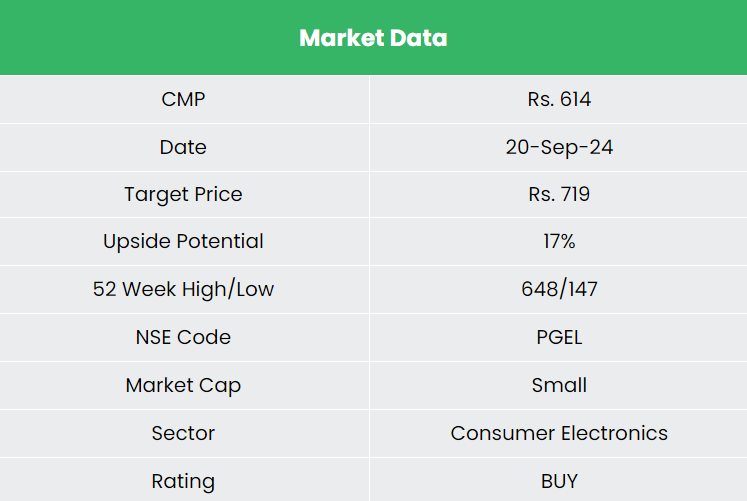

PG Electroplast Ltd – Expertise meets innovation

PG Electroplast Limited (PGEL), a flagship of PG Group, is a leading electronic manufacturing service provider in India. Founded in 2003 and based in Greater Noida, PGEL specializes in ODM, OEM, contract manufacturing, and plastic molding. The company offers comprehensive solutions from design to production, focusing on room air conditioners, washing machines, and plastic molding. With 10 manufacturing units and over 3,500 employees, PGEL has served 107 clients as of FY24 including Astral, Blue Star, Godrej, Whirlpool, etc.

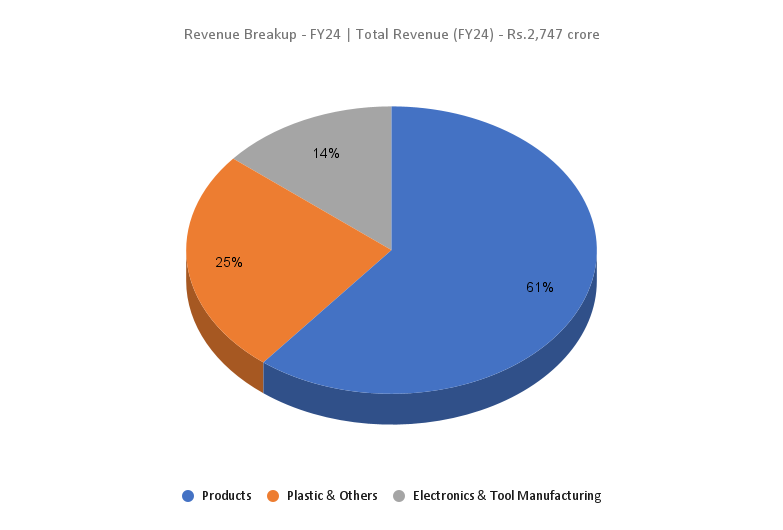

Products and Services

The products and services offered by the company can be categorized as below:

- Products – Includes RAC (indoor units, outdoor units), window air conditioners, washing machines, air coolers & televisions.

- Plastics – Plastic moulding solutions for sanitaryware, consumer durables, automotive, consumer electronics, etc.

- Electronics – Electronics manufacturing comprising televisions and PCB assemblies.

- Tool manufacturing – Tool manufacturing for consumer durables, sanitaryware, automotive, etc.

Subsidiaries: As of FY24, the company has 2 subsidiaries and 1 joint venture.

Growth Strategies

- PG Electroplast (PGEL) began operations at a new AC manufacturing facility in Rajasthan, with an annual capacity of 360,000 split ACs and 250,000 window ACs, making it the second-largest ODM for RACs in India.

- The company plans to further expand AC capacity and is setting up a new integrated unit, alongside a greenfield washing machine facility in Greater Noida.

- PGEL has allocated Rs.370-380 crore for FY25 capex, including Rs.125-130 crore for RACs, Rs.35-40 crore for washing machines, and Rs.180 crore for land and buildings.

