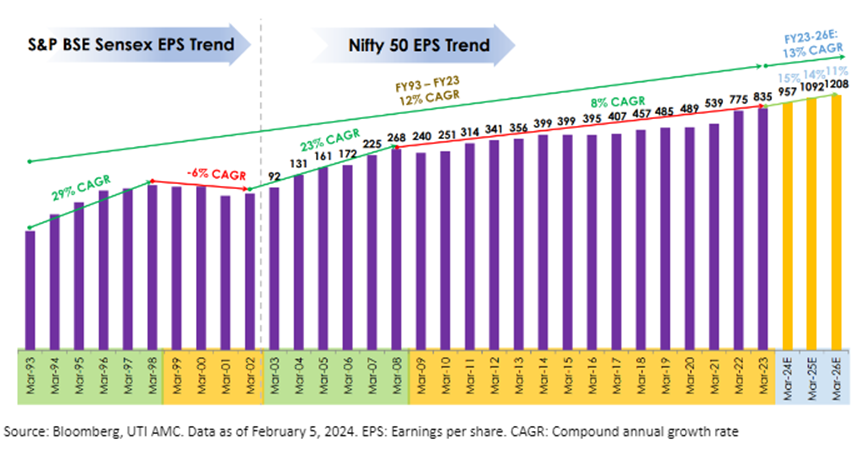

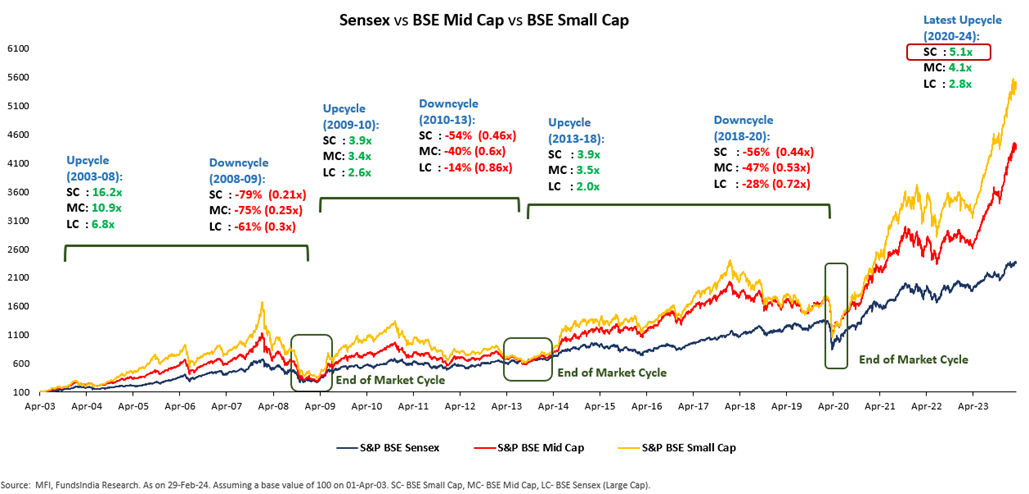

LENS 1 – LONG PRICE CYCLE: Long Cycle Indicator is flashing ‘red’ – close to historical highs

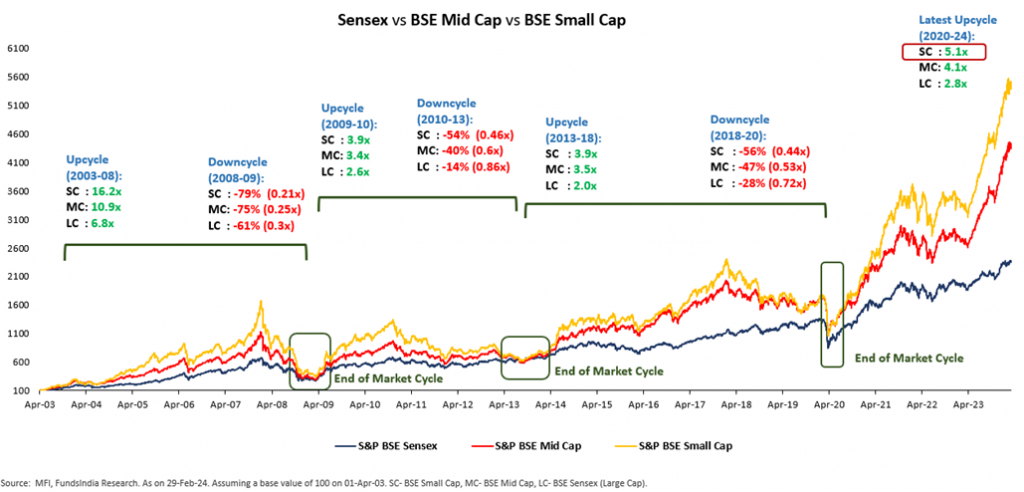

Small Cap Price Cycle – Current rally at 5.1x times from 2020 lows

Large, Mid & Small Caps tend to converge over long cycles, but small caps do disproportionately well in upcycles and vice versa. Currently, Small Caps have seen a sharp rally of 5.1x from the bottoms in Mar-2020.

