In recent years, I’ve seen friends around me in their 30s and 40s leave this world abruptly due to sickness or an accident. My friend, who’s a neurosurgeon, also sees cases of head trauma where people get into unexpected accidents and lose their mental capacity in their 40s and 50s.

I’ve also seen what it does to their family, especially if they neglected to draw up plans or a will that would take care of their loved ones in their absence.

This made me sit up and be mindful as I too, have not made any of such provisions ever since my second child was born.

Growing up in an Asian family, many of our elders would say “touch wood!” when we try to even raise this topic. In retrospect, it makes us not see the importance of planning too.

But if we don’t plan today, then when? Nobody will be able to do it for us.

So today, join me as we break generational trends and do the right thing for our loved ones.

What actions can we take as part of pre-planning?

Now that I’ve seen what can happen, I think frequently about my children’s future – this includes plans for if something were to happen to me one day before they come of age.

Here’s a list of what I have set out to do:

- Make a CPF nomination (as CPF savings cannot be distributed through a will)

- Set up a will on how to pass my assets on

- Make my Lasting Power of Attorney (LPA)

- Set up Advance Care Planning (ACP) outlining my healthcare and treatment preferences, which will be kept on the National Electronic Healthcare Record (NEHR)

I’ve yet to do my ACP, so in this article, I’ll focus on the first 3 which I’ve already completed. The last on my list that I aim to complete by this year is my ACP!

Why I made a CPF Nomination

As a Singaporean, one of the significant assets most of us will be leaving behind is our CPF savings.

If there isn’t a CPF nomination, the CPF savings will be distributed according to intestacy laws following your departure, even if you did state it clearly in your will. The unnominated CPF savings would be transferred to the Public Trustee, and an administrative fee will be deducted from your CPF savings before it is distributed to your family members based on the intestacy laws or the Muslim Inheritance Certificate.

The reason this is so, is because our CPF monies do not fall under our personal estate and therefore cannot be covered by a legal will. Instead, we need to make a CPF nomination to state whom and how the savings should be distributed, in what proportions.There are reasons why CPF Savings cannot be included in a will. This helps protect against creditors, and since you can save on needing to hire a lawyer to go through a court probate process (which is necessary for wills and typically takes 3 – 6 months), this allows your CPF nominees to receive your CPF monies more quickly.

Note: I also learnt that investments made under CPF Investment Scheme (CPF-IS) are not covered under CPF nomination – read why here.

Imagine if you wanted to give certain family members a bit more (or less) depending on their circumstances. Making a CPF nomination will ensure that this happens.

In my case, even though my desired distributions are the same (for now) as how it would be under intestacy laws, I’m still making a CPF nomination so that my loved ones can receive the money in my CPF account sooner. That way, they will not need to wait for the Public Trustee to identify which of my family members are eligible to claim my CPF savings, which can take up to 6 months!