- The “Products Segment” contributed 75% of Q1FY25 revenue, driven by room ACs, washing machines, and air coolers, with a 60% growth target for FY25 to Rs.2,650 crore.

- PGEL aims to raise its monthly production capacity for indoor and outdoor AC units and double the capacity of window ACs and washing machines.

Financial Performance

Q1FY25

- Record-high quarterly sales and profits in Q1FY25.

- Revenue grew 95% YoY to Rs.1,321 crore (vs. Rs.678 crore in Q1FY24).

- RAC business increased by 130%; the washing machine segment rose by 72%.

- EBITDA surged 101% YoY to Rs.135 crore (vs. Rs.67 crore).

- Net profit increased 151% YoY to Rs.85 crore (vs. Rs.34 crore).

FY24

- FY24 revenue reached Rs.2,747 crore, up 27% YoY.

- Product business contributed 60.7% to overall sales.

- Operating profit increased by 53% YoY to Rs.275 crore.

- Net profit grew 78% YoY to Rs.137 crore.

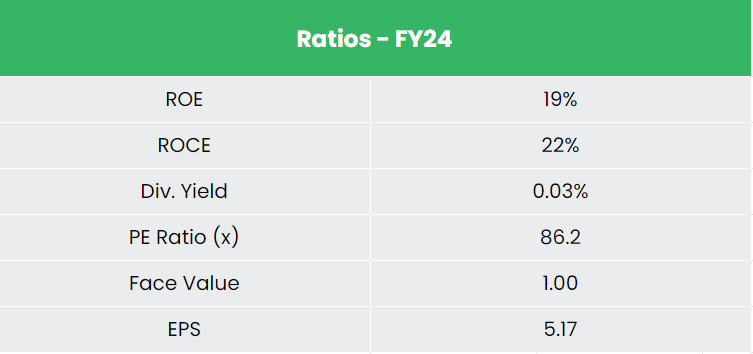

Financial Performance (FY21-24)

- Revenue and PAT CAGR of 57% and 125% from FY 21-24.

- Average 3-year ROE of 19% and ROCE of 16%.

- Debt-to-equity ratio stands at 0.42.

Industry outlook

- India’s electronics ecosystem is experiencing rapid growth across various sectors like mobiles, telecom, and auto electronics.

- Key growth drivers include a rising middle class, increasing disposable income, and growing consumer demand.

- The government projects the Indian electronics manufacturing sector to reach US$ 500 billion by 2030.

- Air conditioner market size is expected to grow from 65 lakh units in 2019 to 165 lakh units by 2025.

- The Indian washing appliances market is projected to grow from US$ 3.76 billion to US$ 5.43 billion by 2029, with a CAGR of 7.65%.

- The white goods market is expected to exceed US$ 21 billion by 2025, expanding at a CAGR of 11%. Domestic manufacturing contributes around US$ 4.6 billion annually.

Growth Drivers

- 100% FDI permitted in electronics hardware manufacturing.

- The Indian government distributed Rs.79 crore (US$ 9.51 million) in fiscal incentives under the PLI scheme for white goods in Q4 FY24.

- Key government initiatives like “Digital India” and “Make in India” have streamlined the process of setting up manufacturing units in India.

