Executive Summary

For many workers, a typical career entails a series of successive jobs over several decades, with the end goal of retiring and finally being able to ‘relax’. And while most breaks from work on the traditional path are limited to short vacations, there is a growing movement of individuals who want to take extended time off during their working years to take advantage of their health and opportunities that might not be available to them once they reach ‘normal’ retirement age. One way to do so is through a sabbatical, and advisors can play an important role in supporting clients who are interested in taking this step.

A sabbatical refers to a period of time in which someone takes an extended, planned break from work prior to retirement, often as an opportunity to focus on their wellbeing and/or to gain valuable perspectives of life outside of work. While sabbaticals can involve as little as 1 month for some individuals, taking a sabbatical for 6–12 months is not uncommon. However, longer sabbaticals do carry more substantial financial and career ramifications that require careful planning, especially when extensive travel plans are involved.

One of the biggest challenges of planning a sabbatical is enduring a period of little or no income and coordinating job opportunities after the sabbatical is completed. While some employers have formal sabbatical programs that guarantee the individual can return to the same job after their time away, others may be willing to allow a sabbatical on an ad hoc basis. And there are other employers who are less flexible that may require the individual to quit their job altogether in order to take significant time away from work.

With this in mind, advisors can help clients assess how their sabbatical plans will affect their other financial goals. This could include planning for how their expenses will change during the sabbatical as well as simulating how the sabbatical will impact their financial picture going forward. Advisors can also add value by analyzing tax planning opportunities during the sabbatical; for example, having reduced (or no) income during the sabbatical could create unique opportunities for Roth conversions or harvesting capital gains.

Advisors with clients who might be interested in taking a sabbatical can start the conversation at a strategic level, thinking about their goals for the time off as well as how it relates to their other life objectives. For example, some clients might be fine with taking a one-year sabbatical that pushes out their projected retirement date by two years, while other clients might prefer to stick with an earlier retirement date. In addition, advisors can help clients explore contingency scenarios if they do go through with the sabbatical. For example, an advisor can model what the client’s financial picture will look like if it takes 3 months longer than anticipated to find a job after returning from the sabbatical.

Ultimately, the key point is that advisors are uniquely positioned to add significant value for clients who are considering a sabbatical, both in conceptualizing what the sabbatical would entail and how it would affect their other financial goals. In the end, while taking a sabbatical might not maximize a client’s net worth, it could be a decision that maximizes how they experience their life!

In the US, we are generally programmed to follow the traditional “9-to-5, work-until-you’re-65” concept where we work our whole lives before we truly start to experience it in ‘retirement’, which is defined a lot of different ways by different people, depending on their unique goals and circumstances. However, the rise of ‘mini-retirements’ and the Financial Independence/Retire Early (FIRE) movement is challenging this concept as people want to ‘experience’ more of their life now, rather than deferring potential life highlights until retirement. One way of doing this is through a sabbatical.

A sabbatical is an often-talked-about-but-rarely-executed goal that many people have. It requires veering off from the well-paved “9-to-5, work-until-you’re-65” path and wandering into lesser-known territory, which can be scary to both clients and advisors because nobody wants to uproot their long-term financial future by doing so.

However, a deeper look into the numbers reveals that taking extended time off from work can have very little impact on an individual’s projected long-term financial future, if planned for properly. This prompts the question – are sabbaticals being made out as more financially challenging than they actually are? Can individuals intentionally start planning to take a sabbatical, especially in between jobs or a career change?

If planned for properly, individuals can take a sabbatical with the peace of mind that their long-term financial future will remain intact, while allowing them to accomplish a once-in-a-lifetime goal at the same time. Which means that advisors have the opportunity to help clients interested in taking a sabbatical plan a strategy to do so, by first assessing how best to address the long-term financial concerns so that they can then more deeply discuss the short-term, tactical financial decisions (and other non-financial decisions) that are needed to support their goal.