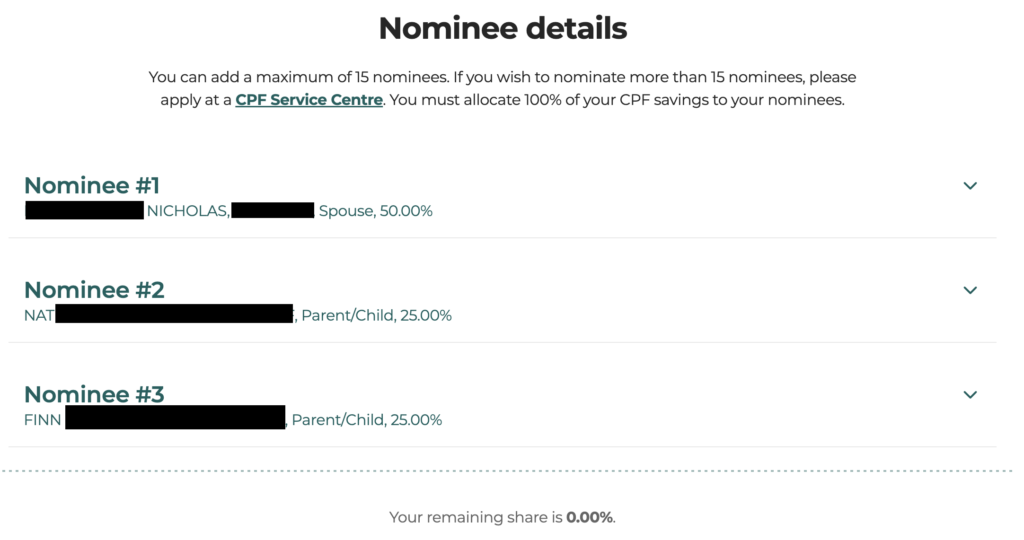

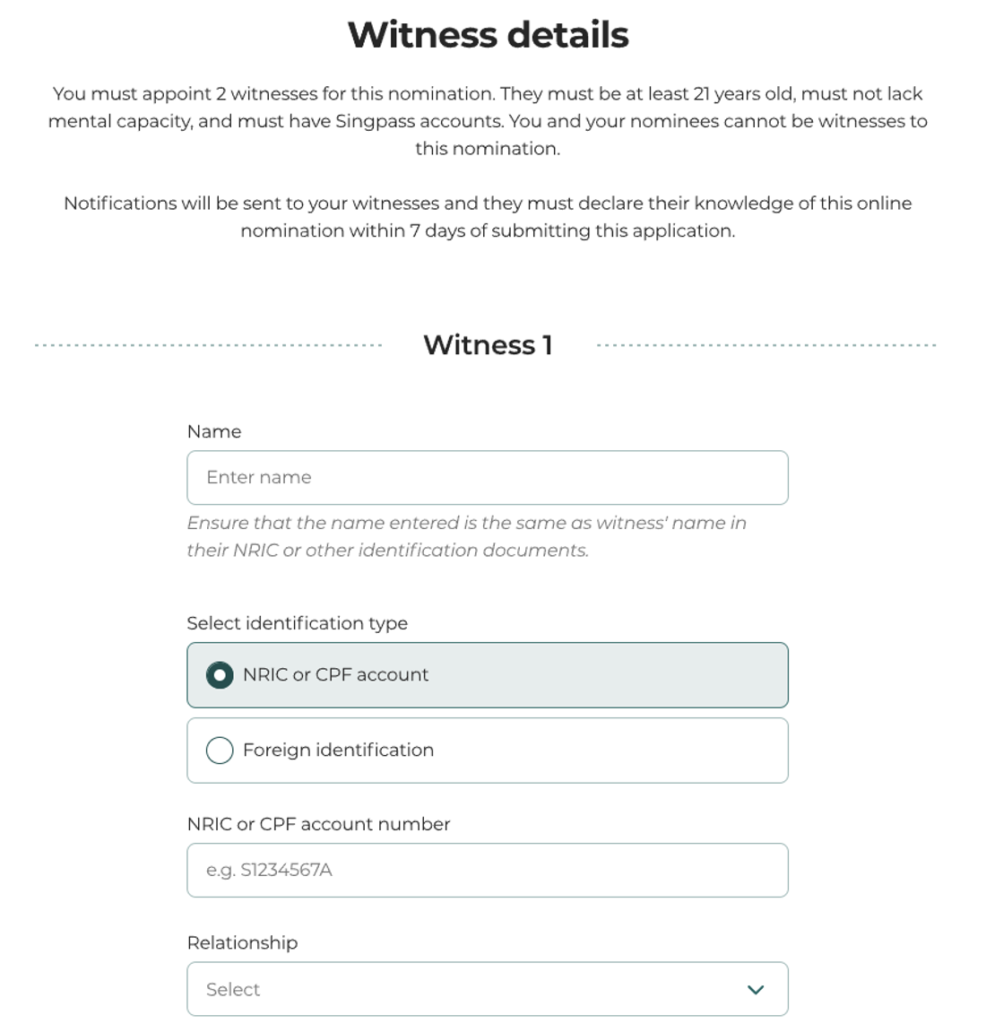

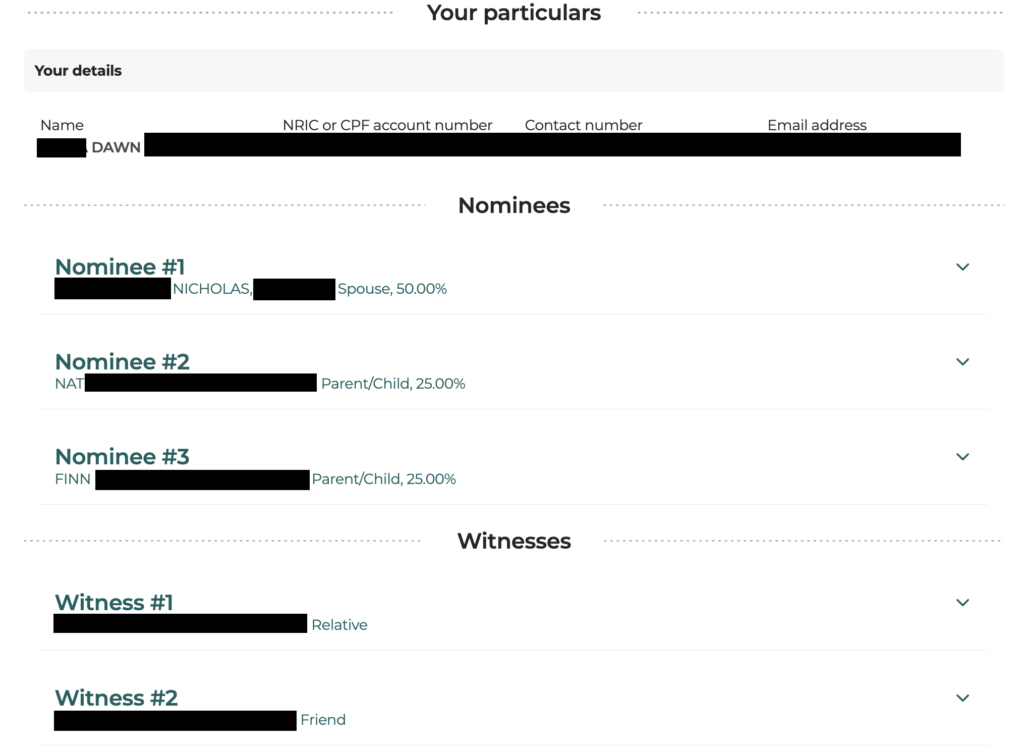

How to make a CPF nomination?

I did mine within minutes by logging into mycpf digital services with my Singpass. I simply filled in my nominees’ details along with the information of my 2 witnesses.

After completing the CPF nomination, I promptly informed my two witnesses via WhatsApp. The witnesses’ role is to simply acknowledge my nomination, and confirm that I had the intention to make a CPF nomination.

They had to do so via here, within 7 days.

What happens if I don’t make or update my CPF nomination regularly?

Aside from a longer wait time if the Public Trustee gets involved (with a fee payable), not having an (updated) CPF nomination can easily lead to disputes or resentment among your surviving family members.

I recall about a real-life case shared at last year’s CPF Board’s Ready for Life Festival. An elderly man had passed away, leaving behind 3 surviving sons. However, the youngest son was excluded from his father’s CPF nomination. This led to a huge misunderstanding among the siblings, with the youngest son believing that his elder brothers had influenced their father to leave him out of a share in the bequeathed CPF savings. The bequeath arrangement to only his 2 elder brothers also contradicted with the equal fair treatment the father had usually given to his 3 sons during his lifetime. Eventually, CPF Board discovered that the deceased’s last nomination was made before his youngest child was born! Imagine the unnecessary hurt, agony and misunderstanding the sons had to go through!

