Financial advicers are intimately familiar with the phrase, “Past results are not indicative of future performance.” Every document that considers the facts around any particular asset class will invariably include that disclaimer, but constructing a portfolio consisting of a mix of equities, fixed income, and other assets requires investors and advicers to make some fundamental assumptions around long-term expected returns and correlations between assets. 3 common assumptions that have driven asset allocation decisions for decades are that 1) equities have historically outperformed fixed income over the long-term, 2) bonds act as an effective diversifier in a portfolio since they are negatively correlated to stocks, and 3) various combinations of non-correlated assets improve a portfolio’s expected return per unit of risk. However, as investors learned in 2022, when the S&P 500 and 20-year Treasury Bonds fell 18.1% and 26.1%, respectively, historical “tendencies” don’t always hold over shorter timeframes, prompting the question: How reliable are our assumptions around the long-term performance of stocks and bonds?

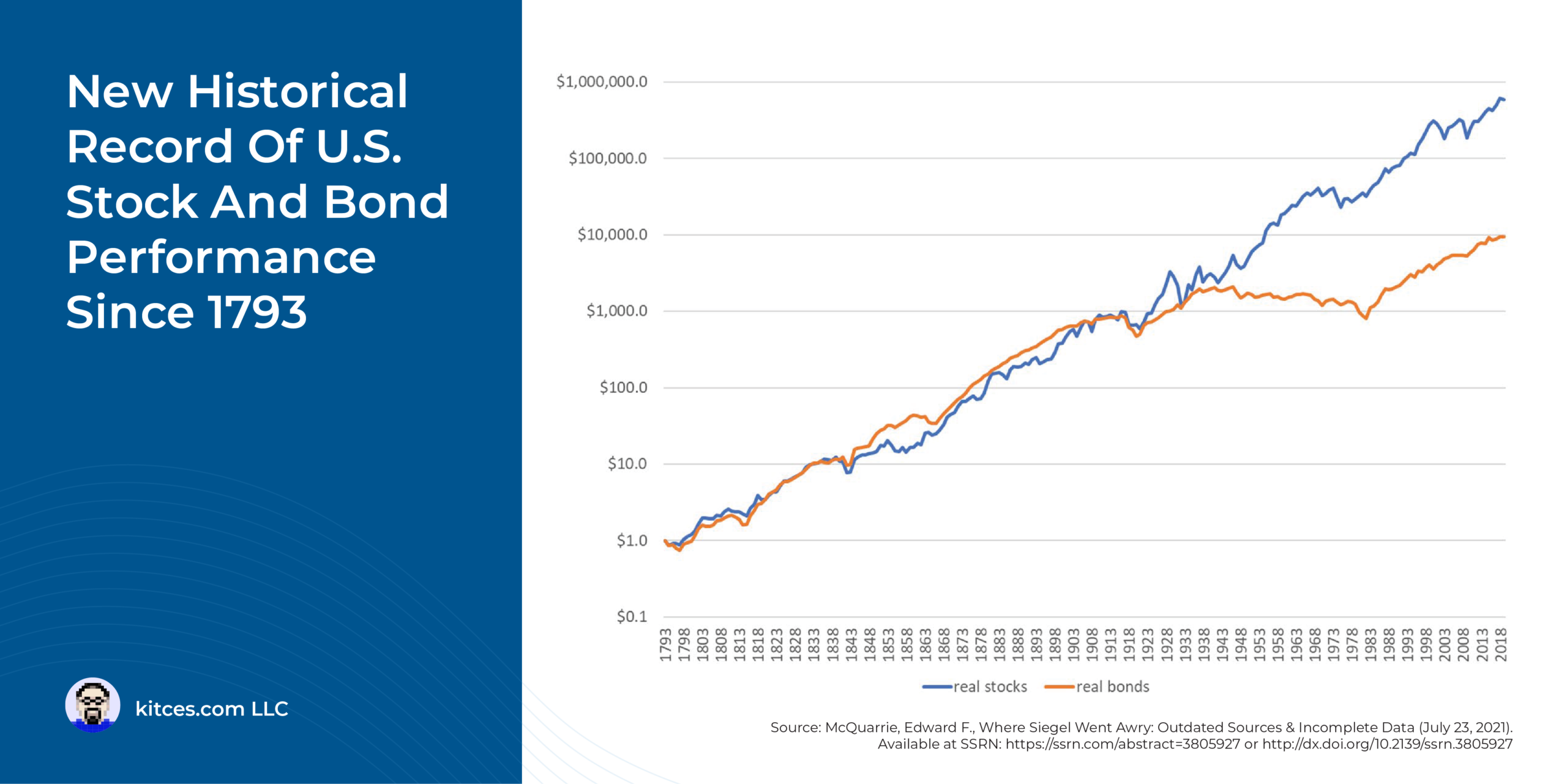

On the one hand, in an analysis of data going back to 1802 in his seminal book, “Stocks For The Long Run”, Jeremy Siegel concluded that stocks outperformed bonds over long periods. However, Edward McQuarrie, author of the 2023 study “Stocks for the Long Run? Sometimes Yes, Sometimes No,” reached back even further to 1793 and expanded the data set to include 3–5X more stocks and 5–10X more bonds. Accordingly, McQuarrie found that, while stocks did indeed far outperform bonds between 1942–1981, not only did stocks and bonds produce about the same wealth accumulation during the 150-year period before 1942, but the same held true from 1982–2019 as well.

So, although the entire 227-year span of McQuarrie’s analysis from 1793 to 2019 was weakly supportive of Siegel’s conclusions, there were subperiods where bonds actually outperformed stocks, leading McQuarrie to conclude that there was no consistent relationship between asset outperformance and length of holding period to which values must revert. Instead, McQuarrie argued that the changes over various periods depend solely upon the ‘regime’ in place, where a regime is defined as “a temporary pattern of asset returns” characterized by “ceaseless variation” over time.

Meanwhile, McQuarrie also found that stock-bond correlations have also been “highly variable over 20-year intervals, ranging all the way from about −0.70 to 0.90”, suggesting that, in addition to performance, correlations are also subject to regime changes and that bonds don’t always effectively diversify risk. In fact, they can even magnify risk, as was the case for the 7 decades between 1926–1999, when the stock-bond correlation was a positive 0.18.

Finally, over time, regime changes have also lowered the overall risk of equity investing. For example, the creation of the Federal Reserve in 1913 and the SEC in 1934 have helped to reduce economic volatility and increase corporate transparency. These changes, along with lower trading costs, have made the world a much safer (and less expensive) place for investors, who, as a result of reduced investment risks, may experience lower future returns.

There are several takeaways for advicers as they serve their clients. First is the fact that stocks (specifically because they carry a higher risk level) have not always outperformed bonds, and while stocks should carry a risk premium, advicers can turn to Monte Carlo simulations to consider a wider dispersion of outcomes, versus relying on ‘expected’ returns when developing investment plans. Second, the stock-bond performance-correlation relationships are regime-dependent, and those regimes are neither time-dependent nor mean-reverting.

As a result, an advicer’s primary consideration when developing asset allocation plans should be the diversification of risk, while accounting for the fact that bonds won’t always be an effective tool to achieve such diversification. Moreover, advicers might consider incorporating alternative investments into client portfolios, including things such as long-short factor strategies, private equity debt, reinsurance, consumer and small-business lending, among other assets. Ultimately, the key point is that there are asset classes outside the traditional stock-bond universe that can be used to create portfolios that are more diversified and that may be better suited to address a particular client’s ability, willingness, and need to take risk!

{kind=link}