What Is A Sabbatical?

A sabbatical is defined as a period of time in which someone takes an extended break from work. The ‘extended break’ can mean different things to different people. While it could mean as little as 1 month for some individuals, taking a sabbatical can run for as long as 6–12 months, which generally carries more substantial financial and career ramifications that require careful planning, especially when extensive travel plans are involved.

A Sabbatical Can Recharge Our Energy And Allow Us To Experience Life Now

A sabbatical can offer individuals a unique opportunity to focus on their wellbeing, gain valuable perspective on life outside of work, reset mentally, and re-prioritize their time. Which is important, given that a 2021 study, conducted by the job search engine and hiring platform Indeed, found that 52% of survey respondents reported feeling burnout.

In addition, there may be several life goals that clients could accomplish during their sabbatical, which may otherwise be difficult to do while working full time (otherwise making it necessary to put off those life goals until retirement). Yet for individuals whose top priorities include extensive travel, what better time to experience the world than when they are young and healthy? What if they actually took that trip around the world? Or what if they took extended time off just to spend simple quality time with family?

A sabbatical can also give individuals a preview of what retirement will mean for them in the future. It allows them to dip their toes into the water and experience extended time off from work before diving in and fully retiring in the future. And taking a sabbatical may cause some to redefine their values and priorities altogether, which could drastically impact their life (and finances) in even more positive ways going forward.

Sabbaticals Are Generally Hard To Coordinate With Most Employers

The idea of taking a sabbatical is somewhat new in America, and most companies still don’t permit them. A 2017 research report by the Society For Human Resource Management showed that only 12% of companies surveyed offered an unpaid sabbatical program and 5% offered a paid sabbatical program.

Compare this to Europe, where taking a sabbatical is far more common. In Sweden, employers are actually required to grant employees a leave of absence from their employment for up to 6 months to pursue entrepreneurial ideas!

This prompts the question – why don’t more people take sabbaticals? For most, they are primarily concerned about the impact on their career, and having the financial means to afford losing the income that generally results from taking a sabbatical. While it can certainly be difficult to approach a current employer about taking a sabbatical (especially if the employer doesn’t offer a program, and even more so if it would jeopardize their current role), many people can instead plan to take a sabbatical when they are in between jobs.

In fact, with the rise of the gig economy and the ‘Great Resignation’, people are changing jobs at higher rates than ever before, with 47.8 million Americans who voluntarily quit their jobs in 2021, up by 12 million compared to 2020. While the need to handle childcare during the pandemic likely factors into that figure, the rise of remote work is expanding employment options and providing more opportunities for people to change jobs at a higher frequency.

Though even before the Great Resignation, people still changed jobs at a high pace. According to a 2021 study by the U.S. Bureau of Labor Statistics, the average baby boomer born between 1960 and 1964 held 12.4 different jobs from age 18 to 54!

For advisors who know that clients are considering leaving their jobs in the future, perhaps they can begin by asking clients, “Have you ever considered taking a sabbatical before starting your next job?” Because these gaps in employment can serve clients with valuable opportunities to get a much-needed mental break, and even to fulfill some of their life goals that might not be possible while working for an employer.

A Sabbatical Is More Affordable Than Most People Think, And May Even Offer Tax Planning Opportunities Along The Way

Now let’s say an advisor has a client who wants to take a sabbatical – what does this mean for the client’s financial future?

Let’s consider an actual example where I helped my own clients plan for a sabbatical – I will call them Ned and Cat Stark (shout out to the Game of Thrones fans!).

Ned (age 39) and Cat (age 38) are a married couple with no kids. They earn $255,000 combined income per year, spend on average $6,000 per month, and they save roughly $117,000 per year from cash flow, which funds various long-term taxable investment accounts. Their current net worth is approximately $1.2 million, which has put them in a very strong financial situation to achieve their goal to retire early.

