Given the frequent news headlines on the (un)sustainability of the Social Security system, many working-age financial advisory clients might harbor doubts about receiving their full estimated Social Security benefits (and many current Social Security recipients might be concerned that they will not continue to receive their full benefits throughout the remainder of their lives). In this environment, financial advisors have the opportunity to add value for their clients not only by giving a clear explanation about the current status of Social Security and the potential legislative changes that could improve its solvency, but also by modeling what (realistic) changes would mean for their clients’ financial plans.

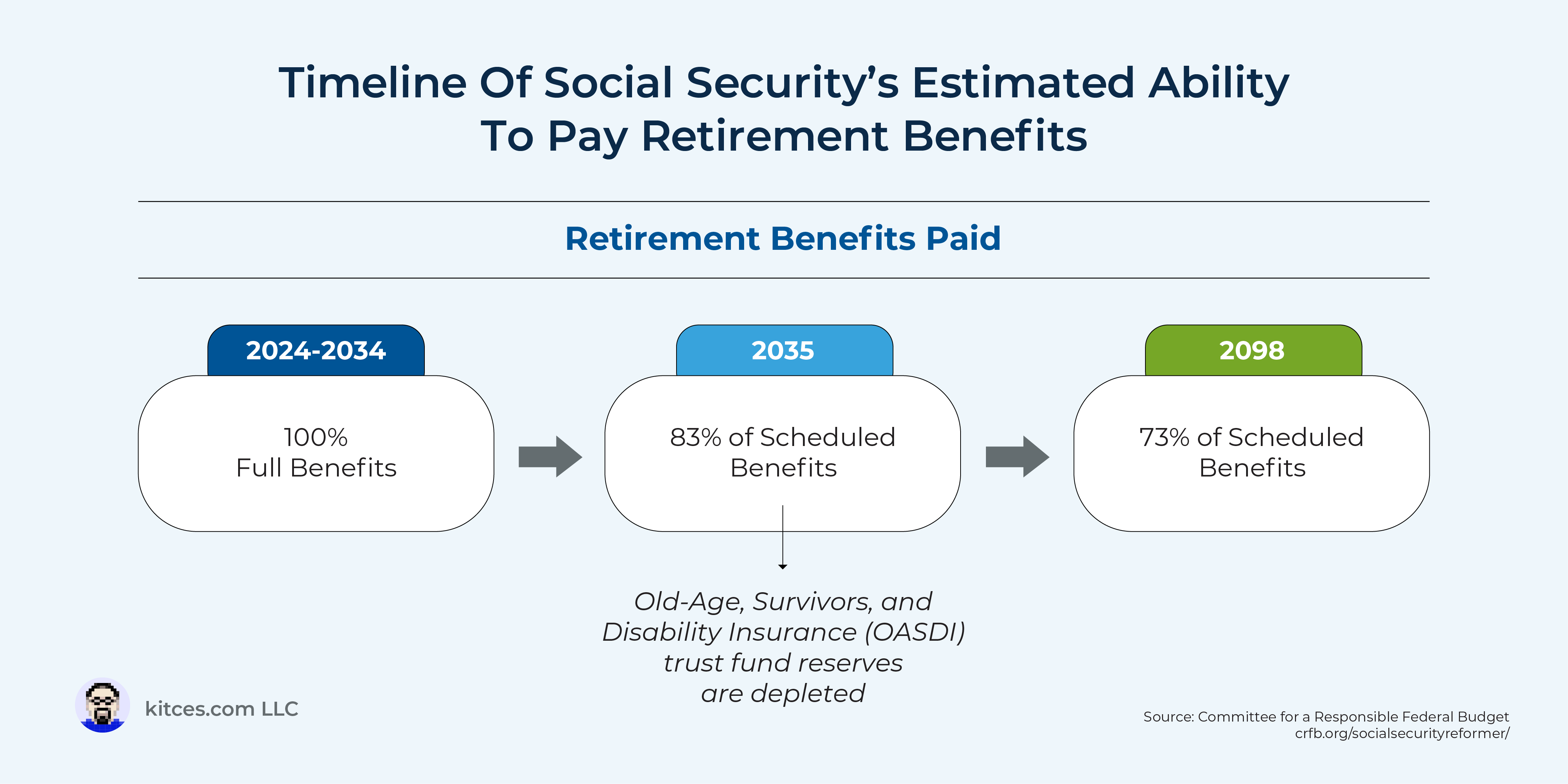

To start, while the state of Social Security’s trust fund reserves often receives significant media attention, in reality, the bulk of funding for paying out Social Security benefits comes from Federal Insurance Contributions Act (FICA) taxes, more commonly known as payroll taxes (with workers and their employers each paying 6.2% on up to $168,600 of income in 2024 for the Social Security portion of FICA). Which means that even if the trust fund reserves were to become depleted (currently estimated to occur in 2035), the system would continue to pay the majority of benefits that are simply covered by the ongoing receipt of significant payroll tax revenue. In fact, according to the latest annual report of the board of trustees of the Social Security trust funds, Social Security would still be able to pay 83% of scheduled benefits in 2035 when it is expected to be depleted, though this figure would decline to 73% of scheduled benefits by 2098. Which might come as a surprise to clients who assume that the exhaustion of trust fund reserves would mean that no (or very little) benefits would be paid!

Nonetheless, given the disruption that a reduction of benefits would cause recipients of Social Security retirement benefits (particularly those who rely on such benefits for a significant percentage of their retirement income), policymakers have an incentive to enact measures that would allow the system to continue paying out full benefits for decades to come. Such options include single-policy solutions that would wipe out the entire 75-year shortfall (e.g., the board of trustees report estimates that a 3.33 percentage point increase in the payroll tax or a 20.8% reduction in benefits would cover the gap) or a (perhaps more politically feasible) combination of policies that address system revenues and/or costs (e.g., raising the payroll tax wage cap or increasing the Full Retirement Age) that would close the funding gap.

Ultimately, the key point is that financial advisors have the opportunity to add value for their clients by providing context on the state of Social Security (e.g., even if the trust funds are exhausted, the system would still be able to pay out the majority of scheduled benefits) and potential legislative fixes (which, depending on the legislation passed, might not be as severe as some clients assume), as well as leveraging financial planning tools to show the impact of the possible trust fund exhaustion and/or potential policy actions on each client’s financial plan (both in dollar terms and how it changes the probability of success of their plan). Which, together, could provide clients with a more realistic picture of what changes to Social Security could mean for their unique situation!

{kind=link}