Fact 1: Most young and middle-aged investors need life insurance.

Fact 2: Term insurance is the best and the cheapest way of purchasing life insurance.

Fact 3: Term life insurance does not come cheap.

Therefore, while it is super critical to buy life insurance, it can cost you a lot of money.

How do you reduce the Term life insurance premium?

Your life insurance needs are not static. Your life cover requirement keeps changing during your life.

Your life cover need increases when you assume additional responsibility (marriage or birth of a child). On the other hand, it decreases as you achieve your financial goals or your savings for the goals grow. For example, your outstanding home loan will keep going down over the next few years. Your children may become independent and you won’t have to provide for their expenses. In such a case, if you had gone for just one big life insurance plan, you may find yourself paying a premium for the extra cover you don’t really need.

And therein lies the solution.

Since our life insurance requirements keep changing, a life insurance ladder can be really helpful. By laddering your life insurance policies, you can save on significant amount of premium. In this post, we discuss life insurance ladder and its benefits. We also discuss how to create an effective life insurance ladder. Before that, a quick note about how much life cover you need.

How much life cover do you need?

To quite an extent, it is common sense.

Absorb the following equation.

Your Existing Wealth + Life Insurance Cover = Money to square off all Your loans + Money needed to achieve your goals + Money needed to provide for regular expenses of the family

As you can, various elements of this equation will keep changing. Existing wealth goes up as you accumulate wealth. Money needed to square off loans will go up when you take loans and goes down (gradually) as you repay those loans. Money needed for financial goals goes up as you add goals or goes down as you achieve those financial goals.

If you have an even deeper mathematical inclination, I shared an excel based calculator in an old post.

How a life insurance ladder works?

Under a life insurance ladder, you purchase life insurance policies with different tenures (maturity). The maturity (or the end of policy tenure) of the policies coincides with the term of a set of important goals. As your major life goals are achieved and corresponding life insurance policies expire, your total premium outgo reduces.

Note: My usage of the word “Maturity” may suggest that you use traditional insurance plans or ULIPs for creating life insurance ladders. While you can do that, it won’t be a very wise choice. It is better to create a life insurance ladder with term life insurance policies.

You take life insurance to bridge the gap between your existing assets and the money required to meet your goals.

As your investment corpus grows over a period of time, this gap shall reduce as the time passes. Moreover, once you achieve the goal, there is no need to provide for that goal through life insurance. Thus, you can see your insurance requirement going down as time passes. However, we cannot reduce our Sum Assured regularly. In fact, your life insurance plan won’t even allow you to reduce Sum assured. In such cases, a life insurance ladder can help.

The life insurance premium depends on the following factors.

- Sum Assured (life coverage amount): Higher Sum Assured means higher premium

- Entry Age of the applicant: Lower entry age means lower premium

- Gender: Premium is usually lower for females.

- Health condition of the applicant : If you have an existing condition such as diabetes, your premium will go up.

- Policy tenure: Longer policy tenure means higher premium

- Habits: If you smoke, the premium will be higher

Longer the policy tenure, higher the annual premium for the same sum assured. Here are the term insurance quotes for 25 and 30 year old non-smoker males from an insurer website.

You can see that the annual premium increases with the age of the applicant, Sum assured and the policy term.

As the policy term increases, the chances of demise during the policy term will increase (everything else being the same). Therefore, the higher premium for the longer policy tenure reflects this risk taken by the insurance company.

Additionally, everything else being the same, the probability of demise also increases with entry age.

How a Life Insurance Ladder helps?

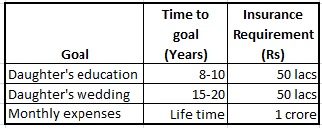

Let’s understand this with the help of an example. Suppose you are 30 years old and have the following goals.

You have taken a policy term of 30 years even for monthly expenses (which may have to be met for many more years). The underlying assumption is that by the time you retire at the age of 60, you would have saved enough to provide for the expenses of your family. Thus, no further life insurance should be needed beyond your retirement age.

So, you have total life insurance requirement of Rs 2 crores.

Option 1

You purchase a 30-year term plan for an annual premium of Rs 20,575.

You will pay Rs. 20, 575 X 30 years = Rs 6.17 lacs over the next 30 years.

Option 2

You can purchase three life insurance policies.

- Rs 1 crore cover for 30 years: For Family monthly expenses after your demise: Rs 10,287 per annum for 30 years

- Rs 50 lacs for 20 years: For Daughter’s wedding: Rs 4,954 per annum for 20 years

- Rs 50 lacs for 10 years: For Daughter’s education: Rs 4,443 per annum for 10 years.

Total premium of Rs 19,684 per annum. Not much difference from Option 1 (Rs. 20,575 per annum).

However, as the policies with shorter tenures expire, the total annual premium payout (under insurance ladder) will fall sharply. From the 11th year, the total annual premium will fall to Rs 15,241. From the 21st, it will fall to Rs 10,287.