Ned and Cat were very interested in taking a year-long sabbatical to travel around the world, but expressed some concerns about how it would impact their early retirement plans.

To help them assess whether the sabbatical would be a viable option, we first walked them through projections to show how forgoing income from one year while on sabbatical would impact their long-term financial future. We then helped them identify the ‘true’ cost of the sabbatical and wrapped it together by discussing the near-term tactical decisions to make it possible.

Determine The Projected Long-Term Financial Impact Of A Sabbatical First, And Then Engage In Short-Term Tactical Conversations

When modeling the long-term financial impact of Ned and Cat’s sabbatical, we knew for certain that these models wouldn’t be completely accurate, as it’s impossible to predict all the variables that go into the models – life always turns out differently from what we plan for. However, these projections did allow us to take a 10,000-foot view of how their projected financial independence age would change if they were to take a sabbatical, and to consider how we would translate those takeaways into near-term decisions.

In order to create these models, we utilized eMoney’s Decision Center to estimate Ned and Cat’s projected financial independence age when they could viably retire, with and without a sabbatical. We defined their financial independence as the year when their estimated cash outflows were roughly at or less than 3.6% of the total portfolio assets using a straight-line projection (no Monte Carlo) beginning in the year they stopped working.

Is this perfect? Nope. But given that Ned and Cat’s financial independence was projected almost 10 years out, is it good enough to see the long-term impact of a sabbatical? I’d say so.

In the scenario of no sabbatical, their estimated financial independence ages (46 for Cat and 48 for Ned) were determined as follows (assuming a 6.75% rate of return, a 2.44% inflation rate, and using straight line cash flow projections):

In the scenario of taking a sabbatical, their estimated financial independence age was only pushed out by one year – age 47 for Cat and age 49 for Ned. The sabbatical was modeled by showing a $0 income for all of 2023 and a cash outflow of $116,800, which represented their estimated total spending during the year of the sabbatical. After in-depth conversations with Ned and Cat, they felt confident that they could return to their pre-sabbatical income levels after they returned (which is a very important variable to discuss with a client).

As an advisor, I am very hesitant to rely on these models for precision, but I do use them to see trends. The trend here makes intuitive sense without even diving deep into the numbers. Losing a year of income next year would need to be made up by adding a year of income later, to end up in roughly the same spot financially. After all, they weren’t pulling money out of retirement accounts to fund the sabbatical – they were simply pausing saving for a year (while their existing retirement savings would continue to grow as well).

Showing this model to Ned and Cat allowed us to have a more engaging conversation about whether the sabbatical was possible or not. Were they willing to push their projected financial independence age a year or so to make up for this sabbatical? The answer was an extremely clear “Hell yes”.

Once we felt comfortable with the estimated long-term impact, we shifted our conversations to short-term, tactical decisions.

Determine The “True” Cost Of The Sabbatical

We divided up Ned and Cat’s estimated sabbatical budget into three categories – fixed, variable, and extra costs.

The fixed costs were costs at home that would continue each month during the sabbatical. This included mortgage/rent, insurance payments, debt payments, etc. These were relatively easy to identify.

The variable costs were those they were currently incurring, but that would likely be higher each month. This included food, medical, activities, etc.

The extra costs were costs they were not currently incurring and would need to be added separately as one-time costs. This included flights, lodging, experiences, etc.

Ned and Cat did the research on the extra costs and, when adding up all three cost categories, we ultimately arrived at a total sabbatical budget of $116,800 (which was a good bit higher than their current $72,000/year lifestyle).

Within the sabbatical budget, we made conservative estimates for the variable expenses that could be reduced if needed. For example, we assumed over a 50% increase in spending on food during the sabbatical, which could certainly be cut if other spending (like medical) was higher. The experiences (which account for additional entertainment and shopping expenses during the sabbatical) and accommodations could also be reduced, since they weren’t planning to book everything in advance; this would provide them with the flexibility to make changes if they found themselves going over budget during the sabbatical.

