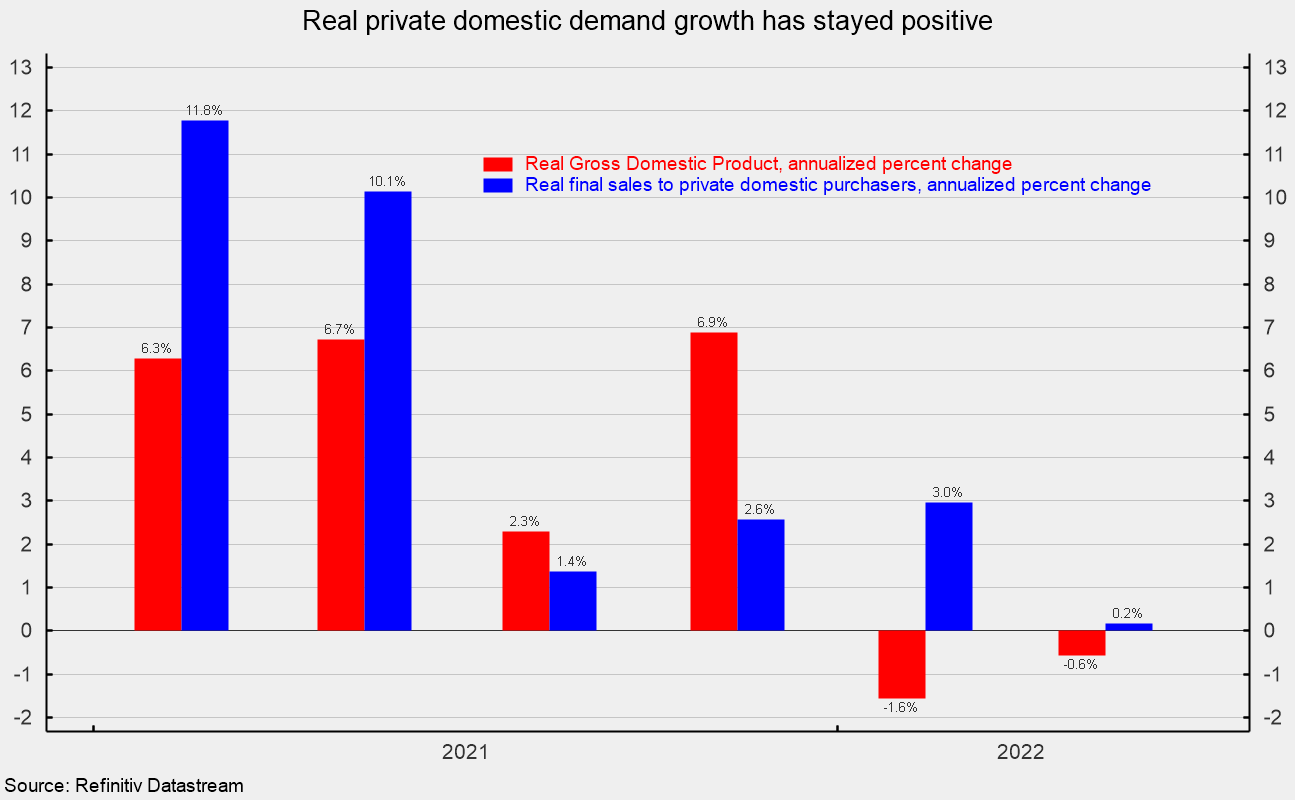

Revised data show real gross domestic product fell at a 0.6 percent annualized rate in the second quarter versus a 1.6 percent rate of decline in the first quarter (see first chart). The advance estimate had shown a 0.9 percent decline. Over the past four quarters, real gross domestic product is up 1.7 percent.

Real final sales to private domestic purchasers, a key measure of private domestic demand, have shown greater resilience. Revised estimates show it rose 0.2 percent in the second quarter following a 3.0 percent pace of increase in the first quarter (see first chart). Over the last four quarters, real final sales to private domestic purchasers are up 1.8 percent.

