Ircon International Ltd – Key player in railway infrastructure

Incorporated in 1976 and headquartered in New Delhi, Ircon International Ltd. (IRCON) is a leading government construction company under the Ministry of Railways. It specializes in railway and highway construction, EHP sub-station engineering, and MRTS, with operations across India and abroad. IRCON has completed over 2,500 km of new and rehabilitated railway tracks and more than 400 infrastructure projects in India, along with 128 international projects in 25 countries, often in challenging environments.

Products and Services

- Railways: Construction and rehabilitation of railway lines, station buildings, bridges, tunnels, signalling networks, electrification, and rail coach factories.

- Highways: Highways and roads to international standards, funded by World Bank, Asian Development Bank, and Arab Fund etc.

- Others: Construction of bridges, flyovers, commercial and institutional buildings, airport terminals, hangars, and runways.

Subsidiaries: As of FY24, the company has 11 subsidiaries and 7 joint ventures.

Growth Strategies

- Navratna Status: Granted in FY24 following key achievements in project acquisition and financial performance.

- Ministry of Railways Linkage: Delivered over 400 infrastructure projects in India.

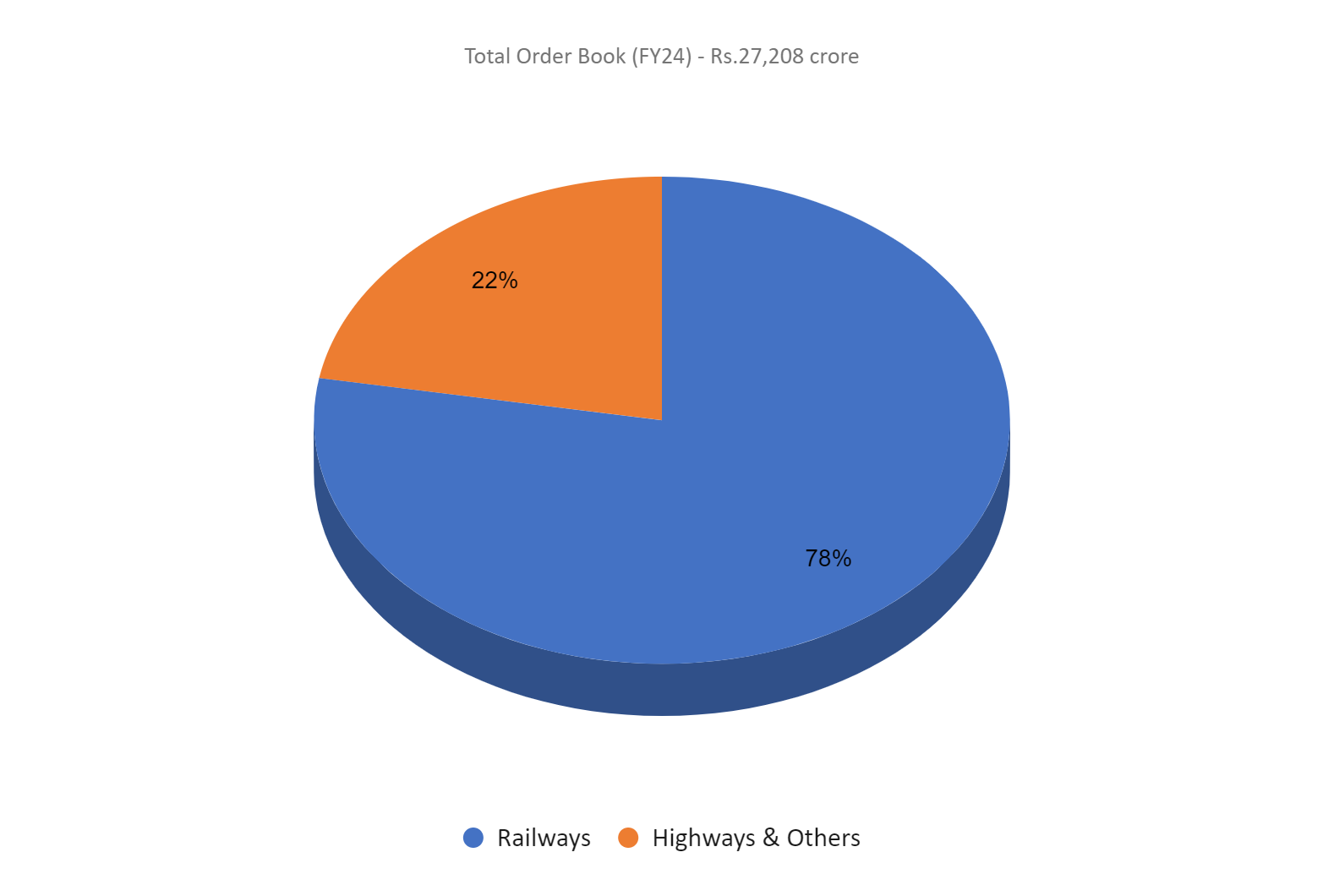

- Order Book: Stands at Rs. 27,208 crore as of March 31, 2024, to be executed over the next 2-3 years.