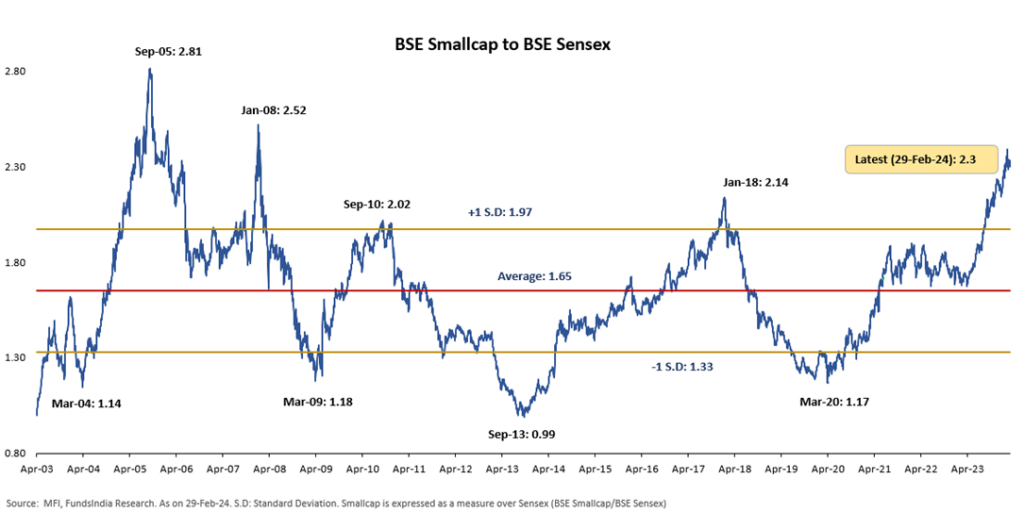

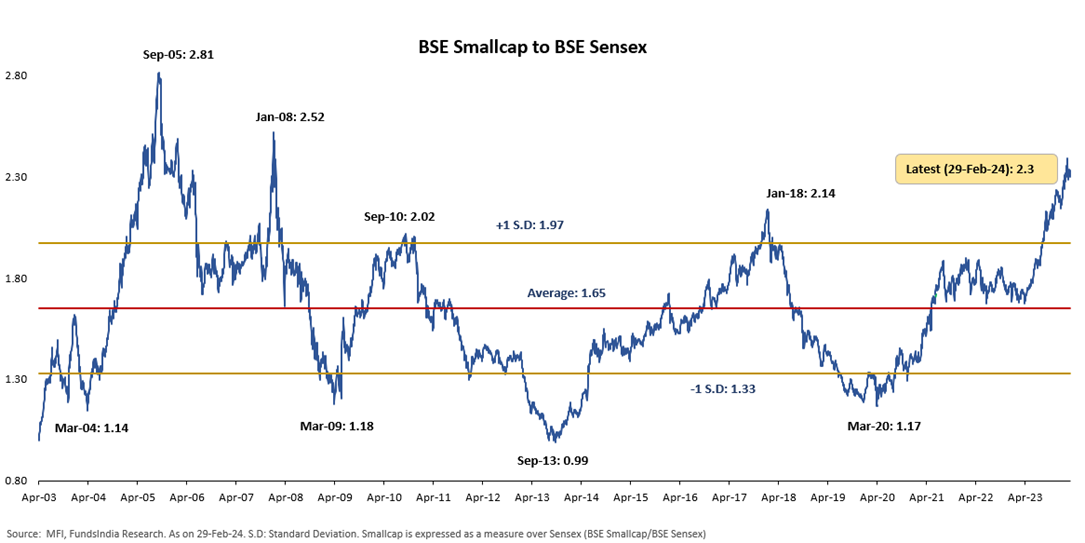

BSE Small Cap to BSE Sensex ratio close to 16 year highs

Historically whenever this ratio has crossed 2.0x the small caps segment has fallen in the short term. Small Cap to Large Cap ratio (currently at 2.3x) has crossed 2018 peak levels and is moving closer to 2008 peaks indicating ‘high risk’. This necessitates caution at the current juncture.

