There seems to be a lot of confusion going on today with respect to inflation, interest rates, and ongoing Federal Reserve policy. A framework for exploring this has many parts: What the Fed (obviously) knows, how it express those views through police like FOMC rates, ZIRP, QE, QT, etc.

There remains the question of what the Fed is actually wrong about.1

It is this last one that I find fascinating and where we can identify the reasons why the Federal Reserve and markets seem to be disagreeing about the future path of rates.

Let’s give the Fed some credit: They know goods’ inflation peaked months ago – they can see the prices of oil, lumber, used cars, shipping containers, etc. And they certainly understand that FOMC policy has substantial lags of anywhere from 6 to 12 months.

What are the major errors that are currently driving Fed policy?

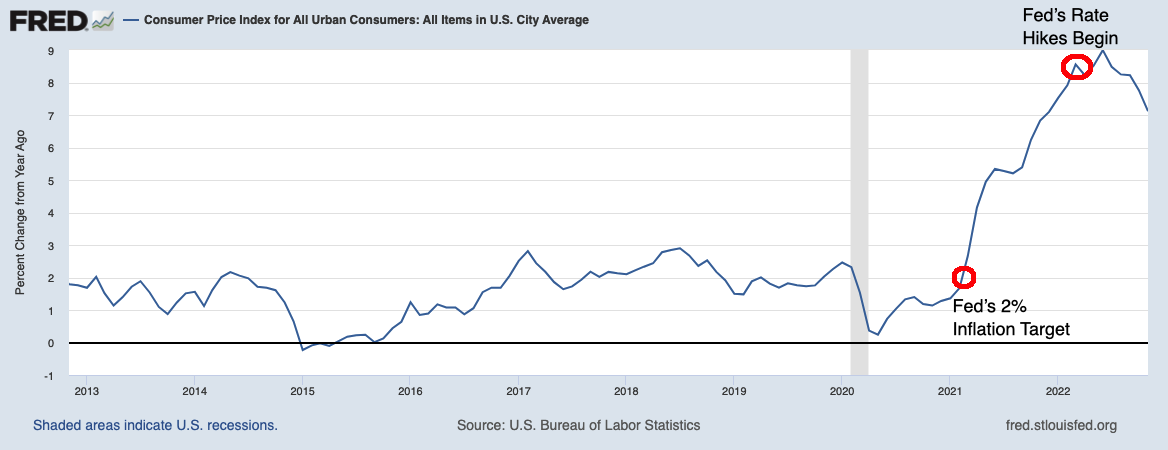

• Tardy: We all understand that Central Bank policy operates on a lag. History suggests that the Fed’s recognition of key market and economic indicators also is on an excessive lag. The result is Fed is always late to the party.

Consider: In the 2010s, the Fed remained on emergency footing from 2008, when they took rates to 0 (zero) until December 2015 (this created lots of distortions). Then again in the 2020s, they remained on emergency footing post-Covid, despite broad evidence of economic recovery.2

The Fed was late to act on rising inflation, waiting a full year from the time CPI ran through their 2% target to raise rates (See chart at top). Today, it appears they are repeating that same error, late to recognize inflation peaked in June and goods’ prices have fallen dramatically.

• Services Inflation: What is the impact of the fastest increase in rates in history? High Fed Funds Rates are causing high mortgage rates which is in turn pricing many people out of buying residential real estate. The net result: Potential buyers become renters, which drives apartment prices higher. Owners Equivalent Rent is the largest portion of the CPI Services sector.

The perverse outcome is the Fed is making the CPI model show both higher and stickier inflation.

• The Wealth Effect: Jay Powell seems to be targeting assets prices, despite equities not being part of the dual mandate.3

The reason for this is that the Fed has institutionally been “all in” on the Wealth Effect theory. The thinking here is that a rising stock market makes Americans feel wealthier, leading to more spending and higher inflation.

There are many problems with this claim, but let’s just give you the biggest two: Most Americans do not own equities; many of those who do have modest holdings in IRAs and 401ks that they won’t touch for years. Its hardly driving spending for 70-80% of consumers.

The second is simply confusing correlation with causation. The same underlying factors that drive higher stock prices – rising GDP, employment and wages – also drive consumer spending and inflation. Hence the Fed believes a rising stock market is what leads to inflation. If you stop to think about for even a moment, you will see they are utterly wrong about this.

• Jay Powell Defers to Economists: Powell is an attorney and investment banker, not an economist. This in itself is not a bad thing. However, it raises the risk that he defers too much to economists (see Wealth Effect, above).

It reminds me of the wonderful quote by Joan Robinson: “The purpose of studying economics is not to acquire a set of ready-made answers to economic questions, but to learn how to avoid being deceived by economists.”

One has to wonder how much of the Fed’s current and past policy errors trace itself to this insightful truism.

Please note I am not part of the contingency of Fed haters out there, nor do I believe that we should “End the Fed” or other such nonsense.4 I do believe the Federal Reserve makes a good faith effort to execute its mission, a job they sometimes do well and sometimes much less so.

I hate unforced errors. Current policies appear so obvious and easily avoided, but are going to cause a lot of unnecessary pain anyway.

If I were Fed Chairman, I would declare inflation is defeated, plant my flag and claim victory, then go home. The battle has already been won. The bigger risk today is snatching defeat from the jaws of victory.

See also:

Jerome Powell’s Grim Inflation Outlook Is at Odds With Markets (Greg Ip, WSJ December 14, 2022)

Previously:

Wealth Effect Rumors Have Been Greatly Exaggerated (November 16, 2010)

Wealth Effect is a Bad Correlation Fantasy (April 25, 2016)

Behind the Curve, Part V (November 3, 2022)

When Your Only Tool is a Hammer (November 1, 2022)

How the Fed Causes (Model) Inflation (October 25, 2022)

Why Is the Fed Always Late to the Party? (October 7, 2022)

__________

1. There is a longer conversation to be had about how the costs of Federal Reserve policy have fallen disproportionately on the poor; this is beyond today’s discussion.

2. Following the rate cuts in March 2020, the Fed stayed at Zero until March 2022. During the same period of time, the S&P 500 rose 67.9% (2020) and 28.7% (2021).

3. The Fed’s dual mandate: First, maintain maximum employment and, second keep prices stable (low inflation) and long-term interest rates moderate. The Fed’s somewhat impossible task is during periods of flux, an inherent conflict exist between those two.

4.As I detailed in Bailout Nation, the Federal Reserve has a rich history of being “often wrong, rarely in doubt.” However I reserve my greatest ire for the ex-maestro, Alan Greenspan, whose disastrous reign not only led to the.com bubble and collapse but also set the stage for the great financial crisis.

{kind=link}