It’s raining new fund offers.

Two new fund offers, however, caught my attention.

- Mirae Asset Nifty 200 Alpha 30 Index Fund of Fund

- Edelweiss Business Cycle Fund

The curious thing about these 2 funds is their focus on something called ‘factors’.

Factor based investing or smart beta portfolios have picked investor’s fancy in India recently.

You do remember the Nifty 200 Momentum 30 Index which has had a dream run of sorts. UTI MF has an older fund there, HDFC MF too launched its own in early 2024.

Can factor based investing or smart beta portfolios make a difference to your portfolio? Let’s find out.

What are “factors”?

Factors are like ingredients that mix, of which can make the food tastier or healthier.

A movie has factors like the script, cast, production quality and editing that can determine its success or failure.

In investing too, the role of factors is being recognised to determine a strategy’s success or failure.

Different factors for different results

There are several factors that can be identified in a portfolio but let me highlight a few for your reference.

a) Low Volatility – Stocks whose prices have lesser extremes or technically, low standard deviation.

b) Quality – Stocks that have shown better capital management, lower risks, debt and higher return on capital.

c) Value – Stocks that are undervalued with respect to the Price to Earnings, Price to Book and Dividend Yields.

d) Momentum – Trending stocks which have delivered better returns over the last 3, 6 or 12 months.

e) Alpha – Typically measured as excess return over a predefined benchmark.

f) Equal Weight – Example, having equal weight to Nifty 50 or Nifty 100 stocks will remove any size bias and allow each stock to contribute equally.

How factor based investing has started to become popular is reflected in the number of indices that are out there. Both the index providers affiliated to NSE and BSE are on a spree.

Some of these indices use standalone factors and others a combo of one or more factors.

Here are some examples:

- Nifty 200 Momentum 30 Fund

- Nifty 100 Low Volatility 30 Fund

- Nifty 200 Quality 30 Fund

- Nifty 200 Value 30 Fund

- Nifty 200 ALpha 30 Fund

- Nifty Alpha Low Volatility 30 Fund

- Nifty Quality Low Volatility 30 Fund

and many more. See a comprehensive list here

Quiz: Which one of the above list is a multi factor index?

Does factor based investing work?

Well, past studies and backtests show that there is a difference in outcomes when factor based portfolios are used in comparison to standard benchmarks from which these portfolios are created.

First of all, as mentioned earlier, a factor based approach is likely to offer a different portfolio than the regular index. How different? We will compare portfolios based on the 4 big factors.