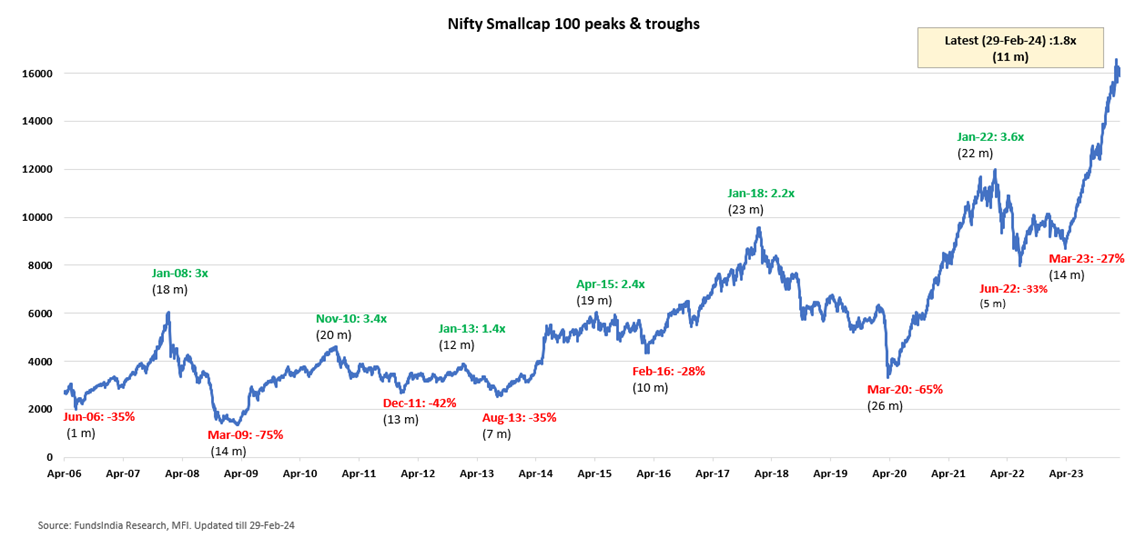

LENS 2 – SHORT PRICE CYCLE: Rally may continue for some more time (6-12 months)

In the past cycles, average time from the bottom to peak is ~1.5 to 2 years and average upside is ~2-3x.

Current rally is at 11 months with 1.8x returns indicating scope for further rally. Using history as a guide, short price cycle indicates that the rally may continue for 6-12 months.

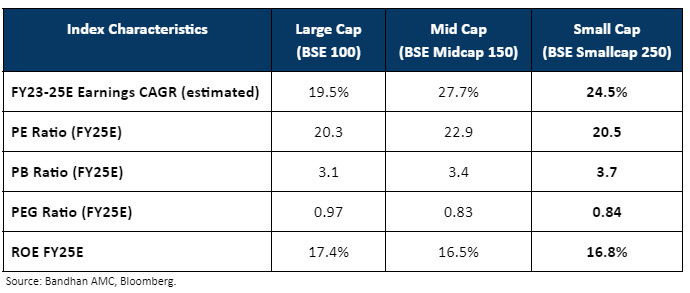

LENS 3 – VALUATIONS: Valuations have become “Expensive”

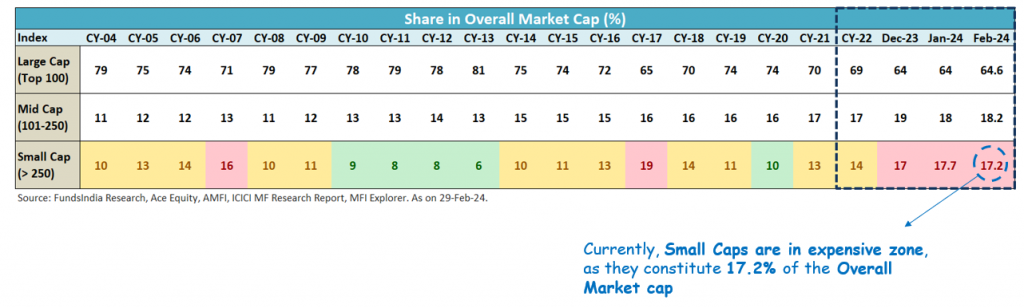

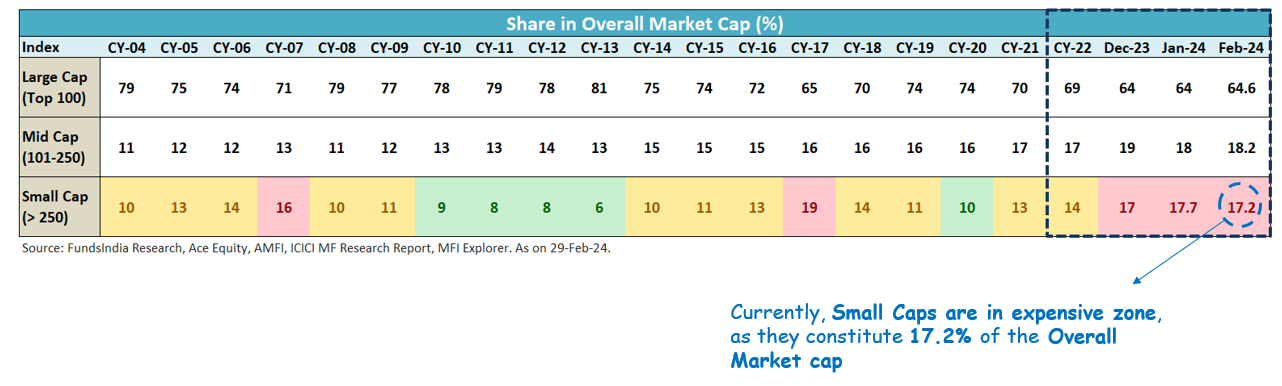

Share of Small Cap Market Capitalisation in the Overall Market Capitalisation is at higher levels (~17.2%).