Competitive Advantage

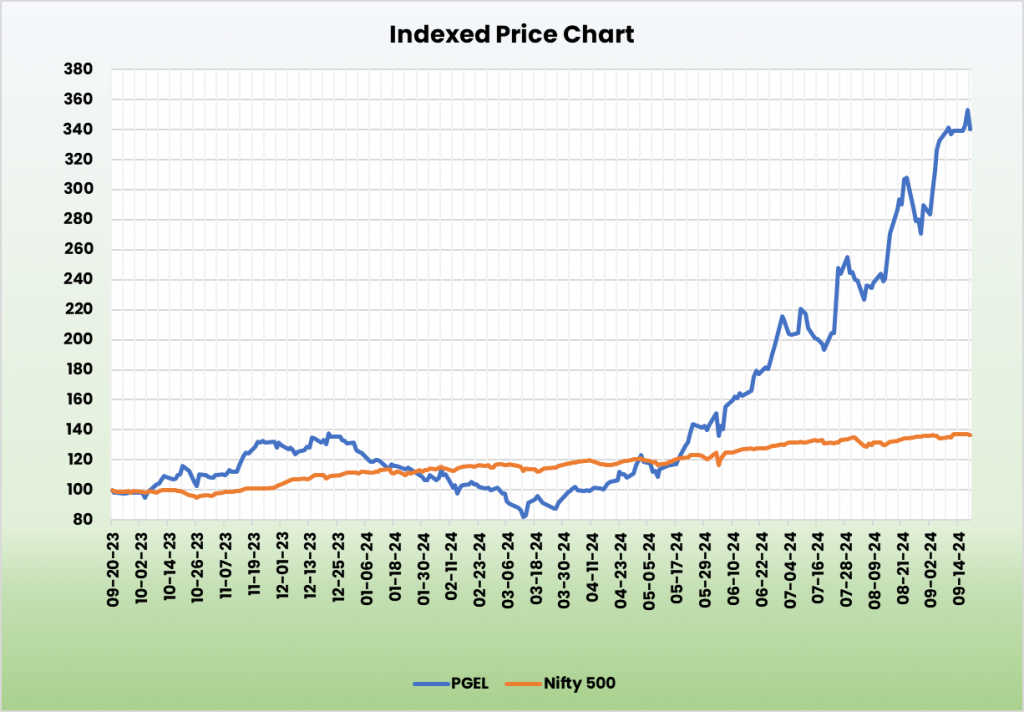

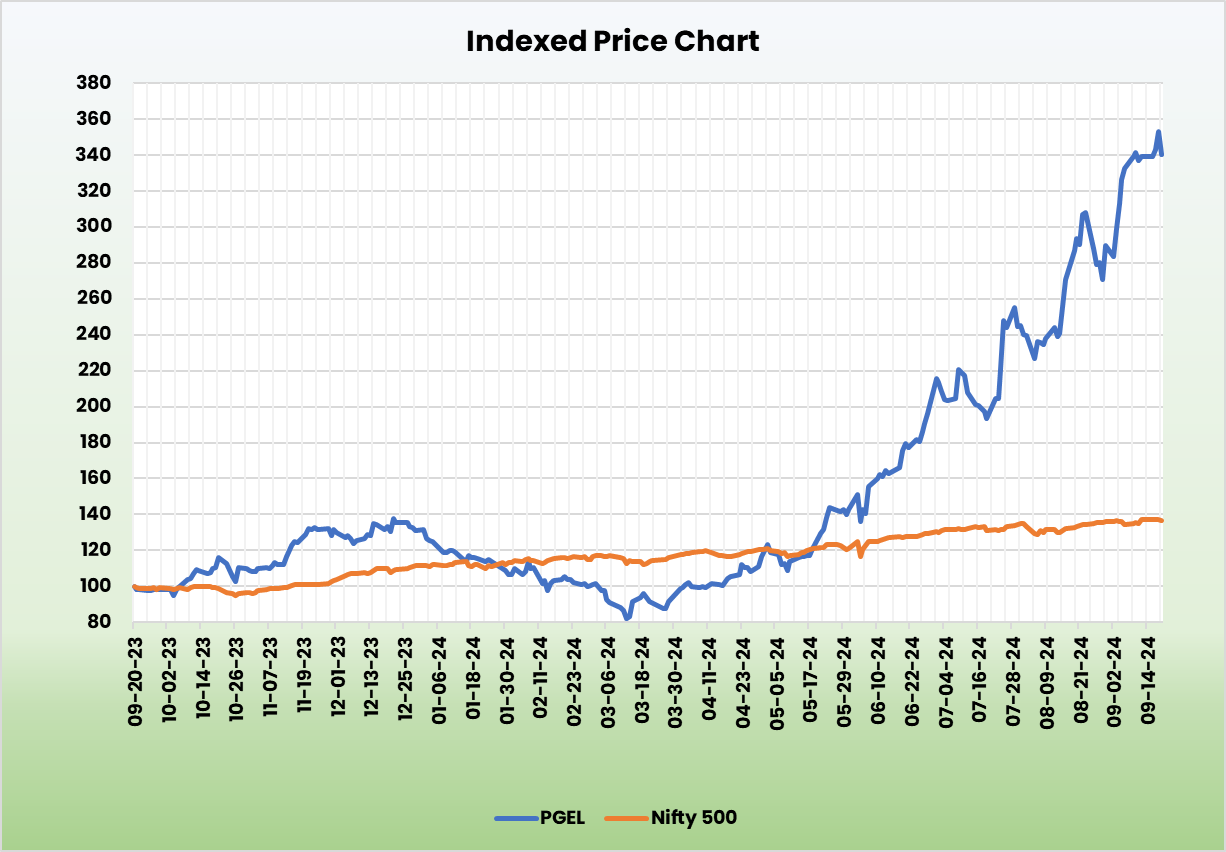

PGEL stands out as the most undervalued stock compared to competitors like Dixon Technologies and Amber Enterprises. Despite its lower valuation, PGEL offers healthy returns on capital employed and demonstrates robust sales growth, making it a strong player in the electronics manufacturing sector.

Outlook

- PGEL aims to be a global leader in electronics manufacturing for consumer durables and electronics.

- Formed a joint venture, Goodworth Electronics Limited, in FY24 to boost its TV and hardware business.

- Revised FY25 operating revenue guidance to Rs.3,650 crore for PGEL and Rs.600 crore for the JV, totaling Rs.4,250 crore—up 55% from FY24.

- Projected net profit of Rs.216 crore in FY25, representing a 58% increase YoY.

- Expects Rs.36 crore from PLI and state incentives in FY25 and is exploring participation in PLI 2.0 for white goods and PLI for IT & Hardware.