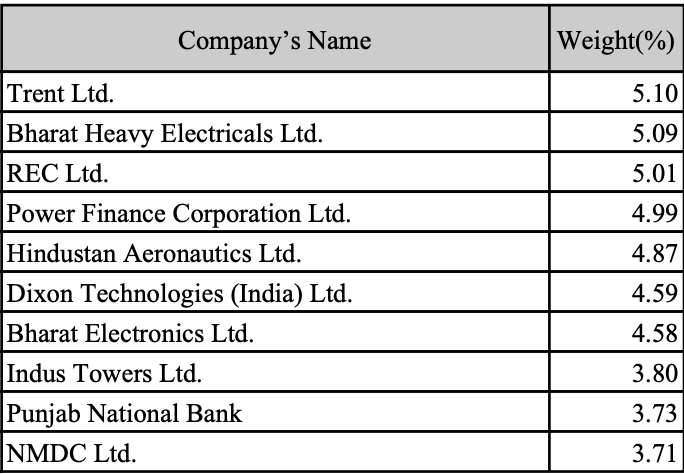

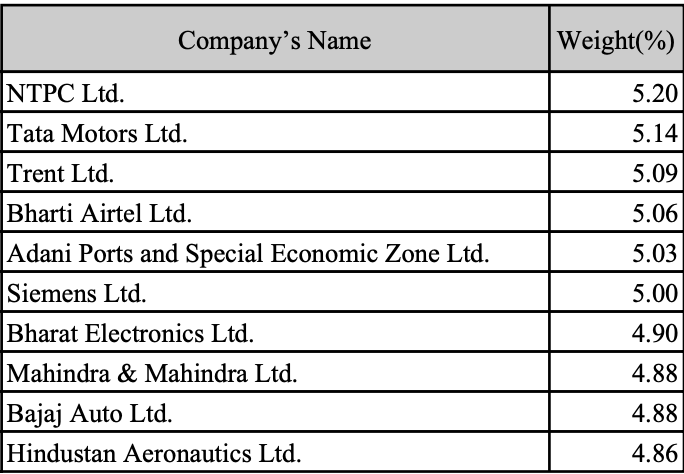

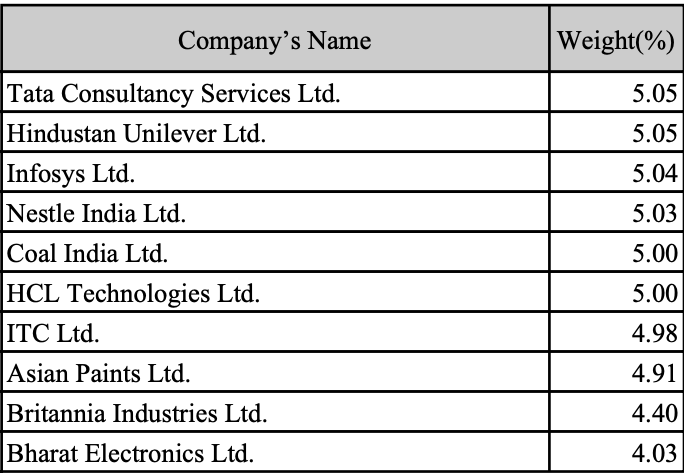

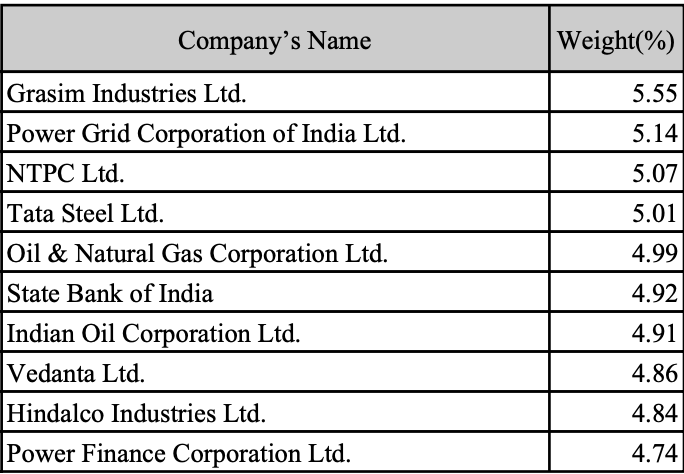

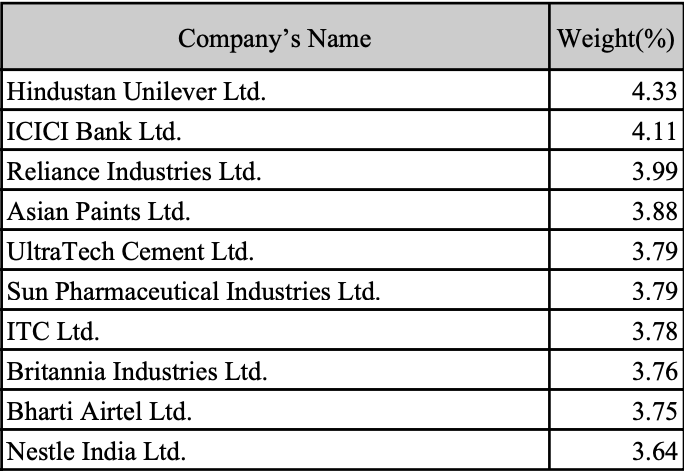

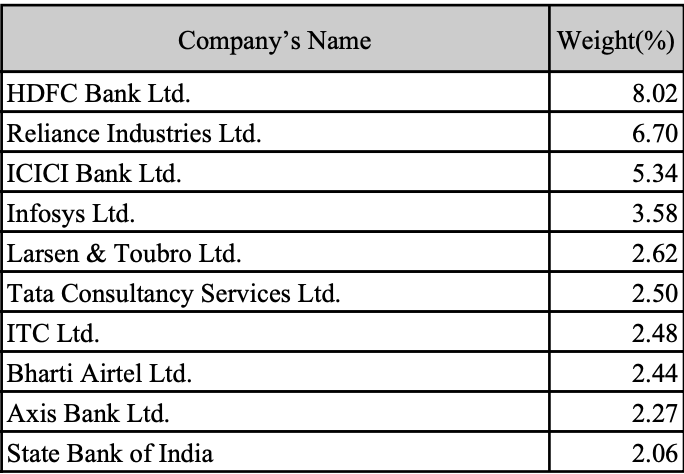

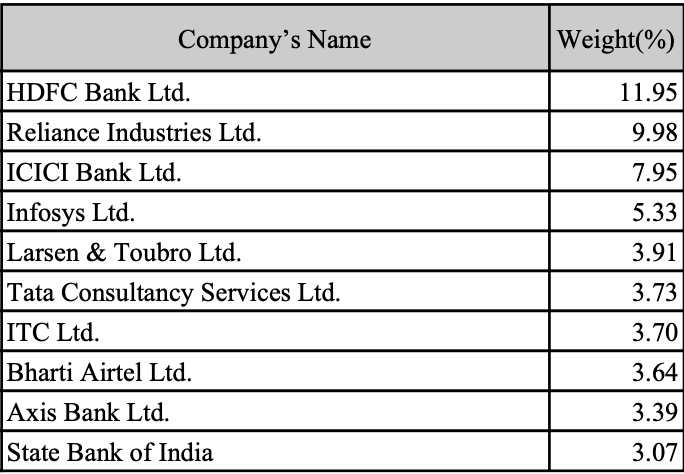

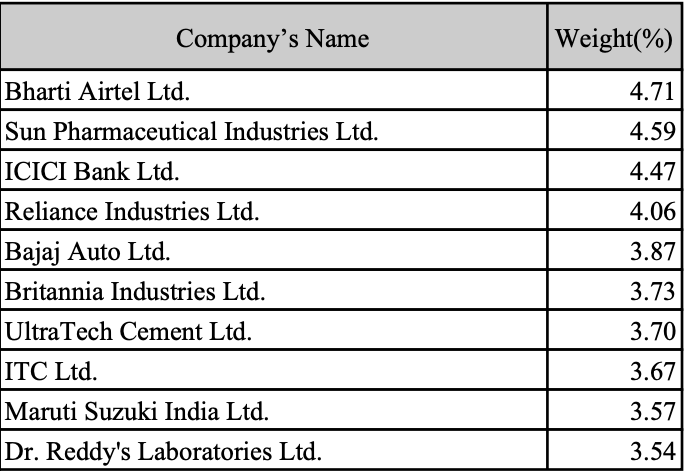

Top Holdings in various factor strategy indices as of June 28, 2024

Nifty 2oo Alpha 30 Index

Nifty 2oo Momentum 30 Index

Nifty 2oo Quality 30 Index

Nifty 2oo Value 30 Index

Nifty 1oo Low Volatility 30 Index

Nifty 2oo Index

Nifty 50 Index

Nifty Alpha Low Volatility 30 Index

Quiz: Which stock appears in both – Low Volatility as well as Quality indices?

How do these portfolios translate into outcomes?