Whenever the share of Small Cap MCAP in the Overall MCAP crosses 15%, it warrants caution. Currently the share is at 17.2%. The profit share of Small Caps in the Overall Market is still at lower levels (~12%) as compared to the share of Market Cap.

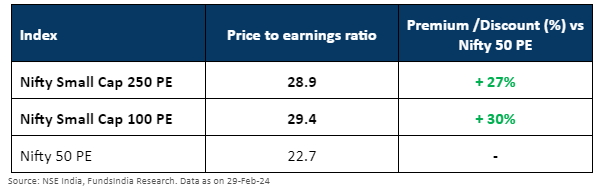

Small Caps are currently trading at a significant premium over Large Caps

Price to Earnings of Small Cap Indices are trading at historically higher premiums over Large Caps. The current premium of Nifty Small Cap 250 PE vs Nifty 50 PE is at 27%, indicating expensive valuations.

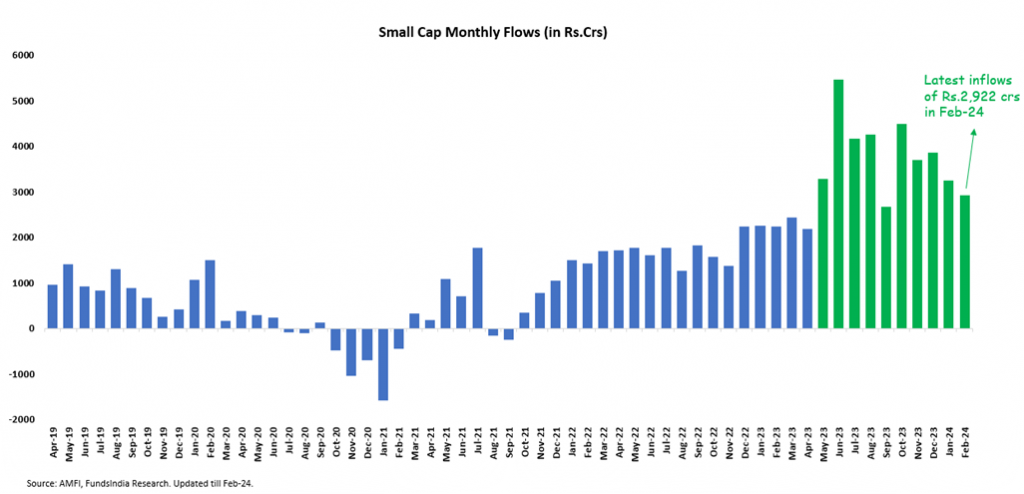

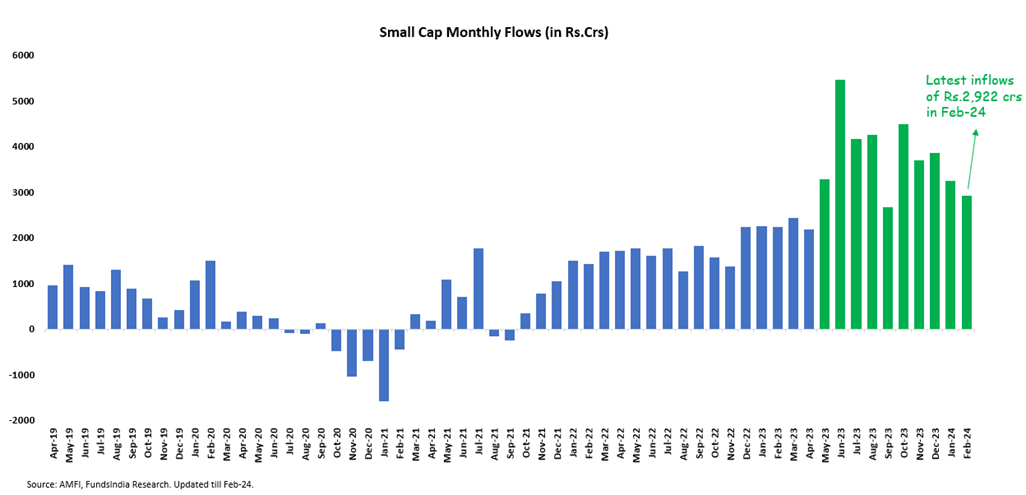

LENS 4 – SENTIMENTS & FLOWS – Sentiments indicate ‘Greed’ in the Small Cap space

There has been a significant jump in Small Cap inflows and an increasing number of new folios starting May-23.

