All of the value creation for investors comes from the actions they take in falling markets, not rising ones. If you’re not yet in retirement and not finished putting money into your retirement accounts, every 5% the market falls is an increased opportunity for you to buy things that will be worth much more in the future when you eventually sell them. Creating value today that will be realized at some point tomorrow.

I don’t give financial advice here on the blog, or on TV or on YouTube or anywhere else outside my firm. When you see me speaking publicly about investing to a general audience, what I am talking about is what I am personally doing with my money or what we as a firm are doing for our own clients. Advice is personal and so, by definition, cannot be given blindly and indiscriminately. However, in my public remarks, my goal is always to say things that are interesting, smart, helpful, encouraging or meaningful. Not everything turns out that way, but this is what we’re aiming for.

I say this to preface what I want to say next:

If you are under the age of 50 years old and selling stocks now, having ridden the market down 25% from last Thanksgiving, well, I hope you have a damn good reason for doing so. Besides the immediate relief you might feel for getting off the roller coaster. Because from where I sit, everything about the current market environment has now gotten better for investors than the environment one year ago today.

In September of 2021, a year ago, the Fed was thinking that no interest rate hikes would be necessary for the entirety of 2022. “Lower for longer” was the mantra. They didn’t see the need for any rate hikes on the horizon until 2023. As a result, cash was yielding zero and stocks were selling for 24 times earnings.

Fast forward to today – We’re trading at a 15x forward PE ratio (below the five year average of 18) and cash now yields 4%.

Which environment is a better one for investors, that of one year ago today or the one we are currently facing?

Of course today is better. Significantly better. No hesitation.

For me, the answer is obvious. But that’s only because of the length of time I have been doing this and the things I have seen or experienced. For younger, less experienced investors it might not be quite so obvious. A lot of the work we do with our public remarks and content is to change that situation to the extent we can.

In keeping with what I said above about not giving investment advice to the general public, please take the below as being for informational purposes and not a solicitation for you to invest in this or any other stock…

I personally own shares of JPMorgan. I have the dividends automatically reinvested each quarter. JPMorgan is about to pay a dividend this October of $1.00 per share. The dividend is payable on October 31st to shareholders of record as of the close on October 6th. This equates to a yearly dividend of $4 per share, assuming they don’t have to cut it. At today’s price, that’s a 3.67% annualized dividend yield, precisely matching the yield on a 10-year Treasury bond. JPMorgan sells for 8x earnings and 1.2x book value, outrageously cheap relative to the overall S&P 500.

So consider the person who has a 10 year plus time horizon for the money they are investing today. Shares of JPMorgan will be substantially more volatile than a guaranteed return of principal plus interest from a Treasury. But they offer significantly more potential upside in return. Your risk is that the 100+ year old banking franchise somehow doesn’t make it through the next decade’s ups and downs. That’s a risk most of us would be willing to take in exchange for what could go right.

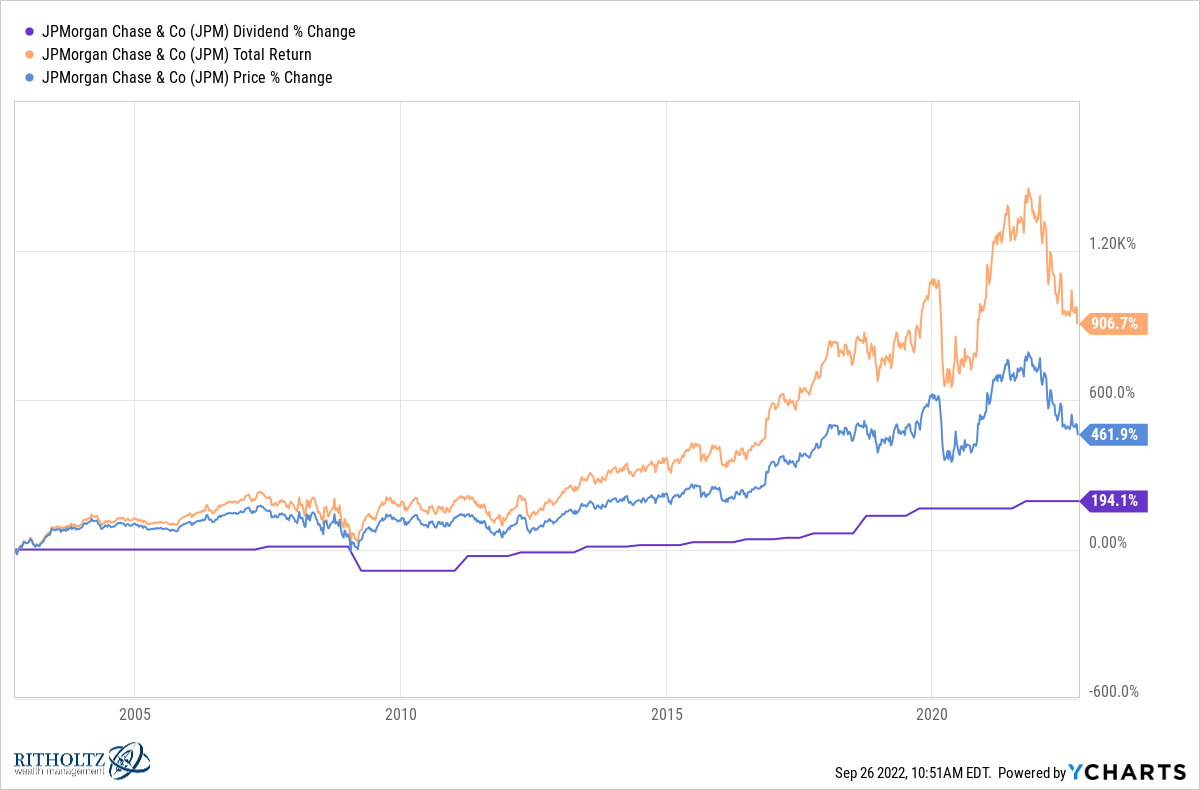

Below, I’d like to show you the last twenty years of JPMorgan’s common stock performance (via YCharts)…

The orange line is your total return over twenty years ending yesterday – a 900% gain for doing nothing other than holding this in a brokerage account and living with the ups and downs. As you can see, the dividends were a very important part of the total return. JPMorgan has grown its annual dividend payout by almost 200% since 2002 (purple line). The blue line is the price return, minus the benefit of dividends along the way. If you’re trading in and out of JPMorgan, or any other stock, you’re not maximizing the full benefit you should be getting as a result of the risk you’re taking of long-term ownership. That’s your fault. You should try to fix that.

I am never going to sell JPMorgan so long as the company continues to do what it does for shareholders, customers, employees and other stakeholders. I will experience years where the stock falls (like this one) and years during which the stock rises, like last year. That’s what comes with the territory. And if someone is willing to sell this stock at 107 having ridden it down from 167 one year ago this week, that’s their problem, not mine and not yours. If they can buy it back at $87, then god bless. If they think they can do that on a regular basis, I have a macroeconomic options trading “alerts” newsletter to sell them.

Again, this is just my opinion and an example of how I have chosen to allocate assets over the course of my career. Your perspective and your time horizon may be different than mine.

But one thing that is undeniable – and I have a century’s worth of data to back this up – market environments like this one are where all of the value creation resides. With today’s lower prices and falling valuations, we are laying the foundation for tomorrow’s success. It may not feel that way in the moment, but that’s why not everyone gets to succeed.

{kind=link}