The sharing made me realise that such family disputes can have long-lasting effects, straining relationships and cause immense emotional distress for all involved, and I should do my part to prevent this from happening to my loved ones. It was a good reminder for me to not only make, but to also update my CPF nomination from time to time, especially at major life milestones such as welcoming a new child.

Did you know that a divorce does not automatically revoke your existing CPF nomination? While a marriage will render any earlier CPF nominations invalid, a divorce does not revoke it because some people may still want to provide for their former spouse and children. So…never assume!

So, take control of who gets to inherit your hard-earned CPF savings and review your CPF nomination online regularly, especially if your life circumstances change. You can see other scenarios on when you should make a new CPF nomination here.

Making a Will

Some of you might recall that I last wrote my will in 2019, before my second son Finn was born. My husband and I will be visiting our lawyer shortly to draft up a new one, as our circumstances and personal assets have changed significantly since.

If you have no budget, the good news is that Singapore recognises self-written wills. You can technically write your own will for no cost at all. If you don’t know where to start, you can read about it here. Help your loved ones to locate your will, when necessary, by securely storing its information online using My Legacy vault.

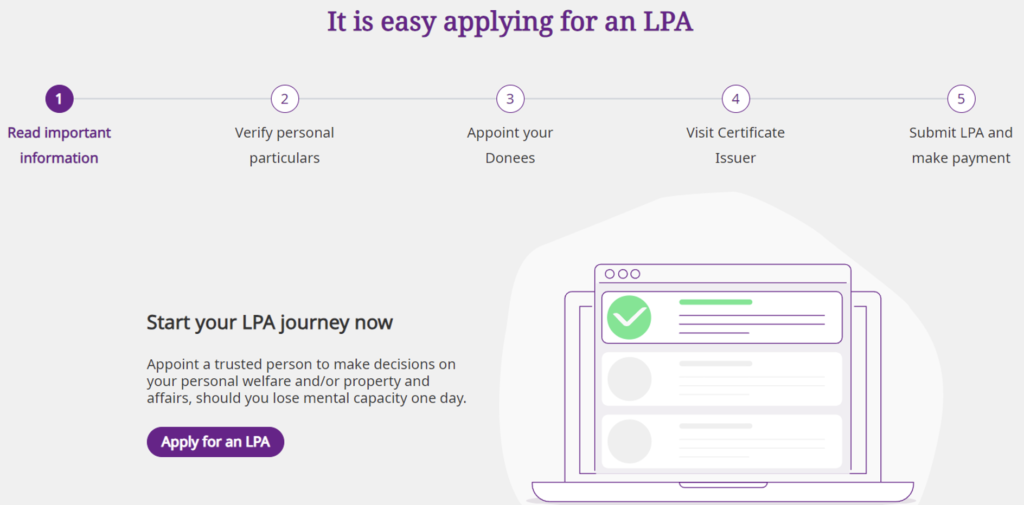

How to Make a Lasting Power of Attorney

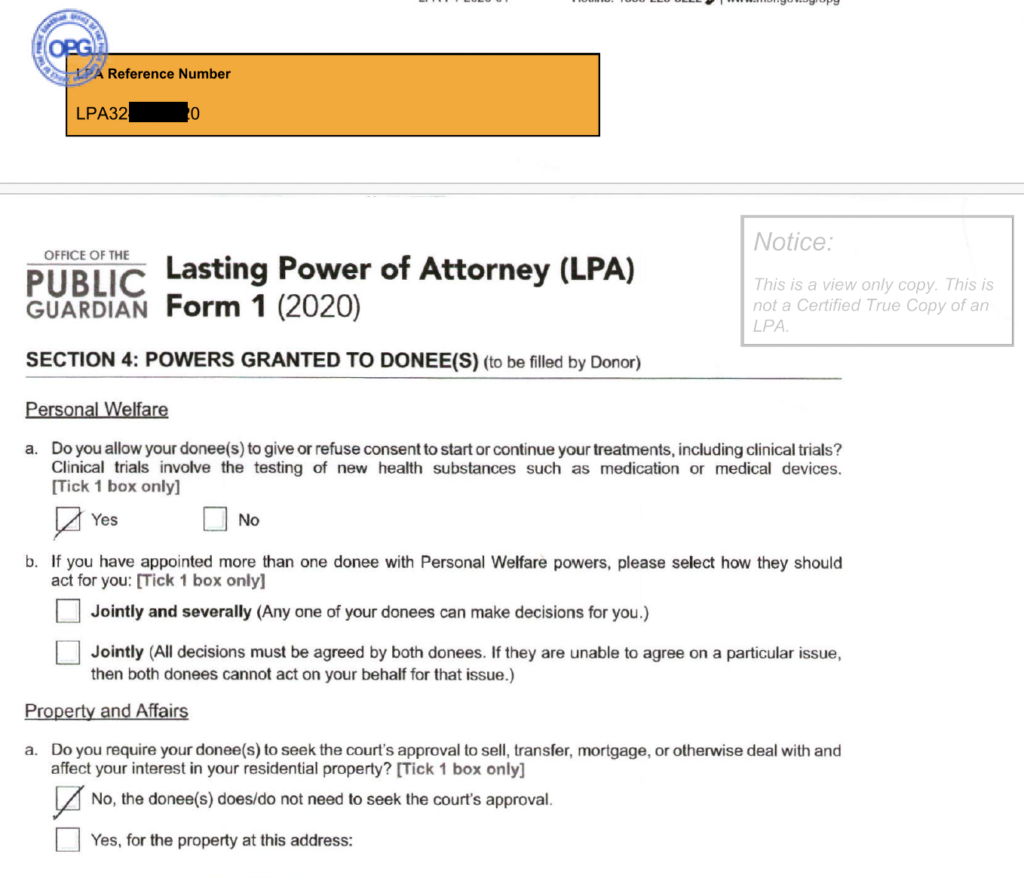

The Lasting Power of Attorney (LPA) is a legal document that allows you to appoint your trusted person(s), also known as Donee(s), to make decisions for you should you lose mental capacity. The LPA allows your Donee(s) to make decisions based on the authority that you had granted i.e. your personal welfare and/or property & affairs matters.