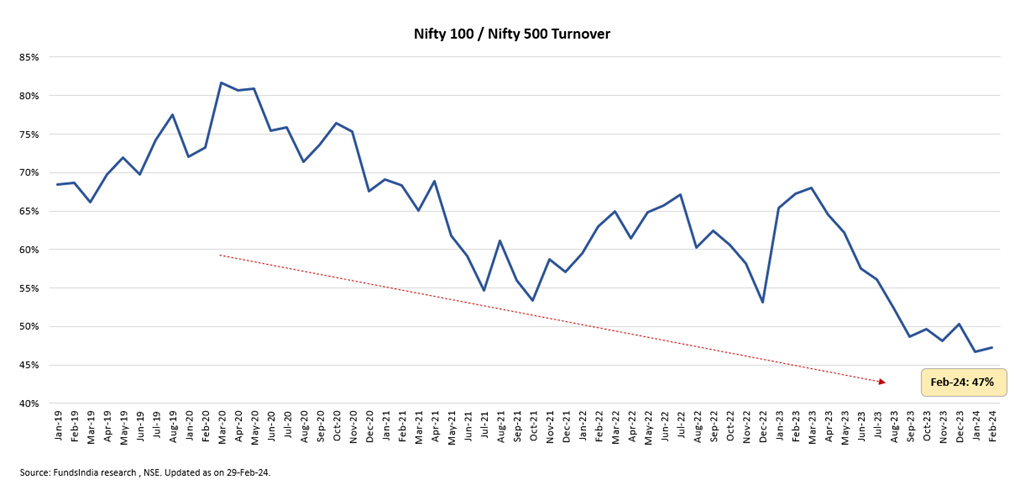

Nifty 100 Trading volume as a % of Nifty 500 has decreased indicating ‘high risk taking’ sentiments