- Bullet Train Project: Secured a Rs. 5,200 crore contract from the Mumbai-Ahmedabad high-speed bullet train project, comprising 19-20% of the order book.

- Proven Execution Capabilities: Demonstrated in challenging terrains, including road projects in Myanmar and rail projects in Sivok.

- RVNL Ltd Order: Won a Rs. 750 crore contract in a joint venture agreement during FY25.

Financial Highlights

Q4FY24

- Revenue: Recorded at Rs. 3,743 crore, a decline of 1% compared to Rs. 3,781 crore in Q4FY23.

- Operating Profit: Improved by 15% from Rs. 370 crore in Q4FY23 to Rs. 424 crore in Q4FY24.

- Net Profit: Decreased by 4% to Rs. 247 crore compared to the same period last year, influenced by the tax benefit received in Q4FY23.

FY24

- Highest Ever Revenue and Net Profit: FY24 was one of the strongest years for IRCON.

- Revenue: Generated Rs. 12,871 crore, an increase of 20% compared to FY23.

- Operating Profit: Reached Rs. 1,510 crore, up by 35% YoY.

- Net Profit: Posted Rs. 930 crore, an increase of 22% YoY.

Financial Performance (FY21-24)

- Revenue and PAT CAGR: IRCON achieved a 32% and 34% CAGR in revenue and PAT over the period of 3 years (FY21-24).

- Average 3-Year ROE & ROCE: Approximately 15% and 16% respectively for FY21-24.

- Strong Balance Sheet: Maintains a robust debt-to-equity ratio of 0.44.

Industry outlook

- Global Ranking: India has the 4th largest railway system in the world, behind the US, Russia, and China.

- Freight Performance: Recorded monthly freight loading of 135.46 MT in June 2024, a 10.07% YoY improvement.

- Infrastructure Upgrades: Focus on electrification of lines, construction of new lines, and redevelopment of existing stations.

- Green Mission: Indian Railways has solarized more than 1000 stations.

Growth Drivers

- Capital Outlay: Budget allocates Rs. 2.52 lakh crore (US$ 30.3 billion) to the Ministry of Railways for advancements.

- FDI Policy: 100% FDI allowed in railway infrastructure under the automatic route.

- National Rail Plan (NRP) 2030: Indian Railways’ strategic plan to develop a modern railway system for India.

Competitive Advantage

Compared to the competitors like Rail Vikas Nigam Ltd, IRB Infrastructure Developers Ltd etc., IRCON is the most undervalued stock that has generated stable return ratios in line with the growth in the sales, indicating the company’s ability to generate better profits for the capital invested.

Outlook

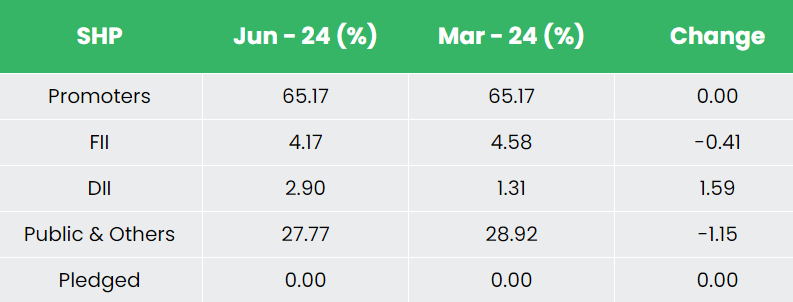

- Government Ownership: Strength from Government of India’s 65.17% ownership, providing stability and strategic support.

- Project Execution Capabilities: Proven track record in executing both domestic and international railway projects, enhancing credibility.

- Revenue Growth Strategy: Targeting to double revenue in the next 4-5 years, reflecting ambitious growth plans.

- Margin Challenges: Increasing the number of projects on a bidding basis may impact margins and earnings, necessitating careful monitoring.

Valuation

IRCON International Limited operates in a sector of national importance, ensuring stable revenue visibility for the future. However, the anticipated shift in project composition from nomination to bidding basis could potentially impact the order book and slow down earnings expansion. Despite these challenges, we recommend a BUY rating on the stock with a target price (TP) of Rs. 393, based on 37x FY26E EPS.

Risks

- Execution Delays: Delay in project tenders and approvals by predominantly government clients may impact turnover, typical of the construction industry.

- Moderate Profit Margins: Slowdown in margin expansion due to increasing competition and a shift from margin-accretive nomination projects to competitive bidding, limiting pricing power.