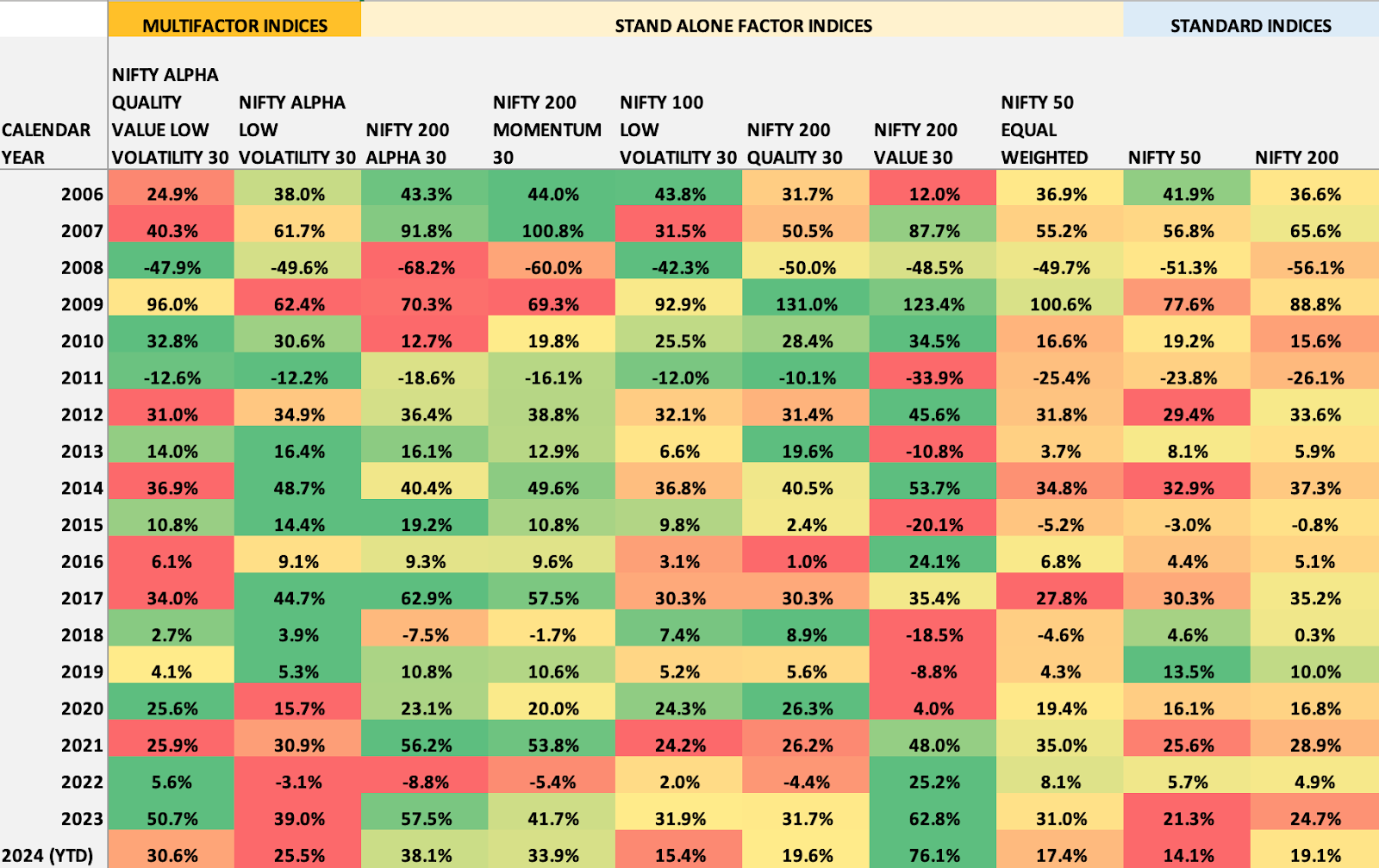

First of all let’s look at how various factors have behaved across calendar years.

We have data from April 1, 2005 till July 16, 2024 for total return index of each of the factor based indices. We used it to calculate calendar year returns as shown in image below.

Calendar Year Returns for various factor indices

Data Source: www.niftyindices.com, compiled by Unovest. Please note all the data shown below is back tested data on the index numbers. It does not account for expenses or any real world impact costs. It is past performance and has no relation to future results.