Develop A Near-Term Savings Plan To Fund The Sabbatical

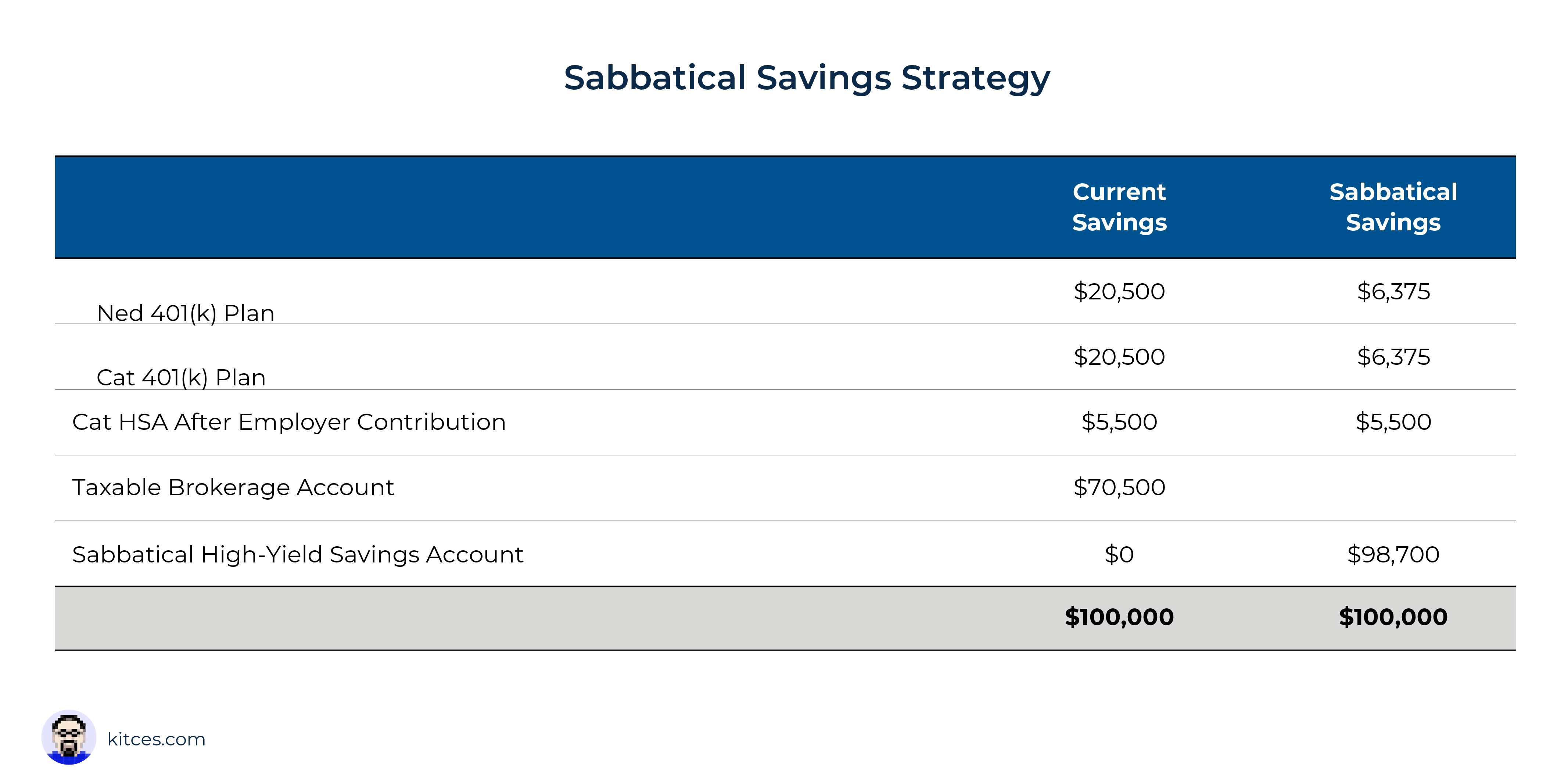

To ensure that Ned and Cat had the full $116,800 saved up in cash before they went on their sabbatical (in addition to maintaining their emergency fund target of $30,000), we decided to open a separate high-yield savings account and named it “Sabbatical Fund”.