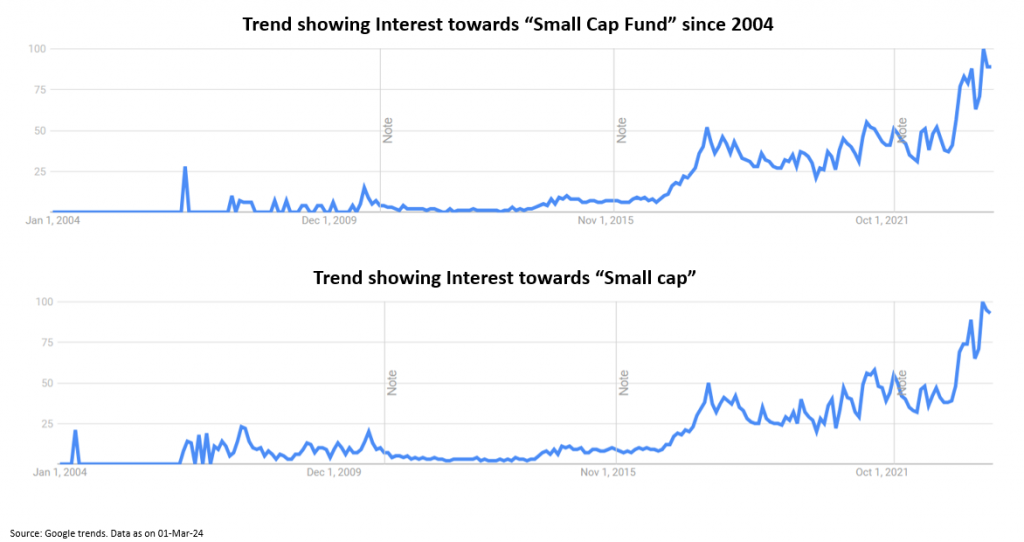

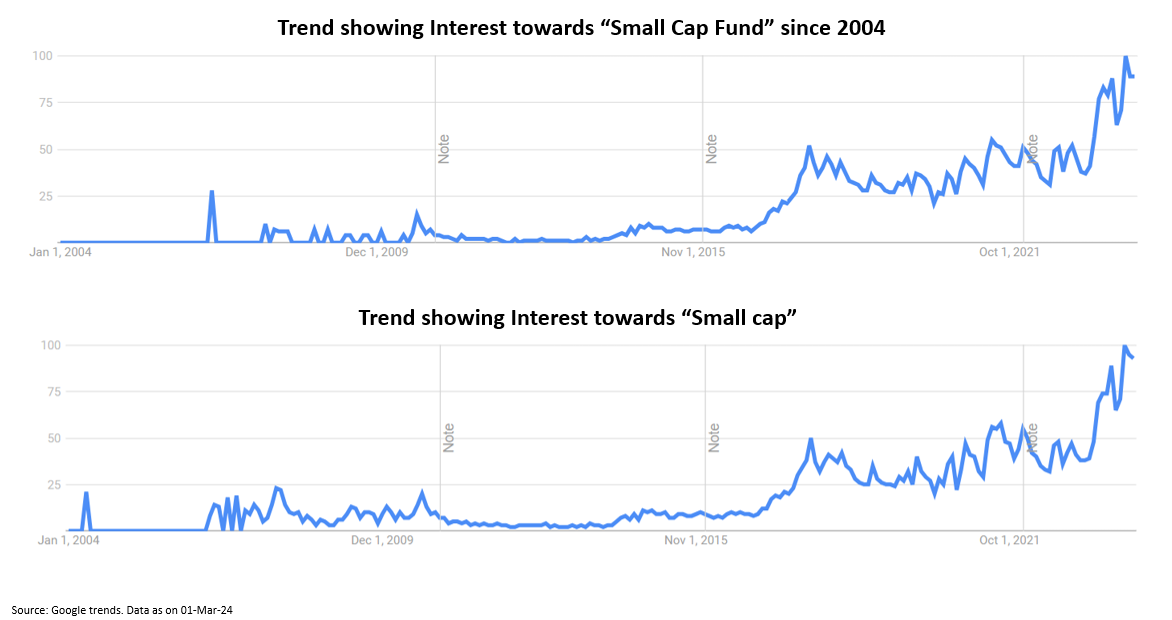

Google trends show significant Interest in the Small Cap space

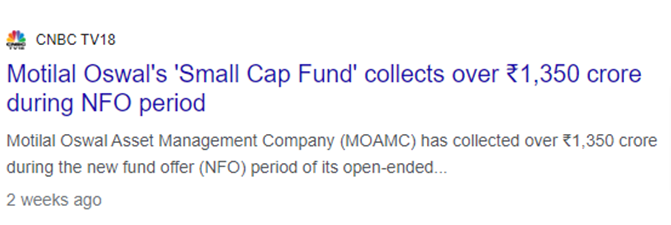

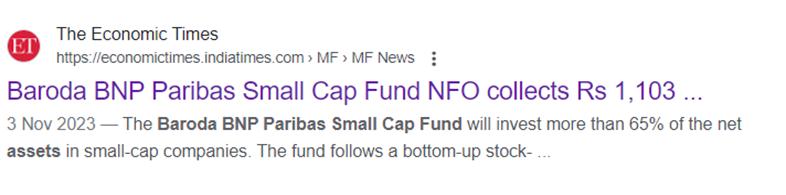

Lot of new Small Cap Funds are getting launched and garnering high AUMs despite high valuations indicating high investor interest

List of New Small Cap NFOs launched recently:

- Mirae Asset Nifty Smallcap 250 Momentum Quality 100 ETF Fund of Fund (15-Feb-24)

- Groww Nifty Smallcap 250 Index Fund (09-Feb-24)

- Bandhan Nifty Small Cap 250 Index Fund (12-Dec-23)

- Motilal Oswal Small Cap Fund (05-Dec-23)

- DSP Nifty Smallcap 250 Quality 50 Index fund (05-Dec-23)

- Quantum Small Cap Fund (16-Oct-23)

- Baroda BNP Paribas Small Cap Fund (06-Oct-23)

- Motilal Oswal Nifty Micro Cap 250 Index Fund (15-Jun-23)

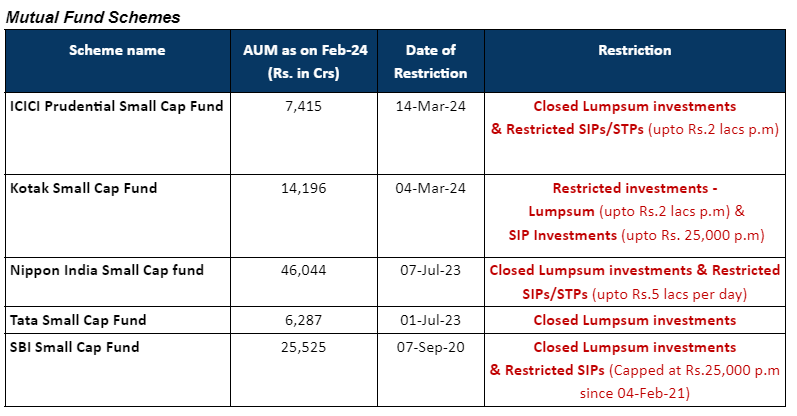

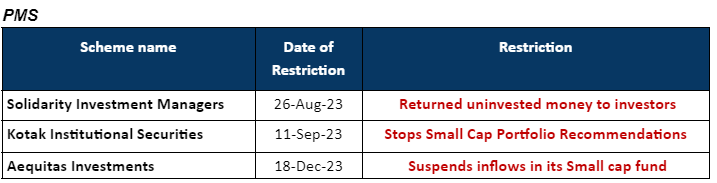

While on the other side, some cautious Fund Managers have stopped accepting flows in their Small Cap Funds citing concerns on Valuations and Flows

Mutual Funds regulator SEBI raised concerns over “froth building up in the Small and Midcap segment” amid continuing flows in these segments.

Industry body Association of Mutual Funds in India (AMFI) in a recent letter (dated 27-Feb-2024) has asked mutual funds to put in place safeguards to protect the interests of all investors in mid- and small-cap funds. AMFI sent this letter after market regulator Securities and Exchange Board of India (SEBI) raised concerns of ‘froth building up in small and midcap segments’ amid continuing flows in mid- and small-cap funds.

AMFI has advised mutual funds to take “appropriate and proactive” measures such as moderating inflows, portfolio rebalancing, conducting stress tests on sharp redemption possibility etc to protect investors from first-mover advantage of redeeming investors in case of sharp redemptions.

