Mankind Pharma Ltd – Building a Healthier Bharat

Incorporated in 1995 and headquartered in New Delhi, Mankind Pharma Ltd. develops, manufactures, and markets a wide range of pharmaceutical formulations across acute and chronic therapeutic areas, as well as consumer healthcare products. For the past seven years, it has been India’s leading pharmaceutical company by prescription volume. The company offers various dosage forms, including tablets, capsules, syrups, and over-the-counter products. Initially focused on rural areas, Mankind Pharma expanded into peri-urban, metropolitan, and Tier-1 cities. It operates 30 manufacturing facilities, with 75% of production in-house, and six R&D centers that have developed 23 brand families.

Products and Services

Mankind Pharma’s offerings fall into two main segments:

- Domestic Pharmaceutical: A broad range of formulations for acute and chronic conditions, including anti-infectives, cardiovascular, gastrointestinal, anti-diabetic, neuro/CNS, vitamins/minerals/nutrients, and respiratory therapies.

- Consumer Healthcare: Established brands in pregnancy detection, oral contraceptives, condoms, antacids, vitamins, and anti-acne products. Popular brands include Prega News, Manforce, Unwanted Kit, and Gas-O-Fast.

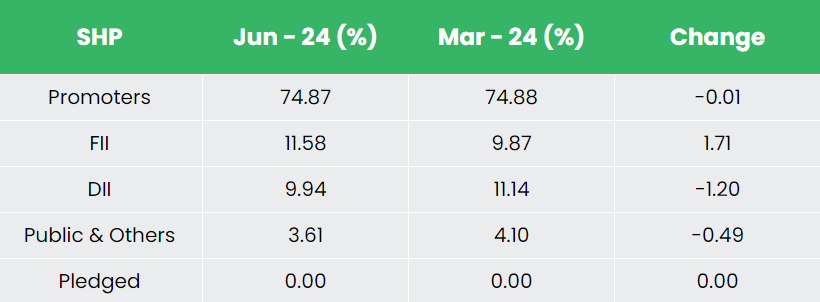

Subsidiaries: As of FY24, the company has 34 subsidiaries, 3 joint ventures and 5 associates.

Growth Strategies

- BSV Acquisition: Acquiring Bharat Serums and Vaccines for Rs.13,630 crore to expand in women’s health and critical care.

- Chronic Growth: Chronic segment grew by 14%, driven by 21% growth in anti-diabetic and 15% in cardiac therapies.

- Market Share Gain: Increased market share to 5.1% in cardiac and 4.4% in anti-diabetes therapies.

- OTC Leadership: Leading OTC brands like Prega News and Manforce continue to dominate their markets.

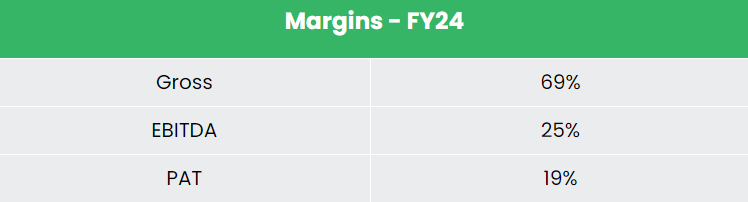

Financial Performance

Q1FY25

- Revenue: Rs.2,893 crore in Q1FY25, up 12% from Rs.2,579 crore in Q1FY24.

- Operating Profit: Rs.686 crore, a 5% YoY growth from Rs.655 crore.

- Net Profit: Rs.543 crore, increasing 10% YoY from Rs.494 crore.

- Export Revenue: Grew by 62% YoY.

- Cash Flow from Operations: Rs.546 crore.

