Gifting is a common planning topic discussed between advisors and clients – often raising questions about which gifts are taxable, need to be reported to the IRS, or may be exempt from reporting altogether. The rules around gifting are nuanced and can create confusion for clients, but advisors with a clear understanding of gifting strategies can guide them toward informed decisions.

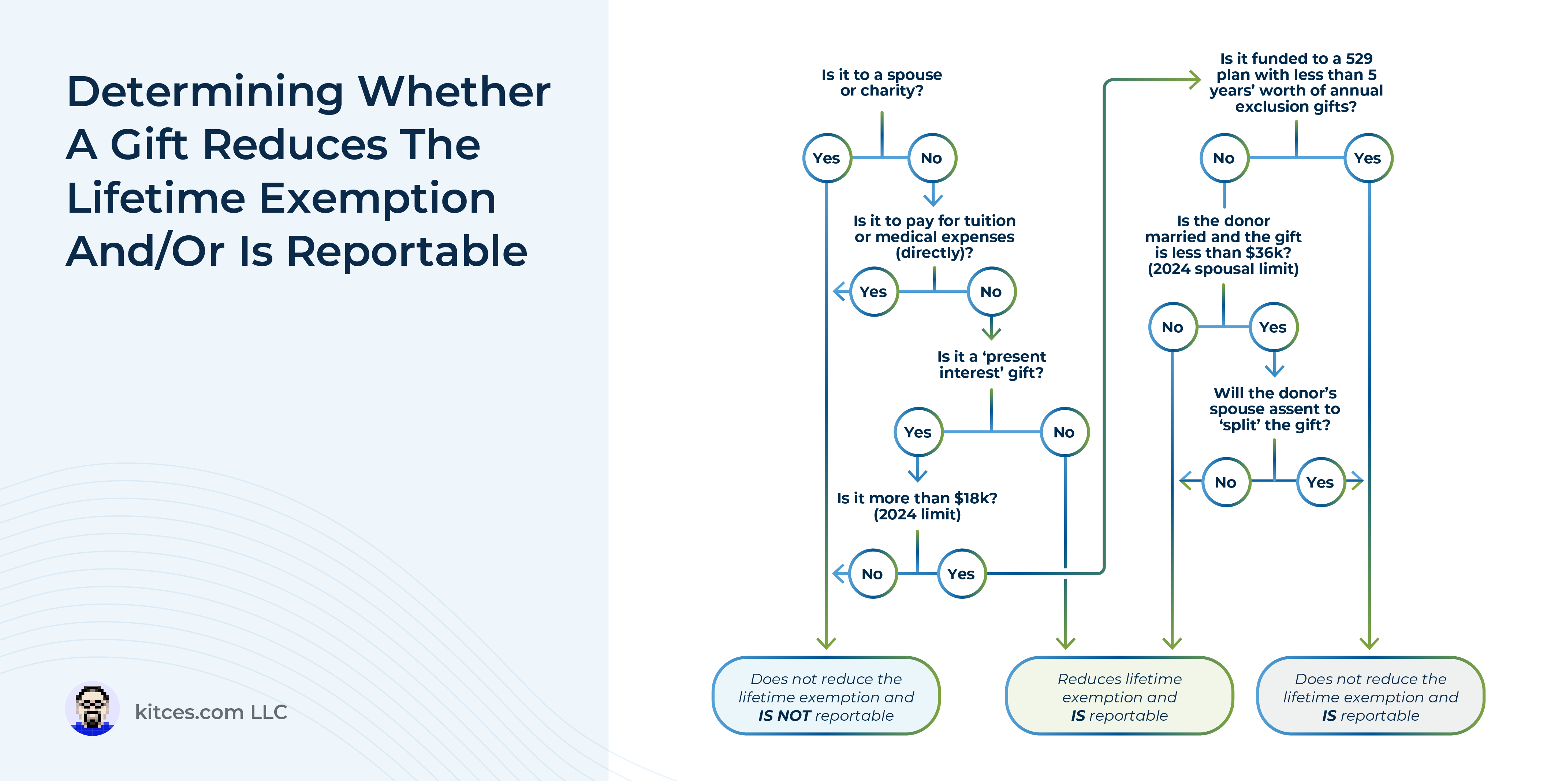

While all gifts could technically be considered taxable to the donor, the annual gift tax exclusion (currently at $18,000) provides for a practical allowance that makes it unnecessary to track and report every small gift (because no one wants to spend time accounting for the value of birthday gifts like bikes, books, or cash!). Furthermore, every individual also has a lifetime gift and estate tax exemption ($13.61M per recipient in 2024). Both the annual gift tax exclusion and the lifetime gift and estate tax exemption come with various nuances that determine what counts toward these exemptions.

For clients looking to give sizable gifts, advisors can help navigate any tax implications by considering how the gift will be given. For example, direct gifts (e.g., those given by cash or check) are simple transfers from donor to recipient, with no limitations on how the recipient can access the gift. On the other hand, gifts in trust allow donors to maintain some degree of grantor-retained control over the recipient’s access, which can safeguard the assets under certain circumstances (e.g., divorce, poor decision-making, or claims by creditors). Finally, there are some contributions that get special treatment. For example, transfers into a 529 plan are considered gifts for tax purposes, even though the donor retains significant control over the transferred funds. And gifts of tuition payments made directly to an educational institution or medical expenses paid directly to a medical provider are exempt from both the annual exclusion and the lifetime exemption, meaning that these can generally be made ‘tax-free’ regardless of amount.

Ultimately, the key point is that despite the many complex rules relating to gifting, clients will rarely be required to pay taxes on a gift. They would need to have both an ultra-high net worth and a desire to gift a substantial portion of their estate during their lifetime to be subject to a gift tax liability. For clients who do fall into those categories, advisors can help them implement relevant gifting strategies to minimize gift tax (e.g., by ‘gift-splitting’ for spouses or dividing gifts across multiple tax years). For others, advisors can offer them peace of mind by clarifying which gifting situations are actually applicable and when they might be obligated to file with the IRS to help them better understand gift taxes. All of which can do a great deal for clients aiming to make the most informed decisions possible!

{kind=link}