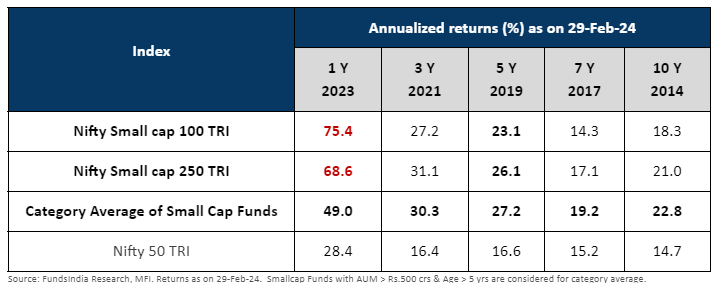

LENS 5 – PAST PERFORMANCE – Flashing “RED” Signal

Very High Past Performance – 1Y, 3Y, 5Y, 7Y and 10Y annual returns are similar to past Bubble markets -> Contra Indicator – indicating extreme optimism

- During past bubble markets, the last 1Y returns were usually above 50%. Currently, the 1Y returns for Nifty Small Cap 100 TRI is at 75%.

- 3Y, 5Y and 7Y are in the 20-30% range, which is similar to 20-25% range seen in the past bubbles.

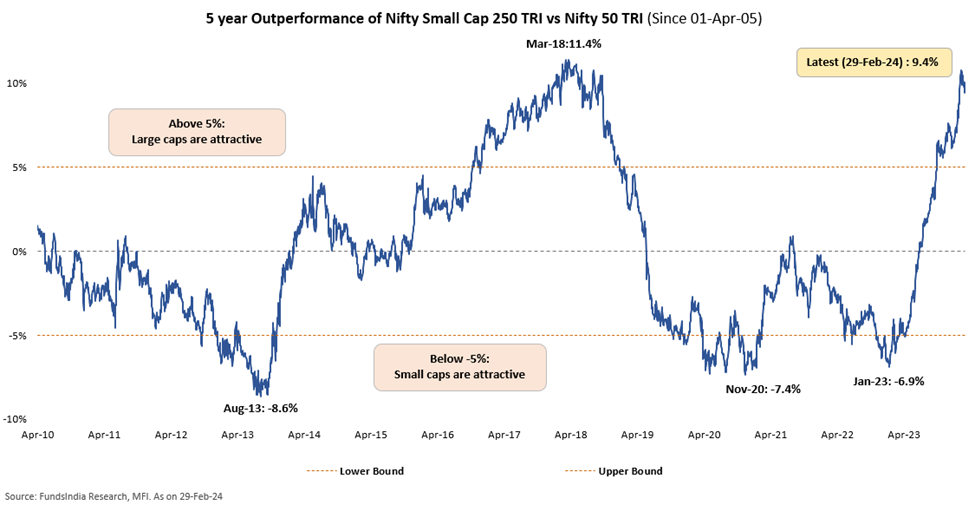

5Y Rolling return Outperformance of Small Caps vs Large Caps are closer to historic highs

The 5 year rolling outperformance of Nifty Small Cap 250 TRI vs Nifty 50 TRI is at 9.4% – closer to 2018 peak levels (11.4% outperformance vs Nifty 50 TRI).

LENS 6 – FUNDAMENTALS: Fundamentals are robust and market environment is favourable for Small Caps

Broader markets expect strong earnings growth over the next 2-3 years. This augurs well for Small Caps as they tend to grow faster than large caps in such environments.

Small Caps usually perform well in a strong earnings cycle phase. Higher Valuations of Small Caps vs Large Caps is driven by Higher earnings growth expectations. BSE Small Cap 250 is estimated to grow at ~25% CAGR over FY23-FY25 (higher than BSE 100 which is expected to grow at ~20% CAGR)

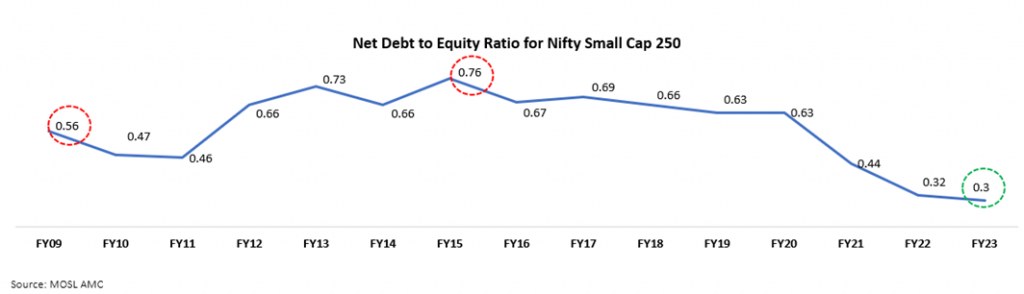

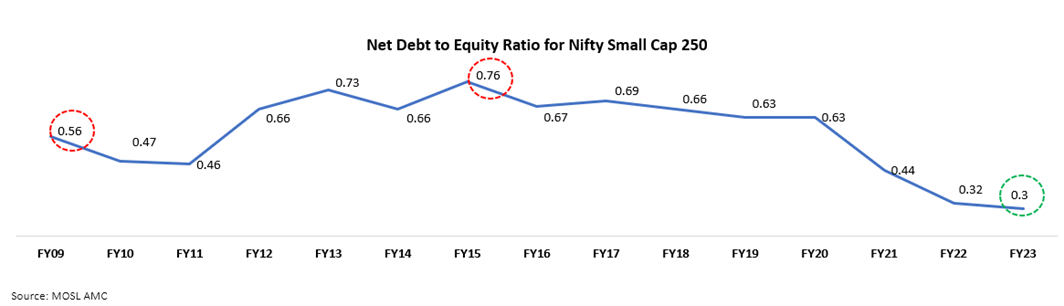

Strong Balance Sheets – Debt to Equity levels for Small caps at historical lows

Debt to Equity ratio for small caps has reduced to 0.3x in FY23 from 0.8x in FY15 – the lowest in the last 15 years