Valuation

PGEL’s expansion strategies and the management’s revised upward guidance, we remain positive on the company’s future growth prospects. We recommend a BUY rating in the stock with the target price (TP) of Rs.719, 69x FY26E EPS.

Risks

- Seasonality Risk: Unfavorable summer weather may weaken demand for room air conditioners (RACs).

- Outsourcing vs Insourcing: Increasing in-house manufacturing by OEMs could pressure the company’s order book.

Note: Please note that this is not a recommendation and is intended only for educational purposes. So, kindly consult your financial advisor before investing.

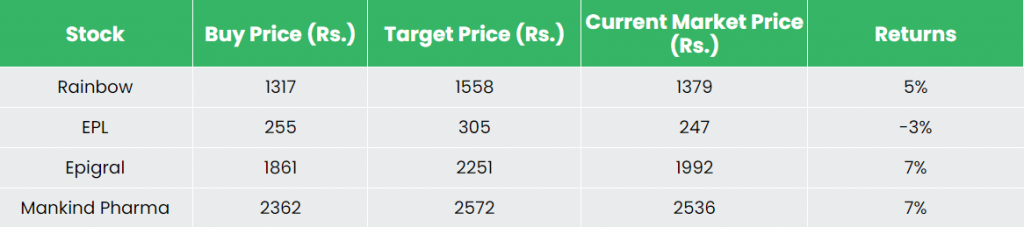

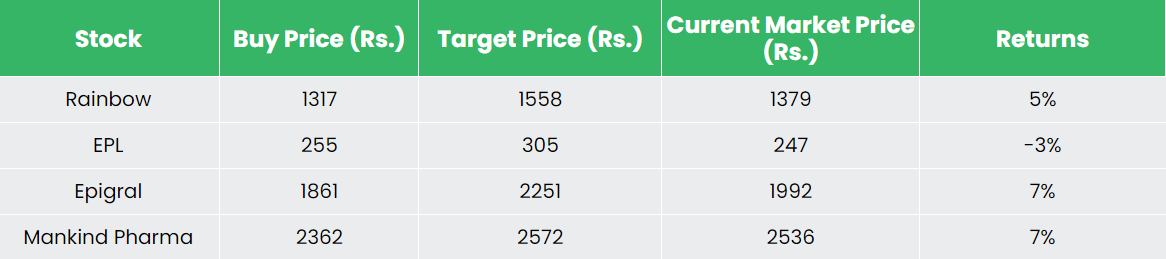

Recap of our previous recommendations (As on 20 September 2024)

Rainbow Children’s Medicare Ltd

Other articles you may like

{kind=link}

{kind=link}

{kind=link}

{kind=link}