Ned and Cat were already saving about $117,000 per year, all of which was going into retirement accounts and long-term brokerage accounts. To meet their sabbatical funding goal of $116,800, we decided to lower their employer 401(k) plan contributions to a minimum contribution of 5% that would still entitle them to receive their full employer match, continue to max out their Health Savings Account (by contributing $5,500 after the employer contribution of $1,800), stop the brokerage account contributions, and allocate the remaining savings directly into their Sabbatical Fund.

Their estimated monthly savings into their Sabbatical Fund was about $98,750 ÷ 12 = $8,229 per month, which meant they would have their Sabbatical Fund savings goal met in about $116,800 ÷ $8,229 = 14 months.

Take Advantage Of The Clients’ Low-Income Tax Bracket During The Year Of The Sabbatical

During the year of their planned sabbatical, Ned and Cat’s salaries will literally be $0, which provides us with many tax planning opportunities. It’s rare for a client to go from a high tax bracket in one year to a very low tax bracket the next year, and then back to a high tax bracket the following year.

The basis of good tax planning is to defer income when your tax rate is high, and take out or otherwise ‘generate’ (e.g., recognize deferred) income when your tax rate is low. Accordingly, we can take advantage of Ned and Cat’s low-income sabbatical year by completing Roth conversions, such that their total taxable income at least matches their Standard Deduction amount. Furthermore, we can also sell appreciated long-term holdings in their taxable account at 0% capital gains rates, up until the 15% capital gain tax rate kicks in.

Based upon 2022 tax figures, this means we can convert $25,900 of their pre-tax accounts to Roth, and then also realize $83,350 of long-term capital gains, without paying $1 in tax. In an environment where we don’t otherwise want to change the investment allocation, this simply means we can purposefully sell appreciated holdings in the clients’ taxable accounts to realize capital gains, and then immediately replenish with the same (or similar) funds to ensure we are maintaining market exposure (as there are no ‘wash sale’ rules when harvesting capital gains, that only applies to capital losses!).

In a ‘normal’ tax year for Ned and Cat, the Roth conversion would result in $25,900 × 24% (marginal ordinary tax rate in 2022) = $6,216 of tax, on top of the additional ordinary income tax due from their salaried earnings, and the long-term capital gains would result in $12,503 of tax. Not only are they fulfilling a life goal by taking the sabbatical, but they are also saving $6,216 (ordinary) + $12,503 (capital gains) = $18,719 of taxes while doing it, offsetting a significant portion of their increased sabbatical-year spending in the first place!

For other clients, it’s important to explore what other ways you may be able to expedite or realize income during the low-income sabbatical tax year. For clients that have access to a 457(b) or other deferred compensation plans, those accounts could be a great savings vehicle for the sabbatical, since they can make pre-tax contributions to the account in the years leading up to the sabbatical, and then withdraw the funds during their sabbatical year penalty-free (and at a lower tax rate thanks to the low-income tax year)!

Discuss How Taking The Sabbatical Will Impact The Clients’ Careers

Once Ned and Cat felt comfortable with the financial ramifications of their sabbatical, we shifted our conversations to the career side. What would this mean for their current jobs? Neither of their employers offered a formal sabbatical program, so taking the sabbatical could mean they would have to leave their jobs.

Ned was already planning to change jobs, so he wasn’t too concerned about this. However, Cat loved her job, had been there for over 10 years, and really valued the work-life flexibility it provided. We didn’t know how Cat’s employer would handle her request, so we had to engage in difficult conversations before she brought up the conversation with her employer.