Just to give you an example let’s see how changing one factor can change the behaviour of the portfolio. In case of Nifty 50 and Nifty 50 Equal Weighted, the weighting criteria moved from free float market cap to equal weight. See the results.

For other factor based indices, the respective score for the factors is used as a weighting criteria for the stock in the portfolio.

What are the other observations?

The contribution of various factors change across cycles and years.

It appears that the value factor has quite a bit of extremes while alpha and momentum factors seem evergreen.

And yes, Nifty 200 Alpha 30 seems to have delivered over plain vanilla Nifty 200.

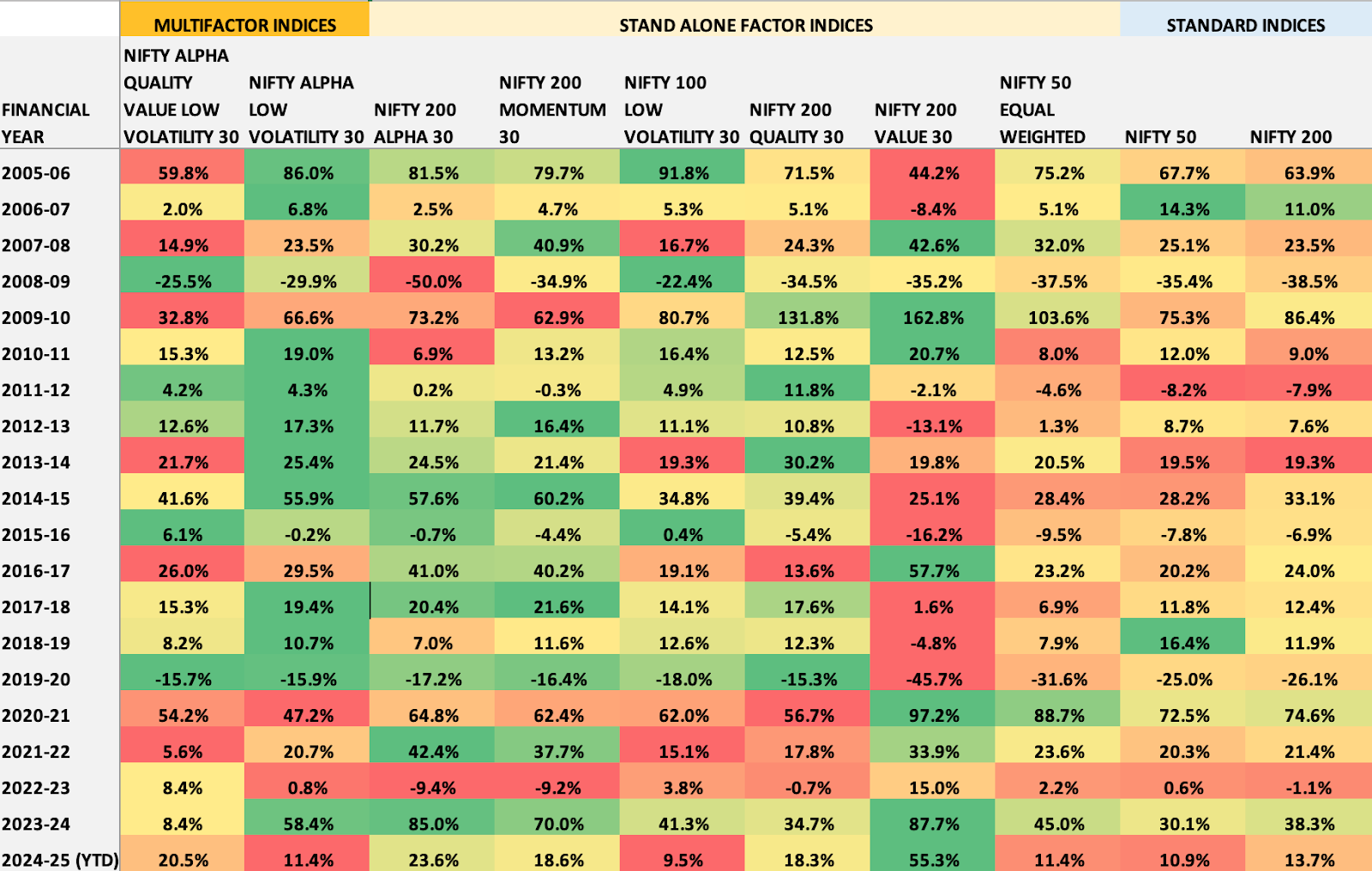

Let’s try a different point to point and see how it changes things.

Financial Year Returns for various factor indices

Data Source: www.niftyindices.com, compiled by Unovest

These numbers look different than the calendar year returns.

Do your observations change?

Well, value still is prone to extremes.