Your overall premium payout will reduce significantly once the policies start to expire. Once the insurance policy that covers the daughter’s education expires, you can use the extra cash to invest and build your investment corpus. In the example under consideration, total savings through life insurance ladder will be Rs 1.65 lacs over 30 years. If invest these savings regularly, the difference will grow to Rs 4.06 lacs (8% per annum) and Rs 6.96 lacs (12% per annum) at the end of 30 years.

Under this case, the total annual premium for the life insurance ladder (breaking into 3 separate policies) is lower than the annual premium for the single policy. This may not always happen. Different combinations of age, sum assured, policy terms and even insurance companies may throw up different results.

You must also realize there are certain costs associated with purchasing a fresh cover. For instance, a cover of Rs 1 crore for a term of 30 years costs Rs 10,287 per annum while two covers of Rs 50 lacs each (30 years) cost Rs 11,607 per annum. Hence, breaking up your life insurance requirement across multiple policies will entail some additional costs. Hence, you will have to do some calculations to find out if laddering works for you and the right laddering strategy for your insurance requirements.

Life insurance requirement can increase too

Marriage, birth of a child or assuming a loan can increase your life insurance requirement. A life insurance ladder can be helpful in such cases too. For instance, a person can buy an insurance cover before marriage (that meets his/her erstwhile insurance requirements). As the person adds responsibilities over a period of time, marriage or birth of a child), he/she may increase the coverage by purchasing additional life insurance.

This method helps in two ways. First, it helps in a more accurate assessment. For example, rather than going for a wild guess before marriage, you may be better able to assess your insurance requirement if you know about your spouse’s salary or whether your spouse is working or not. Secondly, as the insurance premium is dependent on both age and policy term, you may actually be able to save on premium.

A 25-year-old single male can buy a Rs 2 crore life cover (for a tenure of 35 years). Or he can buy Rs 1 crore cover today and a further Rs 1 crore after marriage (assuming marriage adds Rs 1 crore worth of insurance requirement). Assuming he marries at the age of 30 (and purchases additional insurance cover post-marriage), his total savings will be ~Rs 3.6 lacs (at 8% per annum) and ~ Rs 14.2 lacs (at 12% per annum) over 35 year period.

Are there any issues with the Life Insurance Ladder approach?

- You may not be able to meet goals in the specified period. For example, you may have thought that your child will go for higher education within the next 10 years and purchased an insurance policy for a tenure of 10 years. However, your child may decide to take a break from studies and may go for higher education only after 12 years. In such a case, if you have not invested well to build a sufficient corpus for child education, you run the risk in the 11th and 12th year (as your insurance coverage would have got over at the end of the 10th year). In case of death in the 11th or 12th year, child education may have to be compromised (or your child will have to take out a loan).

- There is an extra mental effort needed (and do all this planning). You have to keep track of multiple premium payment dates.

- Your nominee may have to get multiple claims processed.

Whether you should create a life insurance ladder

Life insurance ladder may not bring benefits for everyone as the extra costs of purchasing multiple policies may nullify the benefit of an insurance ladder. You cannot purchase a separate term life plan for every long term goal. The financial and administrative overheads of too many policies will kill the benefits of an insurance ladder.

A Life insurance ladder is likely to work better if you can club your goals in different buckets (of tenure) and purchase separate term insurance for each bucket. You can club goals whose tenures are not too different. For instance, goals expected to be met between 6 to 10 years can be clubbed together and a single term life insurance (for a policy term of 10 years) can be purchased for these goals. Similarly, you can create more buckets for different tenure ranges. This way you will have a sizeable sum assured for each policy to counter the cost of having multiple policies. Please note this approach may not work in every case.

Laddering strategy will vary depending on an individual’s requirements. You need to do the math to check whether the insurance ladder is beneficial to you.

You need to be careful in creating the insurance ladder as incorrect assumptions, especially about time to achieve goals, can create problems for your family in the future. For instance, if your insurance policy expires before the achievement of a goal and the investment corpus is not enough to fund the goal, your family will face financial trouble in the event of your death after policy expiry. In such a case, the goal may have to be compromised.

What should you do?

When it comes to life insurance, be conservative. It is better to err on the higher side. It is still acceptable if you are over-insured even though it means higher outgo in terms of extra premium. However, if you are under-insured, your family can suffer financially if anything were to happen to you.

It is extremely important to get your life insurance requirement right. If that’s too much work, seek services of a financial planner or a registered investment adviser in this matter.

You may or may not go for a life insurance ladder. Through the life insurance ladder, you may be able to increase your investment corpus through premium saved. You will have to do some calculations to find out if the insurance ladder is beneficial to you. You must understand that a life insurance ladder does entail a few risks. Getting adequate coverage is the important part. If working out the proper laddering strategy is too much for you, don’t complicate matters and purchase a single policy that covers all your goals.

Life insurance ladder or a single policy, you still need to invest wisely for your long term goals. Life insurance will bridge the gap between the earmarked assets and the required corpus if you die before fulfilling the goals. However, if you survive the policy term, you have to meet those expenses from your investment corpus (and not life insurance proceeds).

This post was first published in June, 2015.

Image Credit: Pixabay

{kind=link}