Would she be willing to give up her job for this sabbatical? How would she feel about starting from scratch with a new employer? Does she believe she would be able to find another job easily?

Cat felt very confident that she could find another job with a similar level of income easily, but struggled with the possibility of having to leave her current job, which she loved. However, during our discovery process, where we lead clients through George Kinder’s 3 Life Planning questions, I pointed out what Ned and Cat said while answering question 2, which goes like this:

This time, you visit your doctor, who tells you that you have five to ten years left to live. The good part is that you won’t ever feel sick. The bad news is that you will have no notice of the moment of your death. What will you do in the time you have remaining to live? Will you change your life, and how will you do it?

Ned and Cat both independently answered that their number one priority in the scenario posed by this question would be to take a trip around the world. This was the boost that Cat needed – she felt confident that this was their number one priority as a couple, and the career implications were not as important to her.

When they actually had these conversations with their employers, they were pleasantly surprised that their employers were not only accepting, but supportive of their decision! Ned’s boss told Ned to contact him 3 months prior to returning from the sabbatical so they could find him a new role (and one he liked more!) within the company. Cat’s boss granted her leave without pay, so her role will still be there when she returns.

How Advisors Can Approach And Navigate Sabbatical Conversations

An advisor’s primary role is to help clients align their financial decisions with their life and their goals. Of course, not all clients will be interested in taking a sabbatical, but for those who are, it’s an amazing opportunity for advisors to illustrate their value to the client. And discussing this opportunity in depth can uncover what it takes to plan for a sabbatical properly and provide clients with the confidence that they wouldn’t necessarily need to uproot their financial lives and other goals at the same time. A sabbatical may not be a decision that will maximize a client’s net worth, but it could be one that maximizes their life.

Start Sabbatical Conversations At A Strategic Level

Taking a sabbatical will certainly involve some short-term sacrifices. Having a reduced or no income for an extended period of time will impact a client’s other long-term goals. As advisors, it’s important for us to navigate client conversations to make sure they clearly understand the many implications involved.

How will taking a sabbatical impact clients’ other long-term goals? Are they comfortable with those tradeoffs?

For Ned and Cat, their tradeoffs were pushing their projected age of financial independence out by one year. Additionally, Cat would potentially have to leave a job that she loved (although this didn’t happen!). They felt like these tradeoffs were worth it for the once-in-a-lifetime experience.

Each client will have a unique set of tradeoffs that they will need to consider. They may need to spend less in the near-term, pull their kids out of school, delay major purchases, forgo a promotion, etc. Some of these possible outcomes can be measured financially, though others can’t.

Illustrating to a client how their other goals would be impacted by the decision to take a sabbatical can empower them to make more life-centered decisions and feel comfortable pursuing potential opportunities by carefully assessing the tradeoffs.

Engage Clients In Several “What If?” Conversations To Help Plan For Different Outcomes

Some clients will be ready to go on a sabbatical tomorrow, whereas others will be a lot more cautious. It’s scary to make such a big, untraditional life decision!

It’s important to create a safe space for clients to talk openly about all of their fears and concerns. Our brains are hard-wired to immediately think about why we can’t do something, but advisors can help clients reframe their thinking to clearly consider how a sabbatical can potentially work for them!

One of my favorite books is The 4 Hour Work Week by Tim Ferriss. In this book, Tim outlines the following framework for facing fears head-on:

One of my favorite books is The 4 Hour Work Week by Tim Ferriss. In this book, Tim outlines the following framework for facing fears head-on:

- Define your nightmare – what is the absolute worst thing that could happen if you did what you are considering?

- What steps could you take to repair the damage or get things back on the upswing, even if temporarily?

- What are the outcomes or benefits, both temporary and permanent, of more probable scenarios?

- What are you putting off out of fear?

- What is it costing you – financially, emotionally, and physically – to postpone action?