FY24

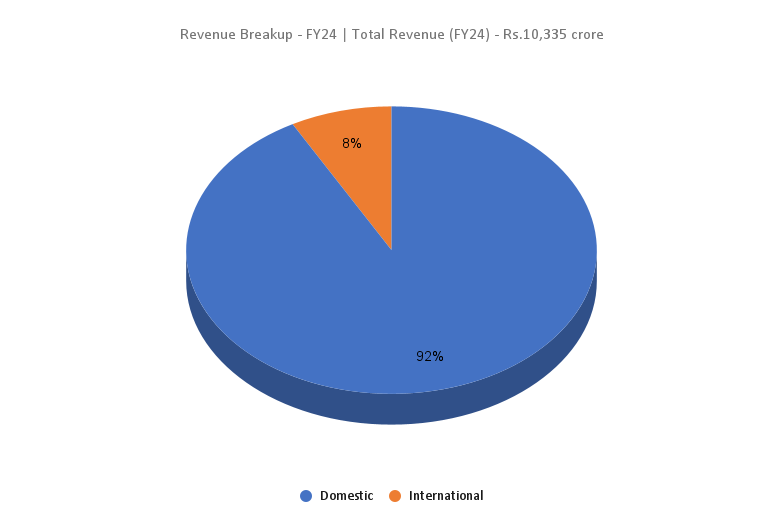

- Revenue: Rs.10,335 crore in FY24, up 18% from FY23.

- Operating Profit: Rs.2,550 crore, a 34% YoY increase.

- Net Profit: Rs.1,942 crore, up 48% YoY.

- New Facility: Inaugurated India’s first fully integrated Dydrogesterone facility in Udaipur.

Financial Performance (FY21-24)

- Revenue and PAT CAGR: 18% and 14% respectively over the past 3 years (FY21-FY24).

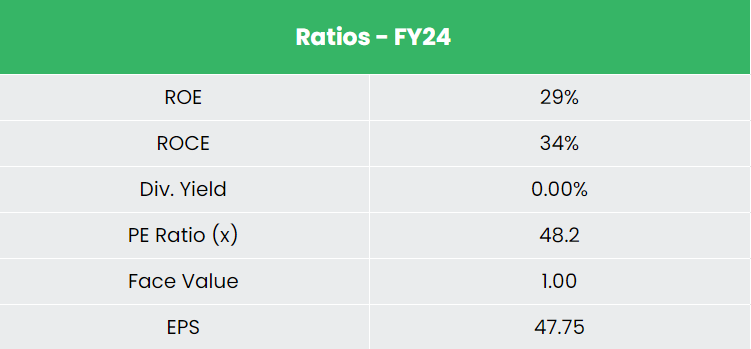

- ROE and ROCE: Average of 22% and 27% over the past 3 years.

- Capital Structure: Strong, with a debt-to-equity ratio of 0.02.

Industry outlook

- Industry Size: The Indian pharmaceutical industry is the third largest globally by volume and is expected to reach US$130 billion by 2030, growing at a CAGR of over 10%.

- Growth Drivers: Increased healthcare spending, ageing population, population growth, rise in lifestyle diseases, and greater awareness of quality healthcare.

- Global Preference: Indian medicines are favored worldwide for their low price and high quality, earning India the title of ‘Pharmacy of the World.’

- Regulatory Presence: India has the highest number of FDA-approved plants outside the US.

- Mergers and Acquisitions: Expected to drive industry progress and create opportunities for expanding product offerings and meeting diverse patient needs.

Growth Drivers

- FDI Policies: Up to 100% FDI allowed through the automatic route for Greenfield pharmaceutical projects; up to 74% for Brownfield projects, with higher stakes requiring government approval.

- Government Initiatives: Programs like Pradhan Mantri Bhartiya Jan Aushadhi Pariyojana and Ayushman Bharat enhance the accessibility of affordable medicines.

- ‘Make in India’ Initiative: Supported by the Production Linked Incentives (PLI) scheme to boost domestic manufacturing and promote indigenous products.

Competitive Advantage

Mankind Pharma is generating higher returns from invested capital compared to competitors like Lupin Ltd and Aurobindo Pharma Ltd. The company’s consistent revenue growth reflects its effective financial allocation strategies and prudent management.

Outlook

- Women’s Health and Fertility: With lifestyle changes and rising chronic conditions, this segment offers significant potential. Mankind aims to lead the gynaecology-fertility market through its acquisition of BSV, a high-entry-barrier business with minimal competition.

- Business Strategy: Mankind’s approach—starting with rural markets and expanding to metro cities while diversifying from chronic to consumer health care products—looks promising.

