Traditionally, the challenge in using a 529 plan to save for higher education expenses has been figuring out how much to save to cover the beneficiary’s college costs without overshooting and saving more in the 529 plan than is actually needed. Because while 529 plans’ combination of tax-deferred growth on invested funds and tax-free withdrawals for qualified education expenses (plus many state-level tax deductions or credits on 529 plan contributions) make it a powerful savings vehicle for college or graduate school expenses, the flip side is that any non-qualified distributions are subject to income tax plus a 10% penalty tax on the growth portion of the distribution. And so the conundrum of people with “too much” savings in their 529 plan – either because they overestimated how much they needed to save, or because they chose a different path entirely that didn’t involve going to college – has been how to get funds out of the plan without sacrificing a large part of their value to taxes and penalties.

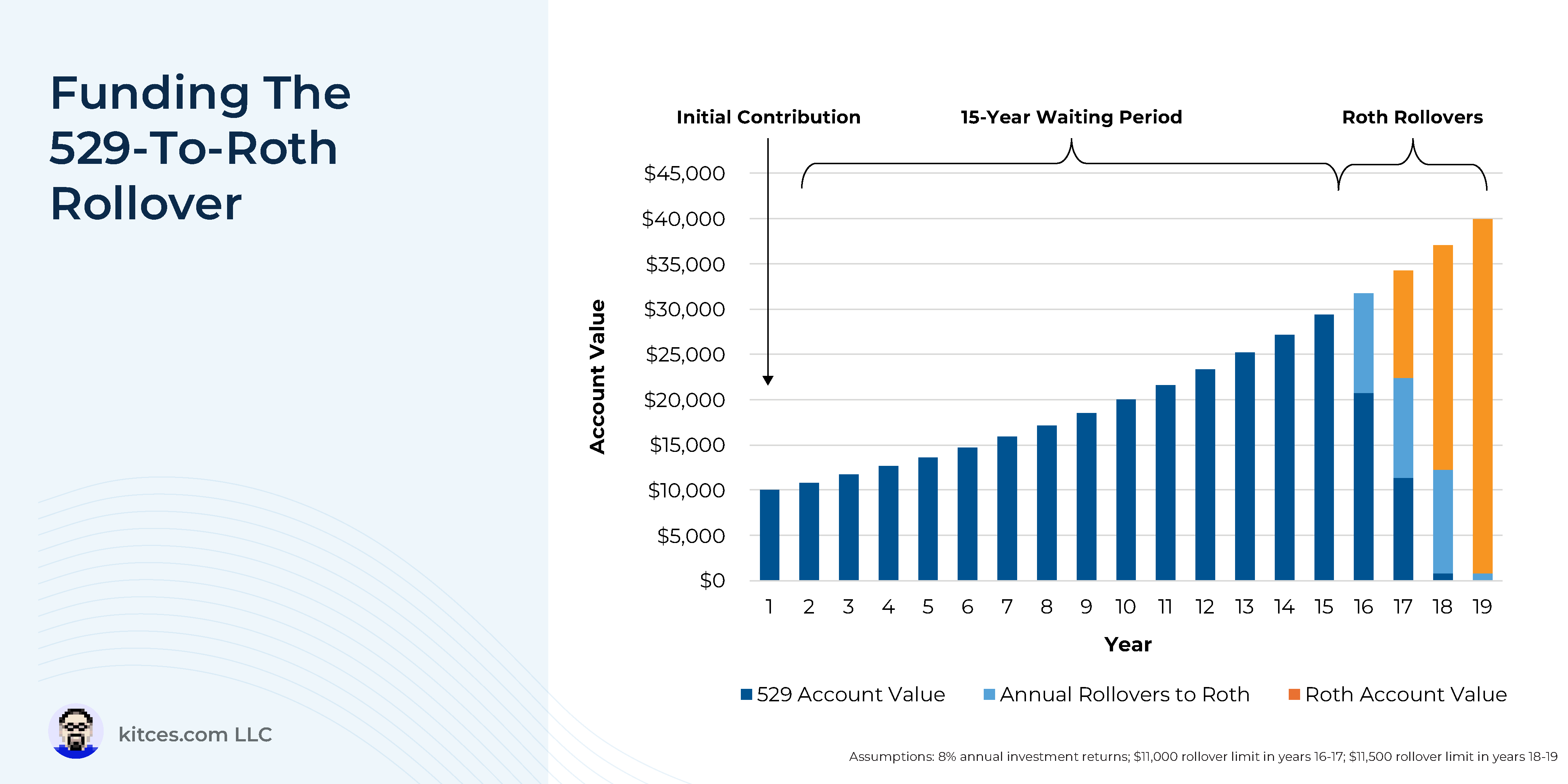

The Secure 2.0 Act passed in 2022 provided a new ‘escape valve’ for individuals who, for whatever reason, found themselves with more funds in their 529 plan than they could use on qualified higher education expenses. The new law created the ability for a 529 plan beneficiary to roll funds over tax-free from a 529 plan to a Roth IRA, subject to several key limitations: The 529 plan must have been maintained for at least 15 years, the amount of the rollover cannot exceed the IRA contribution limit for that year, the rollover must be made using funds that have been in the 529 plan for at least 5 years, and the maximum lifetime that a beneficiary can roll over in their lifetime is $35,000.

Because of the strict limitations on when and how the 529-to-Roth rollover can be done, it has limited usefulness as a planning tool beyond its intended purpose of giving individuals with overfunded 529 plans an opportunity to reallocate some of those funds tax-free towards their retirement savings. Similarly, the $35,000 lifetime rollover limit means that it can’t be used by parents or grandparents to gift huge amounts of tax-free dollars to their heirs, since anything beyond that lifetime limit would still need to either be used on qualified educational expenses or be subject to taxes and penalties as a non-qualified distribution.

Even so, 529-to-Roth rollovers can still be worth incorporating into college and estate planning as a way to gift beneficiaries the “option” of putting up to $35,000 towards their retirement savings. In other words, families who want to give their kids a head start on their career and life path (but don’t want to simply give no-strings-attached cash) can now consider 529 plans as a way to provide a boost not only to their education savings, but also to their retirement savings.

The key point is that while the new 529-to-Roth rollover rules may be limited in terms of how much wealth they can move into tax-free retirement funds, they can still provide real benefits – both in their intended purpose as an escape valve for people who can’t or won’t use all of the funds in their 529 plan for qualified education expense, and in the symbolic significance of contributing funds to a child or grandchild that can be used for education, retirement savings, or both!

{kind=link}