- What are you waiting for?

If clients don’t openly discuss their fears, then they’re unlikely to take action. For Ned and Cat, their biggest concern was not having jobs when they got back from the sabbatical, and that the job search would take a considerable amount of time. Therefore, we dove a bit deeper into that scenario.

First off, they had a $30,000 emergency fund, which represented about 5 months of living expenses. This would be the first source of cash to replace their lost salaries. We then discussed how only one of them would need to be employed to cover living expenses (given their actual non-sabbatical lifestyle costs). So, at the very least, if only Ned or Cat were to find a job within the first six months after their return, they would be able to cover their living expenses without completely depleting their emergency funds (and without needing to touch their retirement savings at all). If neither Ned nor Cat were able to find a new job after 6 months, they would still be able to tap into their taxable account for near-term expenses.

Diving even deeper – would they be comfortable taking a job they weren’t as passionate about, even if it weren’t the best long-term fit and served just to pay the bills? Would they be willing to make changes to their long-term plans for early financial independence if things didn’t play out as initially planned?

Going through these conversations was crucial, especially as the sabbatical started to feel ‘real’, and before they talked with their employers. Clients sometimes need to fully understand and be prepared for the worst, before being able to move forward with some of their most exciting decisions.

Help Clients Narrow In On The Cost Of The Sabbatical, And Consider Working With A Travel Expert To Fine Tune Plans

A sabbatical won’t significantly impact a client’s long-term future… as long as everything goes at least somewhat close to what’s planned.

The biggest variable with the sabbatical is the budget. For Ned and Cat Stark, we built a buffer in their budget, but also tried to get really granular about the expenses to ensure we’d be close to estimates. If we budgeted for $116,800 and they ended up spending $200,000, then we’d likely run into some trouble.

As advisors, we really need to ensure a client’s sabbatical budget is well thought out and realistic. It won’t be perfect, but we should make sure it’s at least in the ballpark. It’s important to also have ‘checkpoints’ during the sabbatical to ensure that clients are still on budget and, if not, what changes they would need to make.

Given the cost uncertainty, it may make sense for advisors and their clients to work with a travel expert to help design a sensible plan with realistic cost estimates. Our firm works with Susie Chau from Carpe Diem Traveler who helps clients plan, prioritize, and budget a sabbatical.

Susie provided per-day cost estimates based on the luxury of travel, so that Ned and Cat could compare their options by 3-star, 4-star, and 5-star ratings in the various countries where they were planning to spend time. We then compared these estimates to Ned and Cat’s actual sabbatical budget to ensure their budget estimates were in the ballpark and, if not, what they were missing.

In addition, Susie identified the ‘peak’ seasons (i.e., where costs are higher) and ‘shoulder’ seasons (i.e., where costs are lower) for each country to show Ned and Cat the most cost-effective times they could travel to each country.

While these travel expense estimates were very high-level and likely to be different from the actual expenses, they were valuable in helping us identify which countries were more expensive and which countries were more affordable. In turn, this process helped Ned and Cat determine how much time they would spend in each country to ensure that they would be able to stick to their sabbatical budget.

Having an expert opinion can give clients peace of mind that they are thinking about their sabbatical with the right expectations, and that they have realistic cost expectations about the journey ahead.

Ned and Cat Stark are scheduled to begin their sabbatical at the end of 2022, and being their guide throughout the process has been one of the most rewarding experiences that I’ve had as an advisor. The process required all of us to reframe how we think about ‘traditional’ financial decisions and to get creative on how to plan their finances to accommodate this untraditional decision. The financial planning involved was intellectually challenging, but more importantly, it was extremely fulfilling to enable our clients to make such a memorable life decision, with the confidence of knowing that their financial life would remain intact.

Sometimes the best decisions advisors can help clients make have nothing to do with maximizing their net worth but, rather, with helping them make once-in-a-lifetime memories in a financially responsible way!

{kind=link}