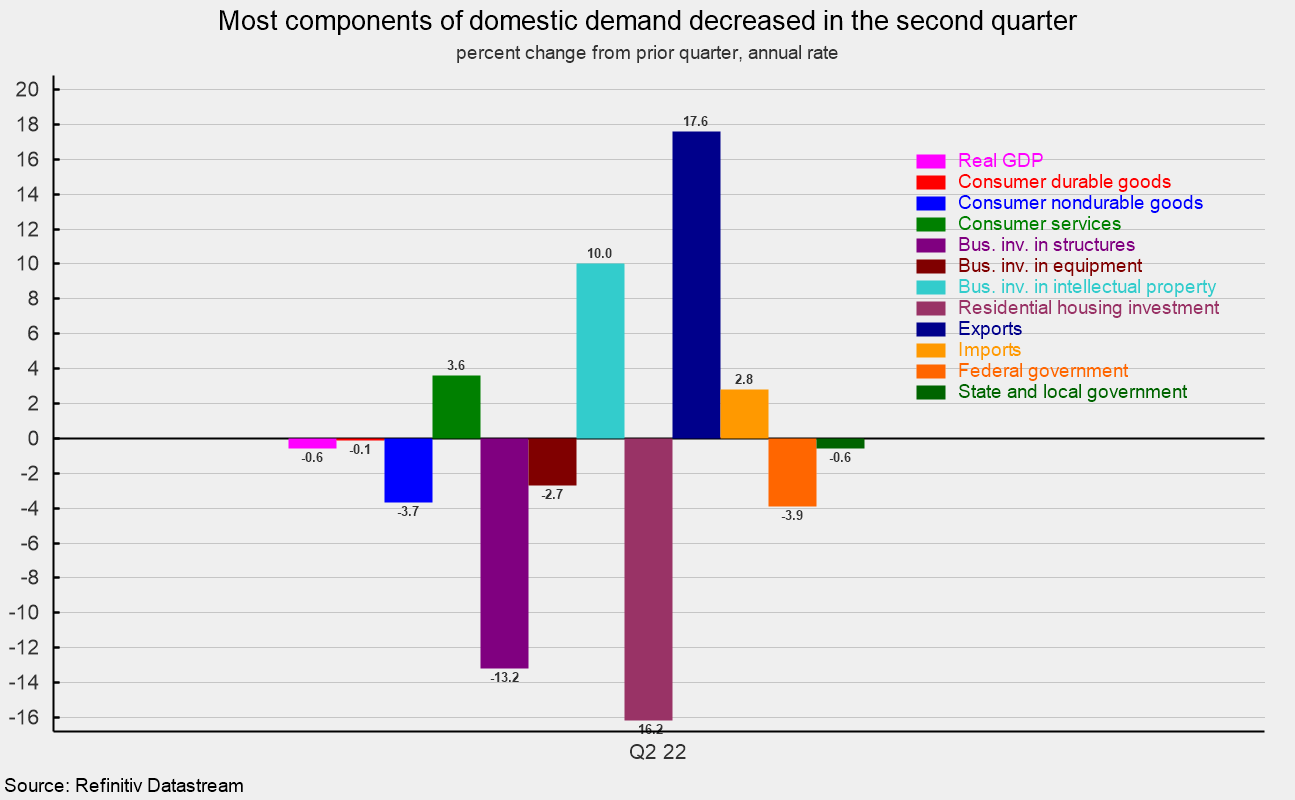

Declines were widespread in the second quarter. Among the components, real consumer spending overall rose at a 1.5 percent annualized rate versus a 1.0 percent gain in the advance estimate, and down from a 1.8 percent pace in the first quarter. That is the slowest pace since the lockdown recession. Real consumer spending contributed a total of 0.99 percentage points to real GDP growth. Consumer services led the growth in overall consumer spending, posting a 3.6 percent annualized rate, adding 1.56 percentage points to total growth. Durable-goods spending fell at a 0.1 percent pace, subtracting 0.01 percentage points while nondurable-goods spending fell at a -3.7 percent pace, subtracting 0.56 percentage points (see second and third charts). Within consumer services, growth was broadly strong, led by food services and accommodation (12.4 percent), recreation (6.8 percent), and other services (5.5 percent growth rate).

Business fixed investment was unchanged in the second quarter of 2022 after a 10.0 jump in the first quarter. Intellectual-property investment rose at a 10.0 percent pace, adding 0.51 points to growth while business equipment investment fell at a -2.7 percent pace, subtracting 0.15 percentage points, and spending on business structures fell at a 13.2 percent rate, the fifth decline in a row, and subtracting 0.36 percentage points from final growth.

Residential investment, or housing, fell at a 16.2 percent annual rate in the second quarter compared to a 0.4 annualized gain in the prior quarter. The drop in the second quarter subtracted 0.83 percentage points (see second and third charts).