Nifty Equal Weight index has shown outperformance only post covid.

Within the group, the combination of Alpha and Low Volatility appears to be a more dependable option.

The question I ponder over is what happens to the plain vanilla Nifty index.

–

Now, we can go looking at each point to point data over the years – but that will be very cumbersome.

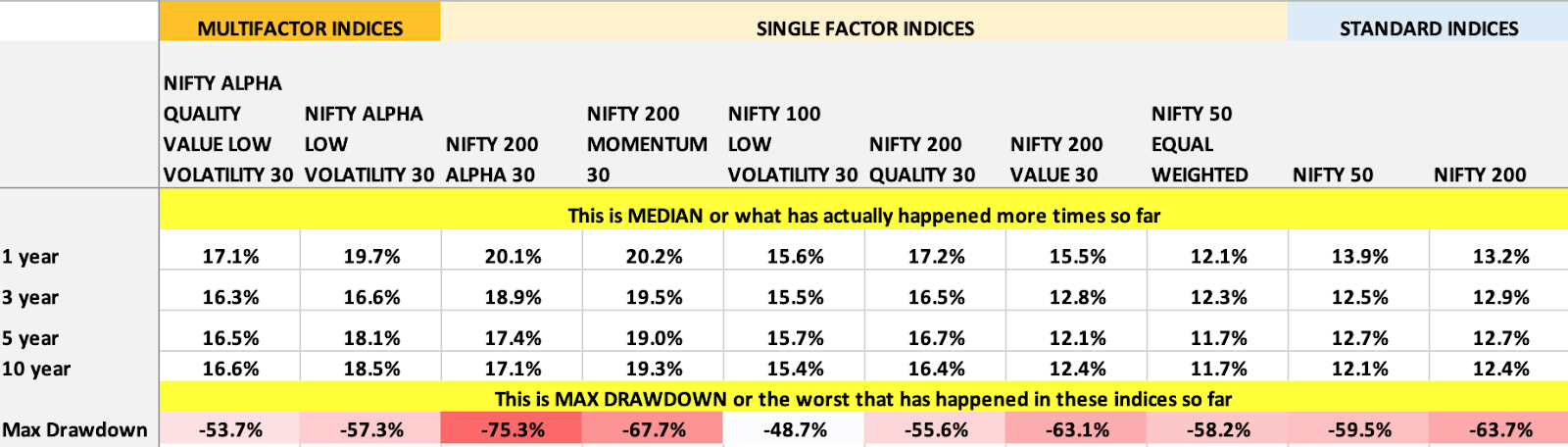

So, let’s go a step further and get rolling returns into the picture. We will calculate the median across this daily interval rolling series.

Rolling Returns summary for various factor indices

Rolling returns calculated with daily intervals. Data based on Total Price Index of respective indices from April 1, 2005 to July 16, 2024. Source: www.niftyindices.com, compiled by Unovest. For additional emphasis on the risks, we include drawdowns and potential losses.

This feels like a whole new frame of reference. The standard indices Nifty 50 and Nifty 200 seem to have been left far behind by factor based strategies (single or multi).