Note: Please note that this is not a recommendation and is intended only for educational purposes. So, kindly consult your financial advisor before investing.

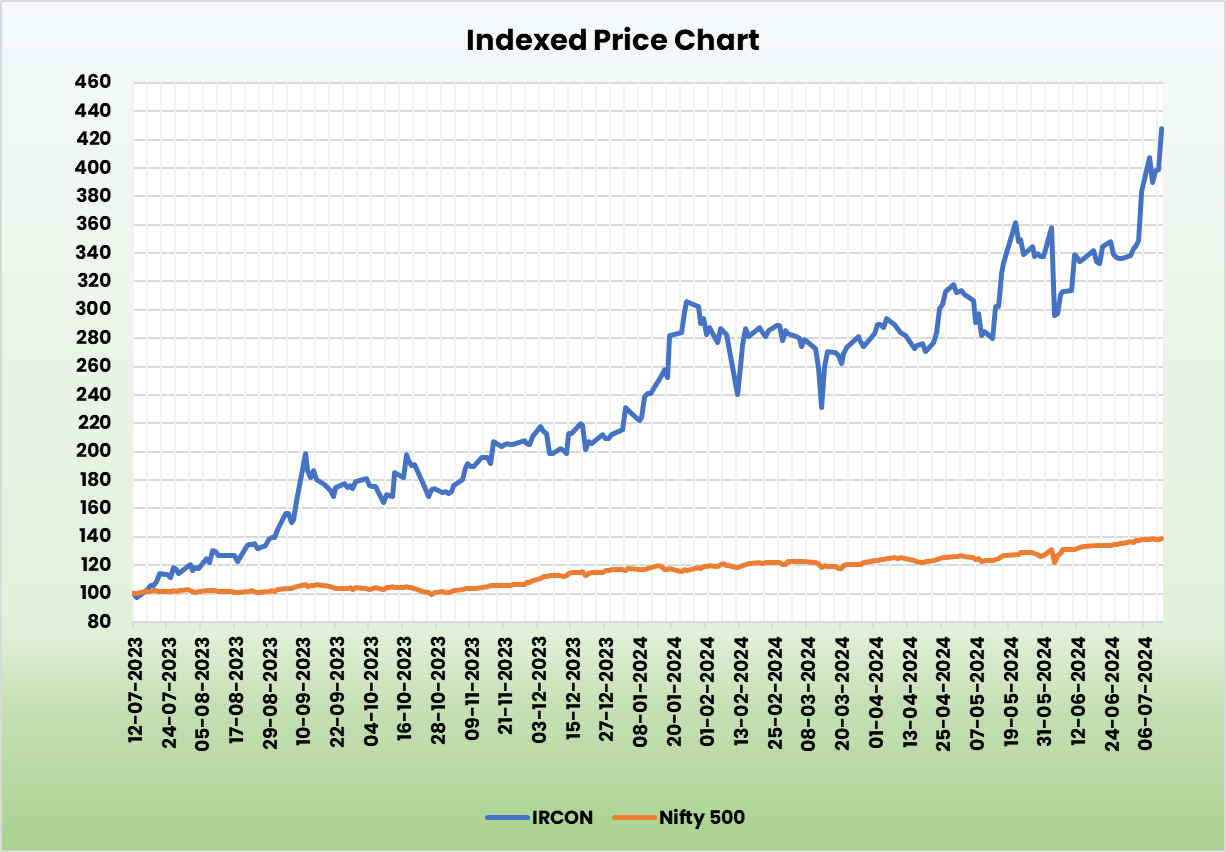

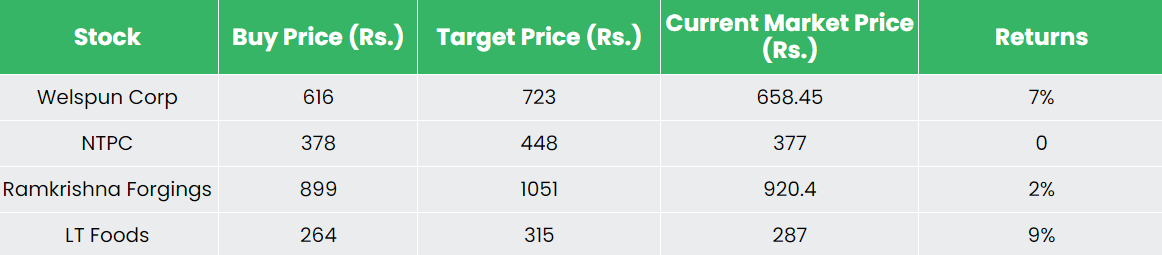

Recap of our previous recommendations (As on 12 July 2024)

Other articles you may like

{kind=link}

{kind=link}

{kind=link}

{kind=link}