Small business owners often treat their businesses not only as their source of income during their working years, but also as an asset that can be sold to fund their retirement. And while many businesses can build up substantial value over the years, the downside is that, when that value is realized upon the sale of the business, a large amount of it is treated as taxable income. And for many business sales that create capital gains of more than $500,000, the one-time spike in taxable income created by selling a business can bump the seller into a higher income tax bracket, requiring them to forfeit a significant chunk of their funds needed for retirement to pay their own tax bill on the sale.

One way to reduce the tax impact of selling a small business is by using an installment sale. Under IRC Sec. 453, capital gains on the sale of assets, such as privately held businesses where the payments are spread out over a period of 2 or more years, are deferred until the years when the payments are actually received. Which not only defers the taxes owed on the sale to future years, but can also reduce the absolute amount of tax on the sale by spreading out the tax impact over multiple years and keeping the seller within the lower capital gains tax brackets.

The downside to installment sales, however, is that, being essentially a loan from the seller to the buyer of the business, the seller takes on the risk that the buyer may ultimately be unable to make their payments as required by the installment note. Additionally, it can sometimes be difficult for a business seller to even find a buyer who is willing to agree with them on the terms of an installment note. And furthermore, because an installment sale involves one or more payments being deferred until future years, the seller can’t use or invest any of the sales proceeds until they’re actually received.

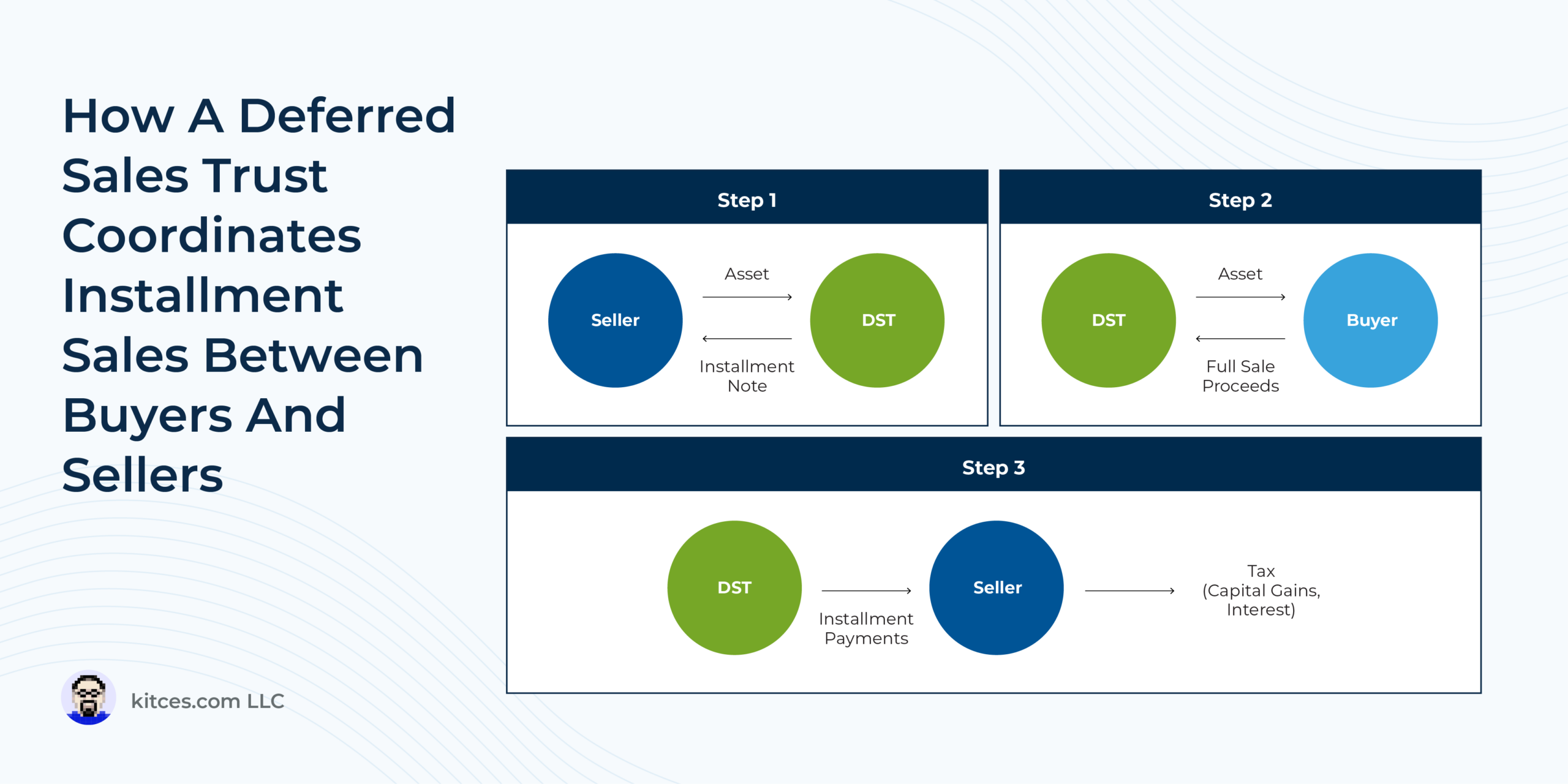

One purported solution to the issues with installment sales that has been promoted by a group of accountants, attorneys, and financial advisors is known as a Deferred Sales Trust (DST), which works by using a third-party (the trust itself) to buy a business or other asset from the seller under an installment agreement, rather than selling directly to the ultimate buyer. The trust then sells the asset to the buyer in a lump-sum transaction and invests the proceeds to pay back the seller under the terms of the installment agreement. As the sales pitch goes, this allows the seller to benefit from installment sale treatment, while eliminating the credit risk of selling to a buyer and giving them at least some ability to choose how the proceeds are invested even before they actually receive them.

However, closer scrutiny of the DST strategy raises significant red flags that aren’t included in the sales pitch. For one thing, details of the strategy are kept closely under wraps by the group that promotes and sells DSTs, limiting advisors’ ability to vet the DST’s legitimacy. Additionally, although DST promoters tout the strategy’s ability to eliminate the credit risk of entering an installment agreement directly with a buyer, in reality, the risk is simply shifted to the trust itself: Because the seller cannot be the owner, trustee, or beneficiary of the DST (because doing so would cause the transaction to lose its installment treatment), they are wholly reliant on the trust to be able to make its required installment payments. Meaning that, for example, if the DST trustee mismanaged the sales proceeds and caused them to default on the installment loan, the seller would have no recourse to recover those funds. (While at the same time, any extra funds that are left over after the note is fully paid off go to the DST trustee, not the business seller – a true ‘heads I win, tails you lose’ proposition.)

In other words, the characteristic that is needed to make DSTs work from a tax perspective – the ceding of all control over the sales proceeds to a third-party trustee – can make them even more risky than a traditional 2-party installment sale. Which is why instead, sellers of small businesses may want to consider other strategies such as structured installment sales (in which the installment note is funded by a large insurance company that has significantly more assets with which to pay off the loan), entering into the installment agreement directly with the buyer, or even simply selling as a lump-sum and taking the entire tax hit in 1 year – which, while being possibly less favorable from a tax perspective, at least ensures that the seller receives all of the sales proceeds to begin with!

{kind=link}