The Alpha factor doesn’t come without its price. It has a huge cost in terms of expected drawdown (this -75.3% above actually happened during the financial crisis in 2008).

Low Volatility is a stabilising factor for a portfolio or in multi factor strategies.

Well, with so much out there, one is definitely spoiled for alpha pick choices.

The question then is what do you want to focus on – More returns or less risk or a combination or just your style/factor preference?

–

Let’s circle back to the 2 funds we mentioned earlier.

The Alpha Factor – Mirae Nifty 200 Momentum 30 Alpha Fund of Funds

Mirae’s fund proposition is to have a fund of funds structure that will feed into its existing ETF (short for Exchange Traded Fund) Mirae Nifty 200 Momentum 30 Alpha ETF..

In this index, the alpha works with a specific formula or a measure called Jensen’s measure.

The measure is used to determine the stocks’ excess return (alpha) and use it rank the best stocks and assign them weightage too.

You see the position the portfolio is taking to deliver a different risk / return profile against, say, a Nifty 50.

The key thing to understand here is that the fund has changed its portfolio construction style and is now doing the following:

- Use a more concentrated portfolio of 30 stocks against Nifty 50’s, well, 50 stocks.

- Change the weightage of stocks and base it on the alpha score instead of market cap weight method used by standard indices such as Nifty 50. The per stock weightage is limited to 5% or thereabouts.

- The universe of stocks is bigger – Nifty 200 stocks against the Nifty 50

One can question as to why compare it with Nifty 50 in sales presentation and yes, it is not the perfect comparison but you need to beat something.

The fund did better compared to the standard index.

Don’t remember? Go back to the tables shown earlier.

Multi Factor magic – The Edelweiss Business Cycle fund?

This fund proposes to take a multi factor approach in a more broad based stock universe of 300 stocks. Its ‘proprietary model’ will pick stocks based on a combination of value, growth, quality and momentum factors and use it for sector rotation based on a set of rules.

They really had me confused about factors and sectors.

The portfolio will have about 60 stocks – the number divided equally between large cap and small/mid cap.

This is an actively managed fund and not a passive like the Mirae Alpha fund.

But everyone is looking for one thing – MORE.

Also know that most of the mutual fund schemes are designed to attract more assets and as they attract more assets they start to resemble the market, for various reasons. Over time, their outcomes may not be so different from the market itself.

So, if you are investing in a fund which is hugely popular or has a large number of stocks, think if it can still do the things which helped make it popular and/or a top ranker in the first place.

Should you invest in factor indices / smart beta strategies?

Human nature poses a big problem to investing success. Everytime there is a new option on the horizon we want to latch on to it in the hope that this is the one that will do the magic.

But by the time you want to pick that factor up, it’s time is done for then and you feel disappointed.

I believe that some of the more popular factor based funds today will disappoint in the near future.

On the contrary, if you were really interested in a factor based portfolio and I were to tell you to pick a Quality and Low Volatility factor?

What I am trying to tell you is that don’t get caught up in the same age old circus of chasing returns.

Factors in a way are a simple way to work with your investor type. If you are a value investor, a value factor based fund / portfolio, gives you the vehicle to ride your conviction.

If you think momentum is the way to go for years (even with setbacks in between), there’s the factor portfolio for you.

Or, if this is too much to ask, then allocate between factors and keep rebalancing regularly.

Factor / smart beta strategies may have their role but only if you are willing to stick to the path and let time do its part.

You have to subject yourself to rules to keep the monkey in the mind from doing stupid things.

The only alpha, in that case, is to those you pay your fee and taxes to.

—

What is your success factor going to be?

–

Frankly, you would be an exception if you can do it yourself. All other smart people, who have accepted that it is beyond them, are working with an advisor.

The advisor’s role is to help stick to a path to compound your wealth which leads to not just a worry free retirement but more meaning too. That’s an alpha worth chasing.

–

If you wish to know more about Nifty Indices and their methodology, check out this link

{kind=link}