- New Launches: The company introduced Inclisiran, a premium injection in-licensed from Novartis costing Rs. 1 lakh, and Ova News, expected to grow similarly to Prega News.

- Development Pipeline: As of FY24, Mankind has 109 new molecules in development.

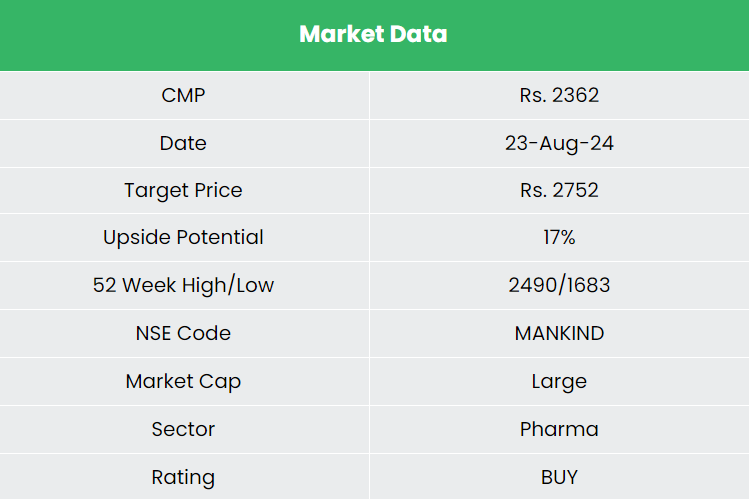

Valuation

Mankind’s strategy of expanding into high-entry-barrier segments with strong pricing power and market share is expected to drive robust growth. We recommend a BUY rating with a target price (TP) of Rs.2,752, representing 43x FY26E EPS.

Risks

- Regulatory Risk: The industry faces significant regulatory scrutiny, including potential limitations or bans on products by agencies like the USFDA, which could impact revenue and operations.

- Patent Risk: The company may face challenges in defending patents or managing third-party agreements, potentially affecting its business operations.

Note: Please note that this is not a recommendation and is intended only for educational purposes. So, kindly consult your financial advisor before investing.

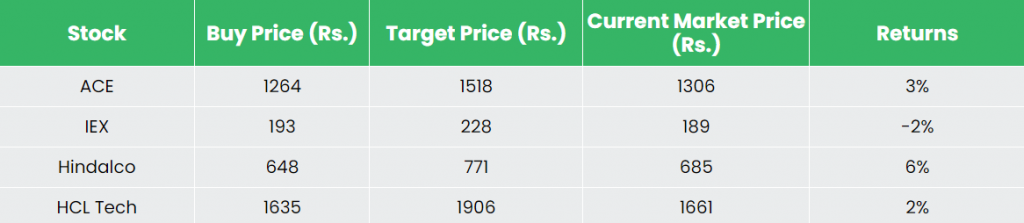

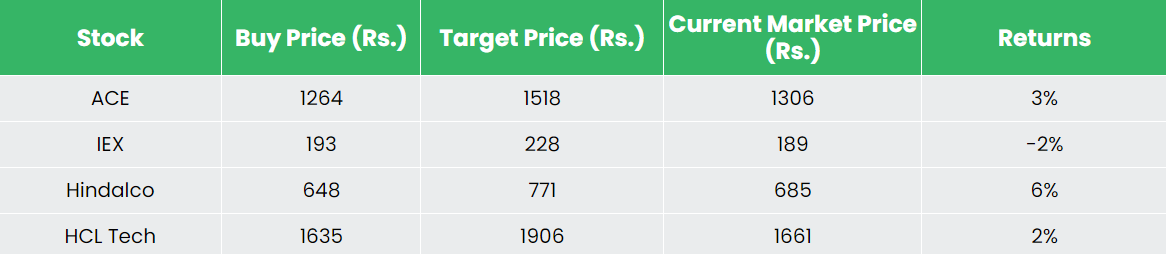

Recap of our previous recommendations (As on 23 August 2024)

Action Construction Equipment Ltd

Other articles you may like

{kind=link}

{kind=link}

{kind=link}

{kind=link}