Summing it up

-> 4 of our total 6 indicators which we use to track the small cap segment are flashing warning signals:

- Negative Signals (Total 4):

- Long cycle shows that Small Caps are close to historical peak levels

- Valuations have become ‘Expensive’

- Sentiments are Euphoric – significant jump in small cap fund inflows (primarily from mutual funds) + few funds closing for fresh inflows + Lot of New NFO launches

- Past performance – contra indicator – very high past returns warrants caution

- Positive Signals (Total 2):

- Short cycle – Historically, the Small Cap short cycle from bottom to peak lasted for ~1.5 to 2 years. The current small cap rally had started from Mar-2023. If we use previous short cycles as a rough guide, the current rally may continue till second half of FY25 (Oct-24 to Mar-25)

- Strong Fundamentals for Small Caps – Improving Profitability (ROE) + Higher Earnings Growth + Strong balance sheets (low debt)

- Trigger to Monitor:

- SEBI’s actions to moderate flows into small and midcaps

- Mutual Fund Stress Test Results

- Liquidity risk in small cap funds/PMS

View -> Time to be CAUTIOUS!

What does this mean in ENGLISH?

Small Caps are not in a bubble (read as chances of a large 50-70% fall is very low) – as

- Fundamentals remain strong – Robust earnings growth + Healthy balance sheets

- Short Price Cycle Lens indicates further legs to the rally

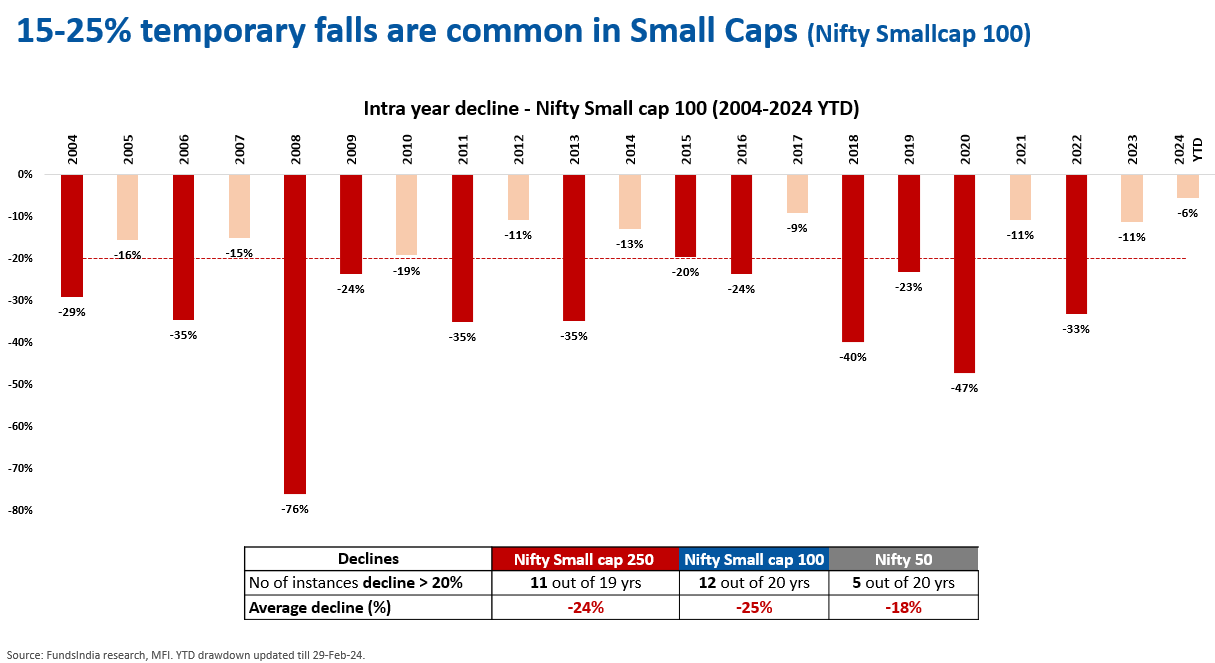

However, the odds of a temporary 20-30% correction has significantly increased at this juncture as Long Price Cycle, Valuations, Flows & Sentiments, Past Performance lens – all signals are flashing RED.

What should you do?

- Rebalance your Small Cap exposure back to original allocation.

- If overexposed, reduce Small Cap exposure to <15- 20% of your Equity portfolio (as per your risk profile)

- Continue your SIPs only if your time frame is >7 years

- For Incremental Investments: Avoid Large Lumpsum Allocations

Other articles you may like

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}