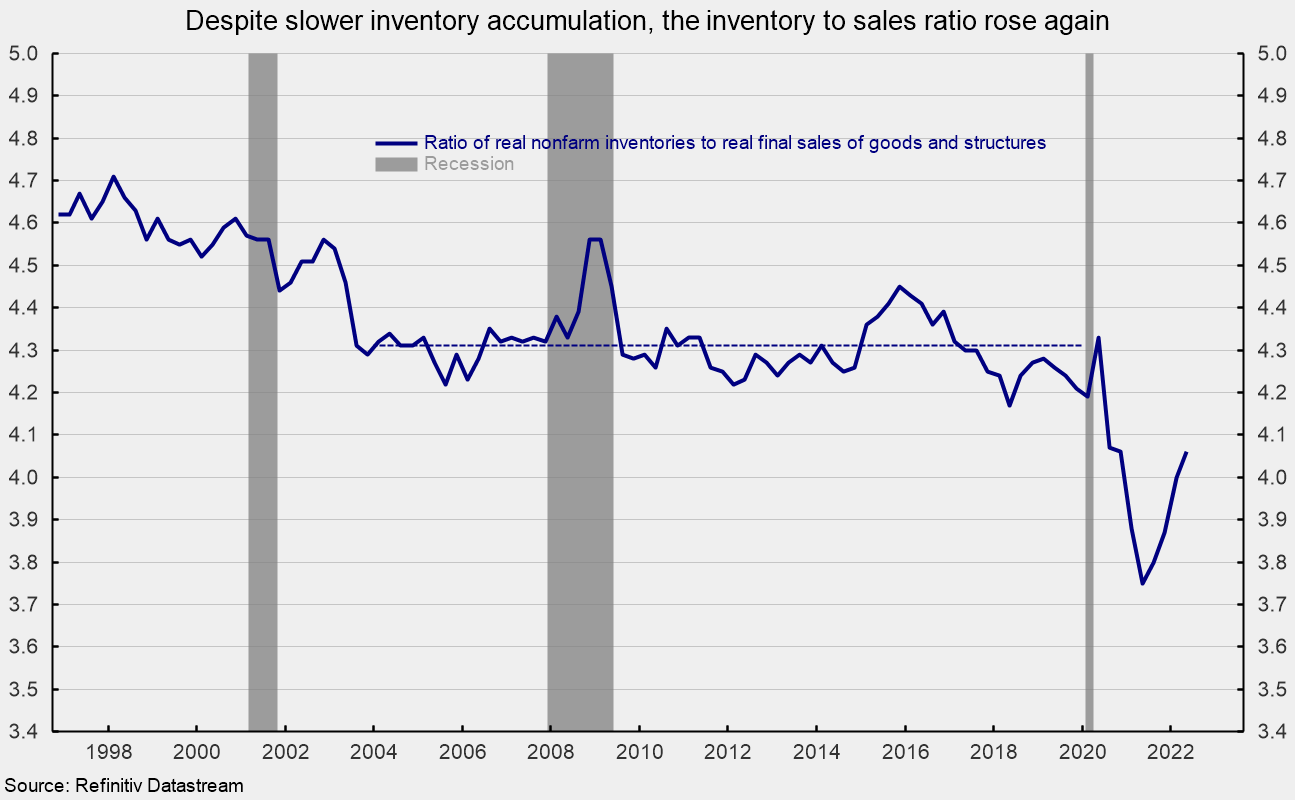

Businesses added to inventory at an $83.9 billion annual rate (in real terms) in the second quarter versus accumulation at a $188.5 billion rate in the second quarter. The slower accumulation reduced second-quarter growth by a very sizable 1.83 percentage points (see third chart). The inventory accumulation helped boost the real nonfarm inventory to real final sales of goods and structures ratio to 4.06 from 4.0 in the first quarter; the ratio hit a low of 3.75 in the second quarter of 2021. The latest result is still below the 4.3 average for the 16 years through 2019 but suggests further progress towards a more favorable supply/demand balance (see fourth chart).

Exports rose at a 17.06 percent pace while imports rose at a 2.8 percent rate. Since imports count as a negative in the calculation of gross domestic product, a gain in imports is a negative for GDP growth, subtracting 0.45 percentage points in the second quarter. The rise in exports added 1.88 percentage points. Net trade, as used in the calculation of gross domestic product, contributed 1.42 percentage points to overall growth.