A few years ago, my dad got diagnosed with a severe condition that has seen him increasingly lose his lucidity and physical control. After receiving the diagnosis, the first thing he did was to update his will at a law firm and inform me.

Then, his hospital specialist advised for him to make an LPA, so we brought him to a General Practitioner (GP) near our house who was a Certified Issuer. The doctor walked him through the process and drafted it on the spot – it cost us $70 then.

OPG has also extended the application fee waiver for LPA Form 1 for Singapore Citizens until 31 March 2026. This is specifically for Donors who wish to grant Donee(s) general powers with basic restrictions. You can draft your LPA online, inform your Donee(s) and Replacement Donee (if any) to accept their appointment online before visiting a Certificate Issuer i.e. accredited medical practitioners, lawyers or registered psychiatrists, who will certify and submit the LPA via the Office of the Public Guardian Online (OPGO) for you.

Here’s how you can do it too:

TLDR: Legacy Planning is a valuable act of love for our loved ones

After we’re gone, the last thing we’d want is to leave our loved ones with burdens, or worse, fighting over our assets and falling into disharmony.

Acting on legacy planning now ensures that our loved ones are cared for per our wishes. This is an act of love we should embrace while we have the chance, sparing our family from additional burdens in the event of anything unexpected.

It took me no more than 5 minutes to make a CPF nomination online, and another hour at the doctor or lawyer to draft the LPA. Completing a legal will (if you choose to go through a lawyer) and ACP will take longer (2-3 hours each), but it will be well worth the while.

Here’s a recap of the steps for you to take:

More importantly, let’s do it while we can.

Sponsored message: Make your CPF nomination today for a peace of mind for you and your loved ones.

Disclosure: This article is written in collaboration with CPF Board, who would like to encourage more Singaporeans to start thinking about pre-planning for our loved ones today.

{kind=link}