Government spending fell at a 1.8 percent annualized rate in the second quarter compared to a 2.9 percent pace of decline in the first quarter, subtracting 0.32 percentage points from growth.

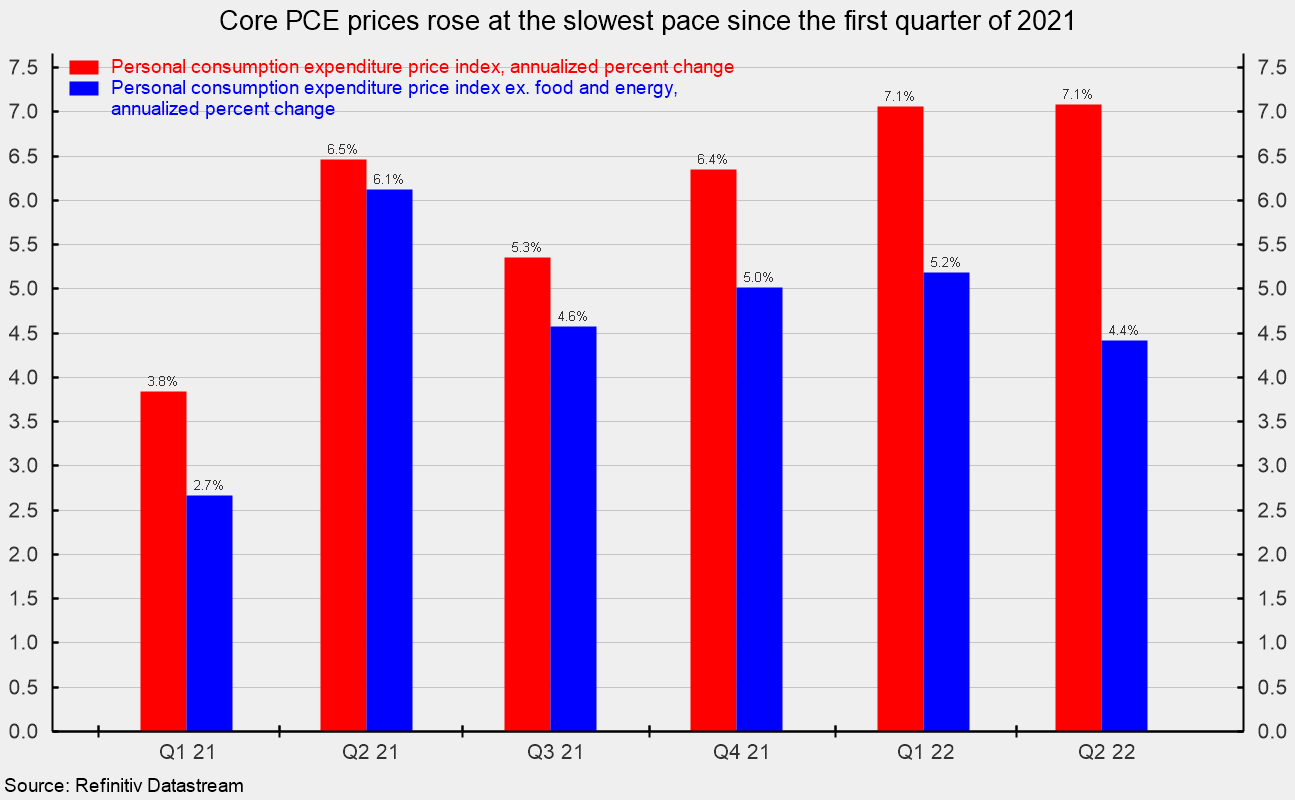

Consumer price measures showed another rise in the second quarter. The personal-consumption price index rose at a 7.1 percent annualized rate, matching the first quarter. From a year ago, the index is up 6.5 percent. However, excluding the volatile food and energy categories, the core PCE (personal consumption expenditures) index rose at a 4.4 percent pace versus a 5.2 percent increase in the first quarter and is the slowest pace of rise since the first quarter of 2021 (see fifth chart). From a year ago, the core PCE index is up 4.8 percent.

Lingering materials shortages, labor constraints, and logistical problems are sustaining upward pressure on prices, though progress is being made on improving the supply-demand balance. Upward price pressures have resulted in an intensifying Fed policy tightening cycle, raising the risk of a policy mistake. In addition, fallout from the Russian invasion of Ukraine continues to impact global supply chains. The economic outlook remains highly uncertain. Caution is warranted.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals.

Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}